West Virginia keeps showing up in "cheapest states to buy a house" lists, and after two properties in Texas, you've learned to distrust that kind of headline on sight. Cheap median prices usually mean cheap rents to match, or a population that is leaving faster than you can fill a vacancy. The question that actually matters isn't whether West Virginia is affordable. It is whether the numbers still work once you run a real mortgage payment against a real rent check at today's rates.

They mostly don't, and the reason is more specific than "rates are high everywhere." Here is the state broken down by the three markets that come up most often, plus a measurement quirk in the headline price that changes how you should read every "cheapest state" list you see next.

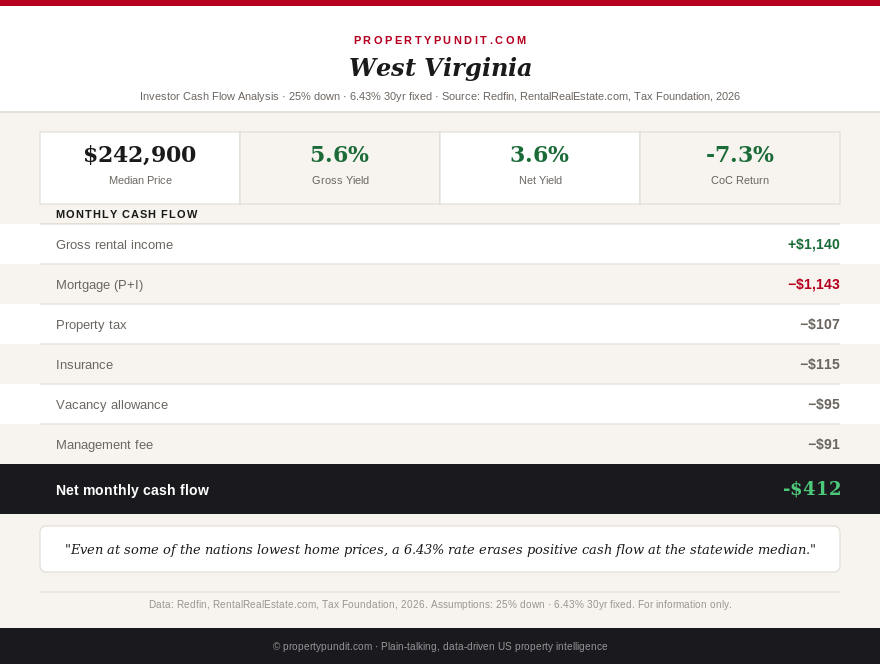

The state median hides two very different price tags

Redfin puts West Virginia's statewide median sale price at $242,900 in 2026, up 3.9% year over year. Zillow's home value index, a smoothed estimate covering the full housing stock rather than just homes that recently sold, puts the average value at $178,719, up a more modest 2.2% (Zillow, May 2026). That is a $64,000 gap between two numbers people casually swap for each other.

The reason is methodology, not a typo. Redfin's median reflects actual closed transactions, which in a low-volume state like West Virginia skew toward the counties and homes that trade most often, typically pricier and closer to population centers. Zillow's index estimates value across every home in the state, including the tens of thousands in declining rural counties that rarely change hands at all. So what this means for you: when a listicle tells you a state is the cheapest in America, check whether the number is a sale-price median or a value index before you use it to size up a deal, because the two can disagree by 25% or more in a thin market.

Martinsburg: the fastest-growing county still doesn't clear breakeven

Martinsburg anchors Berkeley County in the Eastern Panhandle, the one part of West Virginia genuinely growing, up 13.7% in population over the past five years as commuters priced out of the DC and Northern Virginia markets push west along I-81 (U.S. Census Bureau county estimates, 2026). The median sale price here is $283,005, up 3.5% year over year (Redfin, May 2026), and typical single-family rent runs around $1,350 a month.

Run the math at 25% down and 6.43%: principal and interest on the $212,254 loan comes to roughly $1,332 a month, plus about $125 in property tax at the statewide effective rate of 0.53% and an estimated $120 in insurance. That is a PITIA of about $1,577, against $1,350 in rent, a DSCR of 0.86. After an 8% management fee and a vacancy allowance, cash flow lands around negative $400 a month. So what this means for you: the commuter growth story is real and it is the best appreciation case in the state, but at today's price and rate, Martinsburg is a bet on rising values, not a property that pays you monthly while you wait.

Charleston: cheap by national standards, still underwater

The state capital carries the state's largest employer base, government jobs plus a concentration of legal and healthcare work, and Kanawha County's 0.63% effective property tax rate is the highest in West Virginia (Tax Foundation, 2026). At the $220,000 city median with 25% down, principal and interest runs about $1,035 a month, plus roughly $116 in property tax and an estimated $110 in insurance, a PITIA near $1,261. Typical rent in Charleston runs around $1,050 a month (RentCafe, Zillow, 2026), putting DSCR at 0.83 and cash flow, after management and vacancy, at roughly negative $350 a month.

So what this means for you: Charleston's government employment base genuinely lowers your vacancy risk relative to most of the state, but lower risk doesn't show up as a smaller monthly loss on the cash flow line. If you're underwriting Charleston, you're paying for stability, not yield.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Morgantown: the citywide rent number that doesn't tell the real story

Morgantown, home to West Virginia University, posts a median sale price of roughly $255,000, up anywhere from 4% to 12% year over year depending on the month sampled (Redfin, 2026). Zillow lists typical monthly rent at just $888, about 34% below the national median. Run that against a $255,000 purchase, and the math is the worst of the three: a PITIA near $1,408 against $888 in rent is a DSCR of 0.63, meaningfully underwater even before management fees.

But that citywide rent figure almost certainly understates what an actual house near WVU earns, because it blends small studio and one-bedroom apartment stock with the classic college-town product: a four- or five-bedroom house leased by the room to students on nine-month academic-year terms, which experienced Morgantown landlords use to generate meaningfully higher effective rent per property than the city average implies. The tradeoff is operational, not just financial. By-the-bedroom student housing means more tenant turnover, more move-in and move-out coordination every August, and none of the passive, one-lease-a-year simplicity that a DSCR-loan buyer typically wants. So what this means for you: Morgantown punishes the investor who prices a deal off the Zillow city average and buys sight unseen, and it can reward the investor willing to operate a student rental hands-on. Those are two different businesses wearing the same ZIP code.

The tax cut is real. The population trend is the offset.

West Virginia cut its top personal income tax rate for the third consecutive year in 2026, from 4.82% to 4.58%, effective retroactively to January 1 (W.Va. Code Section 11-21-4j, codified June 12, 2026). That is a genuine, durable cost advantage against high-tax states where rental income gets taxed at 8% or 9% or more, and it compounds every year you hold a property here.

Set against that: West Virginia posted the largest five-year population decline of any US state, roughly 1.4%, driven overwhelmingly by deaths outpacing births rather than people moving out (West Virginia Center on Budget and Policy, U.S. Census Bureau estimates, 2026). Only eight of the state's 55 counties grew over that period, and the losses are steepest in the southern coalfields, where McDowell County fell 11.8% and Mingo County fell 9.8%. That decline isn't evenly distributed, Berkeley County is the clear exception, but it means a lower state-average tax bill has to be weighed against a shrinking long-run tenant pool in most of the state's counties. So what this means for you: the tax advantage is real money in your pocket every year, but it doesn't offset a market where population, not price, determines whether you've a tenant in five years.

Put the three markets together and the pattern is consistent: West Virginia's headline affordability isn't a myth, prices genuinely are among the lowest in the country, but at a 6.43% mortgage rate, cheap purchase prices and cheap rents move together, and neither Martinsburg's growth story, Charleston's employment stability, nor Morgantown's student-housing niche produces positive cash flow using standard, passive underwriting. The math points toward treating West Virginia as an appreciation and tax-efficiency play in Martinsburg specifically, or an active, hands-on student-housing operation in Morgantown, and toward skipping the state entirely if what you actually want is a property that cash flows the day you close. For a fuller framework on how to underwrite a deal like this before you make an offer, the DSCR loan investor guide and the county-level SFR yield map are the two most useful starting points, and if you're weighing whether to manage a property like a Morgantown student rental yourself, the real cost of an 8% management fee is worth reading before you decide. For a comparison against a neighboring low-tax Appalachian market, Pennsylvania's 3.07% flat income tax and Pittsburgh's positive cash flow is the closest available benchmark, and for a look at how military demand changes the math in a neighboring state, see Virginia's Navy-base investor math.