You wrote California off a while ago. Two properties into a portfolio built on Sun Belt yield spreadsheets, the coastal numbers never came close to working, so the entire state got filed under "appreciation only, skip it." That verdict was probably right for the coast. It's worth checking again on the two Central Valley cities that used to be the counterargument, because rates have moved since the last time anyone ran this math, and the answer isn't what it used to be.

Here's the state's headline number, the property tax mechanic that changes how you should think about a loss, and an updated look at whether Fresno and Bakersfield still deserve their reputation as California's investor exception.

The number that makes California look impossible

California's statewide median resale price hit $930,260 in May 2026, up 2.3% from April and a fresh record for the series (California Association of Realtors, June 17, 2026). Redfin's broader measure, which counts all closed sales rather than the realtor-reported resales C.A.R. tracks, put the state median at $782,221 for the same month, up 2.3% year over year. Both numbers are real. They measure different things: C.A.R.'s figure skews toward the higher-priced single-family resale market, while Redfin blends in condos, new construction, and lower-cost inventory across the state.

So what this means for you: if you're underwriting off the statewide headline, you're modeling a market that barely exists outside a handful of coastal counties. The real investor conversation in California happens $400,000 to $500,000 lower than either statewide number, in the Central Valley.

Prop 13's hidden edge for a patient investor

Proposition 13 sets the base property tax rate at 1% of assessed value, but a new purchase gets reassessed to the current sale price, and once local bonds, parcel taxes, and other assessments are layered on, the effective rate on a fresh purchase typically lands between 1.1% and 1.25%. The part that matters for a hold strategy is what happens next: the assessed value can only grow 2% a year regardless of how much the property's actual market value rises, and it resets to full market value only when ownership changes. Rent, by contrast, tends to grow 3% to 4% a year in most California metros. That gap compounds every year you hold, so a Fresno property with a DSCR of 0.94 in year one on the numbers below has a real path to DSCR above 1.0 within a few years, purely from the tax side, assuming rent keeps pace with its historical trend.

So what this means for you: a negative cash flow number on day one isn't automatically a reason to pass on a California deal the way it would be almost anywhere else. It's a reason to model year five and year ten before you decide, because Prop 13 is quietly working in your favor the entire time you hold.

Fresno and Bakersfield: the "affordable" plays, retested

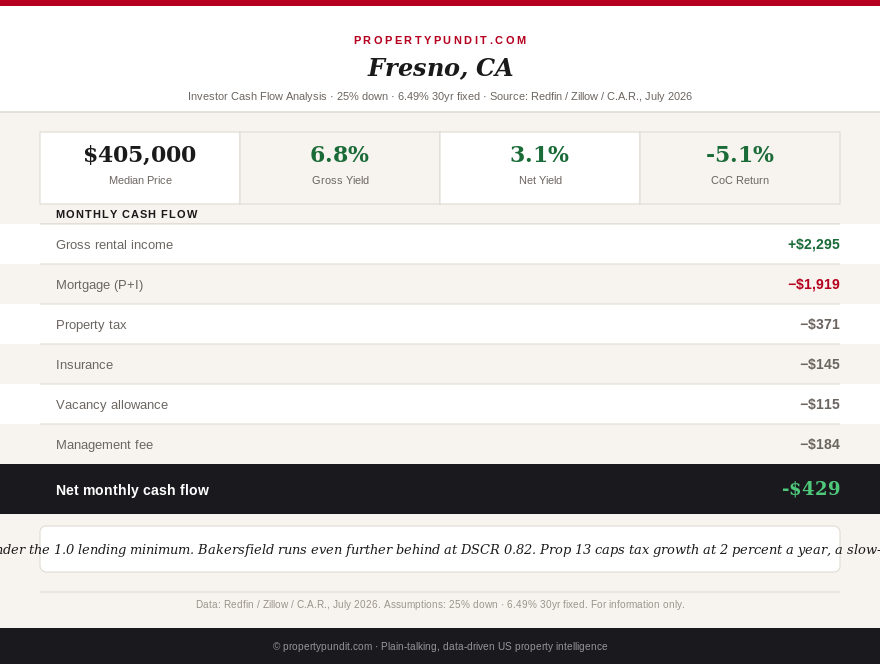

Fresno's median sale price is $405,000 over the three months ending May 2026 (Redfin), with three-bedroom single-family rent averaging $2,295 a month (Zillow Rental Manager, 2026). At 25% down and 6.49%, the $303,750 loan carries principal and interest of about $1,919 a month. Add roughly $371 in property tax at a new-purchase effective rate of 1.1%, plus an estimated $145 in insurance, and PITIA comes to about $2,435. Against $2,295 in rent, that's a DSCR of 0.94, just under the standard 1.0 lending minimum. After an 8% management fee and a vacancy allowance, cash flow lands around negative $429 a month.

Bakersfield's median is $418,000, with three-bedroom rent averaging $2,058 a month (RentCafe, 2026). The $313,500 loan at 6.49% runs about $1,980 a month in principal and interest, plus roughly $383 in property tax and an estimated $150 in insurance, for a PITIA near $2,513. That puts DSCR at 0.82, weaker than Fresno, and cash flow after management and vacancy at about negative $714 a month.

Both cities still post the highest gross rental yields of any major market in California, and both remain far closer to breakeven than Los Angeles, San Francisco, or San Diego, where coastal prices make positive cash flow essentially impossible at any reasonable down payment. But at today's rates, neither Fresno nor Bakersfield is the cash-flow-positive exception the state's affordability reputation implies. So what this means for you: if your plan depends on immediate positive cash flow, California doesn't have a market that delivers it right now, full stop, including its cheapest metros.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The DSCR loan detail most investors miss

Everything above assumes financing at the general 30-year fixed benchmark of 6.49%. Investors using a dedicated DSCR loan program, the type of no-income-verification financing many out-of-state and portfolio buyers actually use, are currently quoted 7.15% to 8.75% in California as of April 2026, well above the conventional owner-occupant rate. Run either Fresno or Bakersfield at the midpoint of that range instead of 6.49%, and the monthly loss on both properties widens by another $150 to $300, since a higher rate pushes more of each payment toward interest. So what this means for you: if you're financing through a DSCR product rather than a conventional loan, the negative cash flow figures above are closer to a best case than a realistic one, and you should re-run the math at your actual quoted rate before making an offer.

Make the call

The math points toward treating Fresno and Bakersfield as appreciation-and-tax-efficiency holds rather than income properties, at least until rates come down meaningfully from 6.49%. Prop 13's 2%-a-year assessment cap is a genuine, compounding advantage that most other states can't offer an investor, and it's the strongest argument for holding through a negative cash flow year rather than passing on California entirely. If immediate positive cash flow is the priority, the numbers here say to look outside the state for now; for a sense of how other low-cost markets currently compare, the county-level SFR yield map and the DSCR loan investor guide are the two best places to start. Before financing any deal with a DSCR product, it's also worth reading how management fees compound against a thin cash flow margin, since an 8% fee is rarely the full cost once leasing charges are included.