You've seen the pitch before: no state income tax, no capital gains tax, property tax rates so low they barely register on a closing statement. Wyoming checks every box on the tax-advantaged-state checklist that gets repeated across investor forums. Then you run the actual rent against the actual mortgage payment, and the tax advantage turns out to be true and, on its own, not nearly enough.

Wyoming's statewide median home price is genuinely hard to pin down. One dataset puts it near $484,000, another near $570,400, and a third, tracking March 2026 closings, at $440,300, down 2.6% year-over-year. The reason for the spread isn't bad data; it's Jackson Hole. In a state with roughly 580,000 people and a low volume of monthly closings, a handful of multimillion-dollar Teton County sales can swing a statewide median by tens of thousands of dollars in either direction. Strip Jackson out and look at Wyoming's three largest ordinary markets instead: Cheyenne, Casper, and Laramie all trade at a fraction of that headline figure, and none of the three currently cash flows for a buy-and-hold investor.

The tax case is real

Wyoming is one of nine states with no personal income tax, and because there's no income tax base to begin with, the state also doesn't tax capital gains. Sell an investment property for a $200,000 profit and Wyoming takes zero of it at the state level, compared with a state like Minnesota that taxes gains up to 9.85% as ordinary income. Property tax is equally favorable: residential property is assessed at just 9.5% of fair market value before the mill levy is applied, producing an effective statewide rate around 0.53%. Teton County runs the lowest in the state at roughly 0.48%; Weston County is close behind at 0.50%.

None of that is marketing. It's a genuine, durable cost advantage over high-tax states, and it will save an investor real money every single year they hold the property. It just doesn't change what the rent check covers relative to the mortgage payment, which is the number that actually determines whether a deal is a buy.

Cheyenne: the military anchor that still doesn't clear the bar

Cheyenne's median sits at $424,500, roughly flat year-over-year. At 25% down and 6.43% rates, principal and interest on the $318,375 loan runs about $1,999 a month; add roughly $187 in property tax and $120 in insurance and PITIA lands near $2,306. Citywide rent data points to around $1,500 a month for a comparable single-family rental, which produces a DSCR of about 0.65 and a monthly cash flow of roughly -$1,001 after an 8% management fee and vacancy allowance.

Cheyenne's genuine advantage is F.E. Warren Air Force Base, home to a nuclear missile wing and thousands of active-duty personnel and their families, providing the kind of steady, recession-resistant tenant demand that has made military-anchor markets a repeat theme in this state-by-state review. That demand floor supports occupancy, not the underlying price-to-rent math. If your Cheyenne underwriting depends on the base to make a deal pencil, plan on a larger down payment or a lower purchase price than the median, because the tenant base alone won't close a $1,000-a-month gap.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

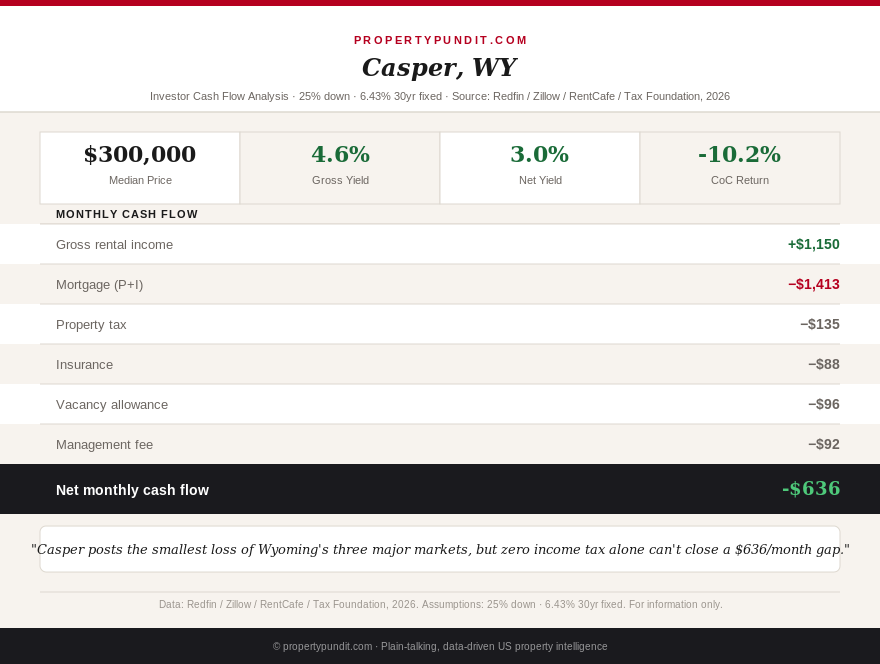

Casper: the smallest loss, mostly because of price

Casper's median runs about $300,000, up roughly 3% year-over-year, and it's the cheapest of Wyoming's three major non-luxury markets by a wide margin. At 25% down, the $225,000 loan carries principal and interest of about $1,413 a month; adding roughly $135 in property tax and $88 in insurance brings PITIA to about $1,636. Citywide rent estimates run closer to $1,150 a month, producing a DSCR near 0.70 and monthly cash flow of roughly -$636 after management and vacancy.

That's the smallest dollar loss of the three cities, and it's mostly a function of the lower entry price rather than superior rent. Casper's economy leans on the energy sector, which means rents and occupancy can swing with oil and gas activity in a way Cheyenne's government-and-military base and Laramie's university base don't. An investor choosing Casper for the smaller monthly gap should treat that cyclicality, not the tax code, as the main risk to underwrite.

Laramie: university demand, thin-market price swings

Laramie's price data is the most volatile of the three. Zillow's smoothed value index sits near $353,500, up about 5.6% year-over-year, while Redfin's transaction-based median jumped to $476,000 in one recent month, up more than 21% year-over-year on a small sample. That's the same low-volume effect distorting the statewide figure, just at city scale: the University of Wyoming's presence means Laramie's housing stock includes both modest single-family rentals and a smaller pool of higher-end sales that can swing a monthly median hard in either direction.

Using the steadier $353,500 figure, a 25% down purchase carries a $265,138 loan with principal and interest near $1,664 a month; adding about $156 in property tax and $103 in insurance brings PITIA to roughly $1,923. Citywide rent sits near $1,400 a month, for a DSCR of about 0.73 and cash flow near -$705 a month after management and vacancy. As in other college towns, that citywide figure likely understates true student-rental income, since by-the-bedroom leases to University of Wyoming students typically out-earn a single-family lease priced at the city average, though that upside requires active, hands-on management rather than passive DSCR-loan underwriting.

If you're underwriting Laramie on citywide rent comps alone, you're probably underestimating the property's real income, but you're also signing up for a management workload that a passive investor should price in before assuming the higher yield.

Jackson: a different market entirely

Jackson, in Teton County, is where Wyoming's statewide median gets distorted from. Typical home values there run near $1.93 million, roughly six times the statewide figure, driven by proximity to Grand Teton National Park and a buyer pool of second-home owners and short-term rental operators rather than local W-2 wages. A 25% down payment on a typical Jackson property is nearly $483,000 on its own, larger than the entire purchase price in Casper. Standard buy-and-hold DSCR underwriting simply doesn't apply here; Jackson is a short-term-rental and long-horizon appreciation market, not a passive cash flow market, and treating it as one will produce a number so far outside the rest of the state's math that it isn't a useful comparison point.

The verdict for Wyoming investors

None of Wyoming's three largest ordinary markets produce positive cash flow for a buy-and-hold investor at 25% down and 6.43% rates today. Casper's lower price makes it the smallest monthly loss of the three; Cheyenne offers the steadiest tenant base through its Air Force base; Laramie likely has the most underpriced true income once student-by-the-bedroom rents are counted, at the cost of active management. Wyoming's zero income tax, zero capital gains tax, and sub-0.55% property tax are all genuinely durable advantages that will compound every year a property is held, the same pattern confirmed across several no-income-tax states this year. But as in Tennessee, Texas, South Dakota, and Utah before it, a favorable tax code doesn't by itself turn a negative-cash-flow property positive.

The math points toward larger down payments or below-median entry prices for anyone determined to make a Wyoming deal cash flow today, and toward treating the tax savings as a bonus that improves the return on an already-viable deal rather than as the reason to buy one that doesn't work on its own. If you're weighing Wyoming against another zero-income-tax state, the Texas investor math and the South Dakota cash flow breakdown are the closest points of comparison already published on this site, and both reach a similar conclusion: the tax code and the price-to-rent ratio are two separate questions, and only one of them determines whether the deal actually pays you.

With Wyoming's spotlight now published, this completes coverage of all 50 states. Anyone comparing a specific market against one already covered here can use the West Virginia, Wisconsin, or any earlier state breakdown as a like-for-like reference point using the same 25% down, current-rate underwriting throughout.