Two rental properties into your Texas portfolio, you've learned to run the DSCR math before you fall for a "cheap Midwest market" pitch, and Wisconsin gets pitched a lot: affordable prices, stable population, no coastal climate risk. The pitch skips the part that actually decides whether a deal works: what rent a property earns against what it costs to carry at 6.43%. Run that math across the state's three largest markets and the answer is narrower than the pitch suggests.

Milwaukee is the one market that clears the lender's break-even line. Madison, despite having the best rents in the state, does not. Green Bay does not either. Here is the full breakdown, city by city.

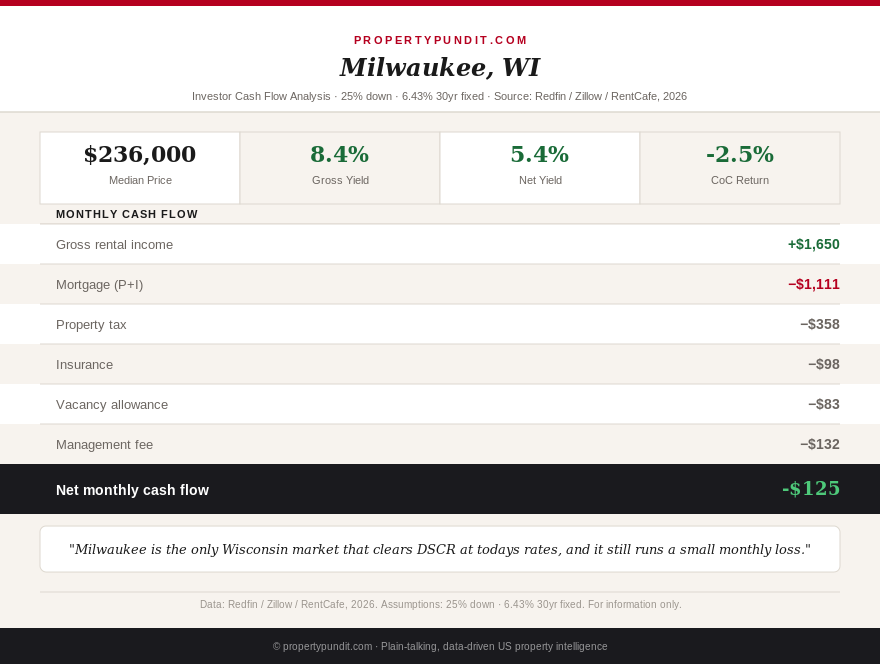

Milwaukee: the only market that clears DSCR, and only barely

Milwaukee's median home sale price runs around $236,000 (Redfin, three months ending May 2026), with a typical 3-bedroom single-family rental earning approximately $1,650 a month, notably higher than the citywide apartment-index average of roughly $1,319 that most quick searches surface (Zillow, RentCafe, 2026). At 25% down and 6.43%, the $177,000 loan carries a principal-and-interest payment of $1,111 a month. Add Milwaukee County's property tax, among the highest in the state at an effective 1.82%, at roughly $358 a month, plus an estimated $98 in insurance, and PITIA comes to $1,567.

Against $1,650 in rent, that is a DSCR of 1.05, clearing the 1.0 minimum most DSCR lenders require for qualification. Once you subtract a realistic 8% management fee and a 5% vacancy allowance, though, effective cash flow lands at roughly negative $125 a month. So what this means for you: Milwaukee is the rare Wisconsin market where a deal can actually qualify for DSCR financing, but qualifying and cash-flowing are two different tests, and this one only clears the first.

Madison: the best rents in the state still are not enough

Madison is the counterintuitive case. Three-bedroom single-family rentals here command roughly $2,515 a month, genuinely the strongest rent figure of any Wisconsin market and well above what most first-time investors expect from the Midwest (apartment and single-family rental listings, 2026). But Madison's median home price has run up to approximately $440,000 (Redfin, three months ending May 2026), driven by University of Wisconsin and state government employment demand pushing against a tightly constrained housing supply.

At 25% down and 6.43%, the $330,000 loan carries a $2,071 monthly principal-and-interest payment. Dane County's property tax runs close to 1.69% effectively, adding about $620 a month, plus an estimated $183 in insurance, for a PITIA of $2,874. Against $2,515 in rent, DSCR comes in at 0.88, meaningfully below the 1.0 threshold, and cash flow after management and vacancy runs roughly negative $676 a month. So what this means for you: Madison proves that strong rent alone does not make a deal work. Purchase price relative to that rent is what decides the math, and Madison's price has simply outrun what even its best-in-state rents can support.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Green Bay: cheaper than Madison, still fails the same test

Green Bay's median home price sits around $273,000, up 4.6% year over year (Redfin, February 2026), roughly 38% below Madison's median. A comparable single-family rental earns an estimated $1,400 a month, scaled up from the citywide apartment average of $1,084 the same way Milwaukee's true SFR rent runs ahead of its own apartment index. At 25% down and 6.43%, the $204,750 loan carries an $1,285 monthly principal-and-interest payment. Brown County property tax at roughly 1.75% effective adds about $398 a month, plus an estimated $114 in insurance, for a PITIA of $1,797.

Against $1,400 in rent, DSCR lands at 0.78, the weakest of the three markets, with cash flow after management and vacancy running roughly negative $573 a month. So what this means for you: Green Bay's lower entry price does not translate into better cash flow, because its rent base is proportionally even further behind its purchase price than Milwaukee's or Madison's. Cheaper is not the same as better math.

The income tax bill is real, but it is not the reason Wisconsin fails

Wisconsin taxes rental income under a graduated personal income tax schedule running from 3.50% to 7.65% depending on total taxable income (Wisconsin Department of Revenue, 2026). That is a genuine ongoing cost for an out-of-state investor and worth modeling into any pro forma, but it is not the reason these three markets struggle to cash flow. Compare it against Minnesota's income tax, among the highest in the country, or against Michigan's non-homestead property tax structure, and Wisconsin's overall tax burden on a rental property is closer to the middle of the Midwest pack than an outlier in either direction.

The real constraint across all three Wisconsin markets is the same one that shows up nationally in 2026: purchase prices have moved further from rents than a 6.43% mortgage rate can support without a meaningful down payment cushion or a genuinely underpriced entry point. So what this means for you: do not rule Wisconsin out because of its tax code, and do not assume it works because of the "affordable Midwest" reputation either. Underwrite the specific property against its specific rent, the same way this article just did for all three cities, before you assume the state-level story tells you anything about a single deal.

Put the three markets together and the pattern is consistent with what Texas's own price-to-rent divergence has been showing all year: Milwaukee is the only Wisconsin market that clears DSCR today, and it does so with only a modest monthly loss once real operating costs are included. Madison's superior rents cannot outrun its superior price. Green Bay's lower price cannot make up for its proportionally weaker rent base. The math points toward Milwaukee specifically if Wisconsin is on your shortlist at all, and toward waiting on Madison and Green Bay until either prices soften or rents catch up; most investors who run these three numbers side by side end up passing on all but the Milwaukee deal. For a framework on how to underwrite any of these three deals properly before making an offer, the DSCR loan investor guide and the county-level SFR yield map are the two most useful starting points, and if a Milwaukee deal looks close on paper, run the numbers again with a real insurance quote before assuming the state's estimated averages match your specific ZIP code.