You've found a condo that pencils. The gross rent covers the mortgage, the cap rate looks like 6.8%, the neighborhood is solid, and the photos are clean. Then you request the HOA financials.

The reserve study is two years old. The current balance is $42,000. The study says the association needs $310,000 to be fully funded. The president of the board assures you they've "always managed fine." Three months after closing, the association votes a $15,000 special assessment: $500 a month for 30 months: to replace the failing roof and the aging elevator.

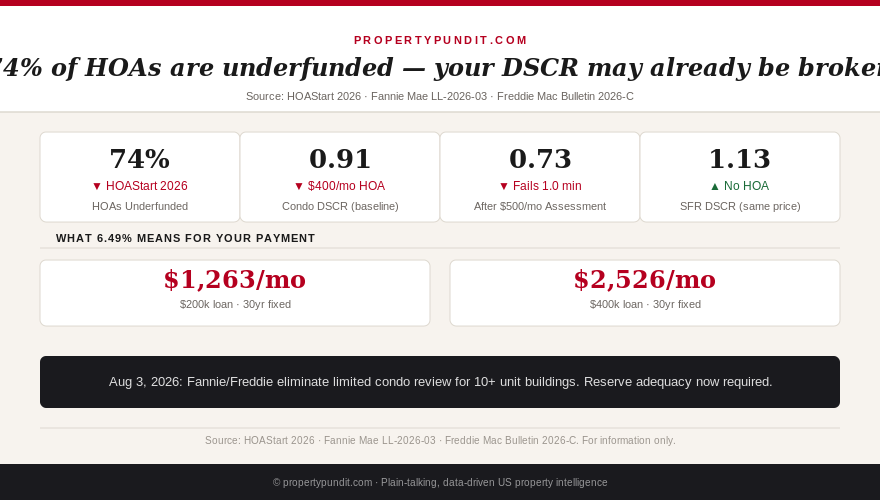

Your $1,900-a-month rent hasn't changed. Your mortgage, taxes, and insurance haven't changed. But your DSCR just collapsed from 0.91 to 0.73, and if you'd bought this property with a DSCR loan, your lender would be calling.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

This isn't a fringe scenario. According to HOAStart's 2026 analysis of more than 100,000 reserve studies, approximately 74% of HOA associations in the United States are underfunded relative to established benchmarks. Roughly one in three sits below 50% funded: a threshold the Community Associations Institute considers critically underfunded. And 35% of associations say they expect to issue a special assessment within the next five years.

If you're a landlord with condo exposure, or evaluating condos for your next acquisition, this is your number: 74%. Three in four HOAs you look at will have a reserve shortfall. The question is how bad, and whether the shortfall is heading toward your deal.

How DSCR lenders treat HOA dues and special assessments

Before getting into the reserve crisis, it helps to understand exactly how HOA costs interact with DSCR qualification. DSCR (debt-service coverage ratio) is the primary metric DSCR loan lenders use to evaluate rental property financing. The formula is simple: gross monthly rent divided by PITIA.

PITIA stands for principal, interest, taxes, insurance, and association dues. That last element is the one most condo buyers underestimate. Every dollar of HOA dues goes into the denominator, not the numerator. A $400/month HOA doesn't just "come out of cash flow": it directly reduces your DSCR ratio and therefore your ability to qualify for financing.

Here's the math on a typical condo deal at current rates. A $285,000 condo purchased at 25% down ($71,250) leaves a $213,750 loan. At 6.49% over 30 years, the principal and interest payment is $1,350 per month. Add property taxes of $238/month (assuming 1.0% effective rate) and insurance of $100/month, and you're at $1,688 PITI before the HOA.

A $400/month HOA brings the PITIA total to $2,088. At $1,900 gross monthly rent, the DSCR is $1,900 / $2,088 = 0.91. Most DSCR lenders require a minimum of 1.0; preferred tier pricing requires 1.25. This deal already fails the minimum before a single dollar of special assessment lands.

The SFR comparison at the same price point illustrates the structural issue. A $285,000 single-family home with no HOA has PITI of $1,688. At $1,900 rent, DSCR is $1,900 / $1,688 = 1.13. It clears the 1.0 minimum, though it still falls short of the 1.25 preferred tier. The $400/month HOA alone is the difference between a fundable and an unfundable deal.

That's the baseline. Now add a special assessment.

When a special assessment is billed monthly or is expected to continue for a defined period, DSCR lenders include it in the PITIA calculation alongside regular dues. On the condo above, a $500/month assessment brings PITIA to $2,588. DSCR: $1,900 / $2,588 = 0.73. That's not just below the 1.0 minimum: it's in the range where most lenders won't even finish the underwrite. The deal that looked marginal before closing has become unfinanceable after.

If you already own the property and are trying to refinance into a DSCR product, the situation is the same. The lender underwrites what's on the books at the time of closing, not the dues before the assessment. So existing owners can find themselves locked out of refinancing a property they've held for years because the HOA voted a special assessment in Q1 of the same year.

The math says: to qualify at DSCR 1.25 with a $400 HOA and $500 assessment, you'd need gross monthly rent of $3,235 on a $285k purchase: a gross yield of 13.6%. That doesn't exist in any mainstream US market. The deal structure is broken at the start.

Why the reserve crisis is getting worse, not better

HOA underfunding isn't new, but two forces are making it worse in 2026. The first is deferred maintenance that accumulated during the pandemic years, when boards routinely voted to "waive" reserve contributions to keep monthly dues stable. The second is the post-Surfside legislative wave in Florida, which mandated full structural inspections and reserve funding for all condo buildings three stories or taller.

The 2021 Surfside collapse, which killed 98 people when Champlain Towers South partially failed, revealed the consequence of decades of underfunded reserves and deferred maintenance. Florida's legislative response exposed the same pattern in buildings across the state. Individual special assessments in Florida high-rise condos have reached six figures per unit. HOA fee increases of 16% or more year-over-year have become common in major Florida metros as boards scramble to comply.

The structural problem is this: special assessments are uniquely difficult to forecast. Unlike monthly HOA dues, which increase predictably, a special assessment can arrive as a lump sum or a multi-year billed charge with almost no warning. A reserve study three years old tells you almost nothing about what the board voted last month. And boards are legally permitted to issue assessments without owner consent in most states.

For investors, this means the due diligence window matters enormously. The time to learn about reserve shortfalls is before the offer, not after closing. You can request the reserve study, the most recent two years of financial statements, and the last 12 months of board meeting minutes. Board minutes often reveal planned assessments, structural concerns, or pending litigation before they appear anywhere else. A seller's disclosure obligation doesn't always extend to a reserve shortfall that hasn't yet become a formal assessment vote.

When you get the reserve study, the key number is the percent funded. Below 70% is considered underfunded by the Community Associations Institute. Below 30% is critically underfunded: a significant assessment is a matter of when, not if. Any building with deferred major repairs: roof, elevators, HVAC, pool systems: that appears in the reserve schedule within the next three to five years deserves extra scrutiny.

The internal links to the HOA fees investor cash flow analysis and the DSCR loan investor guide cover the baseline fee modeling; this article focuses specifically on the reserve risk layer that sits on top of it.

The Fannie/Freddie rule change that takes effect August 3

The reserve crisis got a federal policy response in March 2026, when Fannie Mae and Freddie Mac announced significant changes to condo underwriting standards. These changes don't affect DSCR loan products directly: DSCR loans are non-QM products not governed by agency guidelines: but they matter for any investor who plans to sell to an owner-occupant buyer or refinance into a conventional product later.

Effective August 3, 2026, lenders can no longer use the streamlined limited review pathway for condos in projects with more than 10 units. Every condo loan in those projects requires full project review, which means the lender must verify reserve study documentation, recent financials, and the adequacy of the association's reserve funding. Buildings that can't produce this documentation, or whose reserves fall significantly below recommended levels, will not be eligible for Fannie Mae or Freddie Mac-backed financing.

This matters for investors in two ways. First, it makes it harder to sell condos in underfunded buildings to owner-occupant buyers who need conventional financing. A building with reserves at 25% funded may simply lose access to the largest pool of buyers in the country. Second, starting January 4, 2027, associations must allocate at least 15% of annual budgeted assessment income to replacement reserves: up from the prior 10% requirement. Buildings that haven't started increasing dues to meet this threshold will face either mandatory dues increases or financing restrictions.

The practical effect: if you're buying a condo today in a Sun Belt building that hasn't yet disclosed its reserve status, you're buying into uncertainty about both your financing and your eventual exit. The August 3 change doesn't give you a warning: it's the hard enforcement date.

When a condo still makes sense for investors

The data doesn't say avoid all condos. It says price the reserve risk into the deal.

A condo association that's 80% funded or better, with stable dues that have been increasing gradually, no major deferred items within the next five years, and no history of one-off special assessments is a very different risk profile from a building at 22% funded with a 15-year-old roof and a pending elevator replacement. You can own the first type with reasonable confidence. The second type is an unquantified liability, and you shouldn't close without understanding it.

The due diligence checklist for any condo acquisition should include: the most recent reserve study, the percent funded figure, the five-year repair schedule, two years of financial statements, board meeting minutes for the past 12 months, and a conversation with the property manager about any pending votes. If any of these are unavailable or the seller is uncooperative in providing them, that's your answer.

For DSCR loan buyers specifically, the math says the HOA dues have to leave room for the assessment risk. If you're already at DSCR 0.91 at standard dues, there's no buffer. The deal should pencil at 1.25 or better on existing dues before you factor in what might hit next year. The properties that still work in a condo format in 2026 tend to be in buildings with newer construction, lower HOA fees, and documented reserve health: not the 1990s-era Sun Belt towers where the Surfside-era accounting is now catching up.

The SFR yield county map shows which markets offer comparable returns in single-family product without the HOA layer. For investors who want the lower entry price that condos can offer, the Indiana market analysis and the Kansas investor breakdown both show SFR cash-flow markets at entry prices in the $175,000 to $235,000 range: price points that compete with condo entry and without the reserve exposure.

What this means for your next acquisition

The math points toward one clear rule: if you're acquiring with a DSCR loan, or plan to exit via DSCR refinance, the HOA dues and reserve health aren't a footnote: they're underwriting variables. A condo deal that passes on gross yield but sits in a building with 30% reserve funding is a deal that could fail at closing, fail at refinance, or fail at exit when your buyer can't get conventional financing.

Frankly, if you're building a rental portfolio and you're not a specialist in a specific building or market, the SFR default makes more financial sense right now. The premium you pay in acquisition price on an SFR is real, but the DSCR headroom you get back: because there's no HOA eating into the denominator: is also real. You can't predict when a board is going to vote a $500/month assessment. You can predict that 74% of HOA associations are underfunded and that the math runs against you when one does.

If you already hold condo units, this is the time to request the current reserve study from your association and verify the funded percentage. If it's below 50%, start modeling the cost of a potential assessment into your hold-versus-sell calculation before August 3 tightens the buyer pool for your eventual exit.