You've already run the numbers on a mainland rental and watched them fail. Now you're looking at Hawaii, because the postcard logic says land is fixed, tourists keep coming, and prices only go one direction. Here's the number that logic runs into: Oahu's single-family home median hit a record $1,262,500 in June 2026, according to the Honolulu Board of Realtors, and at today's 6.55% rates, not one entry point in the state, including the cheapest one, produces a genuinely positive monthly cash flow.

Hawaii's condo market tells a similar story at a lower price. The statewide condo median rose 4% year over year to $528,000 in June 2026. That's the more realistic entry point for most out-of-state investors, since a $1.26 million single-family home is out of reach for the large majority of buyers reading this. But affordable relative to Oahu's houses doesn't mean affordable in absolute terms, and it doesn't mean the math works once you add HOA fees and Hawaii's excise tax on top of the mortgage.

Start with what a 25% down, 6.55% loan actually looks like on a median Honolulu condo. On $528,000, the loan amount is $396,000 and principal and interest run $2,516 a month. Add $176 in property tax, a $700 HOA fee (typical for a full-service Oahu condo building), and $130 in insurance, and PITIA reaches $3,522. Against a realistic $2,700 monthly rent, and after Hawaii's General Excise Tax takes 4.5% off the top of that rent before you see a dollar of it, the property runs roughly $1,295 a month underwater once you subtract property management and a vacancy allowance. That's not a rounding error. It's the difference between a rental that supports itself and one that requires a standing subsidy from your other income every single month.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Oahu's single-family math is worse, not better

A $1,262,500 Oahu single-family home at 25% down carries a $946,875 loan, with principal and interest of $6,016 a month. Honolulu's Residential A property tax structure is genuinely competitive, 0.40% on the first $1 million of assessed value and 1.14% above that, working out to roughly $583 a month here. Add $220 in insurance and PITIA reaches $6,819. Against a $3,500 monthly rent, and after the same 4.5% excise tax, this property loses close to $3,930 a month once management and vacancy are factored in. That's a bigger monthly loss than most mainland investors carry as a total mortgage payment, on a single unit.

The takeaway isn't that Oahu real estate is a bad long-term bet. Fixed land supply and a captive tourism and military economy are real, durable demand drivers. The takeaway is that you should never evaluate an Oahu single-family purchase on a cash-on-cash or cap-rate basis, because the number will always look catastrophic. This only makes sense as a decades-long appreciation and equity play, funded by income you're bringing from somewhere else.

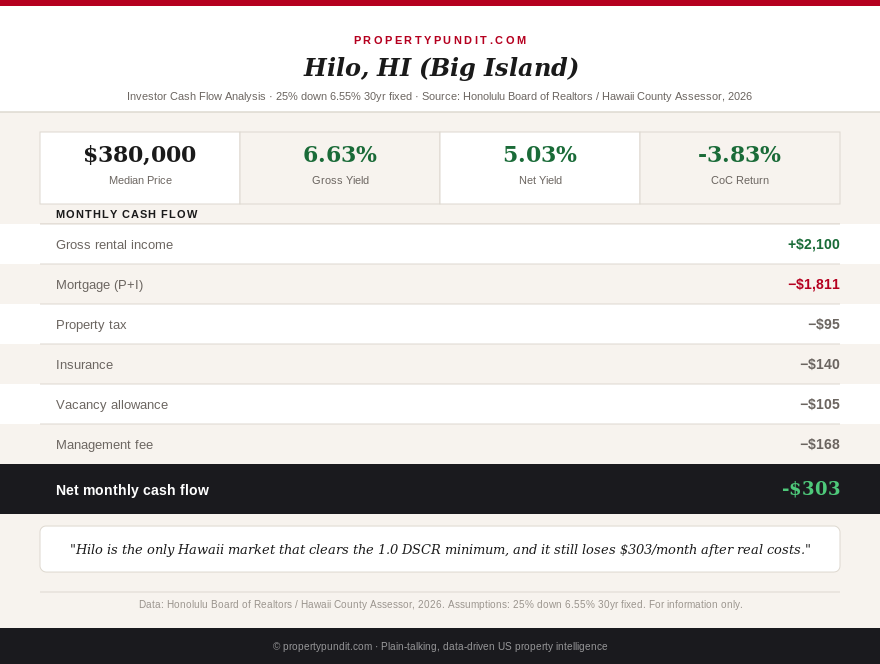

Big Island Hilo is the closest thing to a real number

At roughly $380,000, Hilo on the Big Island is Hawaii's most realistic entry point for an investor who actually wants the numbers to work. A 25% down, 6.55% loan runs $1,811 a month in principal and interest, plus about $95 in property tax at the Big Island's lower roughly 0.30% rate, plus $140 in insurance, for a PITIA of $2,046. Against a $2,100 rent and the neighbor islands' lower 4.0% excise tax rate, gross rent alone clears a 1.03 debt service coverage ratio, technically passing the 1.0 minimum most lenders require.

But passing DSCR and generating positive cash flow are two different tests. Once you subtract an 8% property management fee and a realistic vacancy allowance, Hilo still runs about $303 a month negative. This is the same pattern we've flagged in Vermont and Colorado this year: a property can clear the lender's minimum ratio and still cost you money every month once you account for the actual cost of owning and managing it. Hilo is the best Hawaii has to offer an investor chasing cash flow, and it still isn't one.

The tax picture people get backwards

Hawaii has no traditional sales tax, and that leads some investors to assume it's a low-tax state across the board, the same mistake people make with Delaware. It isn't. Hawaii's income tax is graduated up to 11%, one of the highest top marginal rates in the country, and it applies in full to rental income with no special carve-out. On top of that, the General Excise Tax, 4.5% on Oahu and 4.0% on the neighbor islands, is charged on gross rental revenue before you deduct a single expense. A mainland investor comparing Hawaii's "no sales tax" headline against a state like Nevada or Texas is comparing the wrong line item entirely.

If you're underwriting a Hawaii property against a no-income-tax state, run the full after-tax comparison, not just the property tax line, before you decide the postcard math beats the mainland math.

What SB 2539 would change, and why it hasn't yet

Senate Bill 2539, introduced in Hawaii's legislature in January 2026, would establish the state's first rent stabilization law, capping annual increases at 3% and barring any increase in a tenant's first 12 months. As of this writing, it had been referred to committee but had not passed into law. Hawaii still has no rent control at either the state or county level, which is a genuine advantage for landlords navigating rents that already outrun most tenants' incomes without needing a legislative ceiling.

Watch this bill regardless of whether you're buying this year. If it returns and passes in a future session, it would cap your rent-growth assumption on any long-hold Hawaii property, which matters more here than almost anywhere else given how far current cash flow already runs negative.

The verdict

No Hawaii market, not Oahu condos, not Oahu single-family homes, not Big Island Hilo, produces positive investor cash flow at 6.55% rates and 25% down in mid-2026. Hilo is the closest, technically clearing DSCR before real-world costs, but still a monthly loss once you run the full expense stack. If you're buying in Hawaii as an investor, the math points toward doing it as a pure appreciation and land-scarcity play funded by outside income, not as a cash-flow asset, and sizing your down payment and reserves around carrying a multi-hundred-dollar monthly loss for as long as you hold. Most investors who run these numbers honestly end up either passing entirely or buying with a 40%+ down payment specifically to shrink that monthly gap to something they can comfortably absorb for a decade or more.

For a full walkthrough of how debt service coverage ratio loans are underwritten, see our DSCR loan investor guide, and for county-level yield data across the mainland, our SFR yield county map is a useful comparison point against Hawaii's numbers here. If a condo is on your shortlist, our look at how a single special assessment can wreck a DSCR loan applies directly to Oahu's HOA-heavy condo stock. And if you're weighing Hawaii against another high-price, low-cash-flow state, our recent California spotlight found the same pattern playing out at a lower price point.