You have done the math more than once. Take your income, subtract rent and the car payment and everything else, and the number left over for a down payment fund is smaller than you would like to admit out loud. Every article you read says the same thing: save 20% down so you avoid mortgage insurance and get the best rate. So you open a savings account, set up an automatic transfer, and start waiting. If that is where you're right now, a new study just put a number on how long that wait actually is, and it's worse than most people guess.

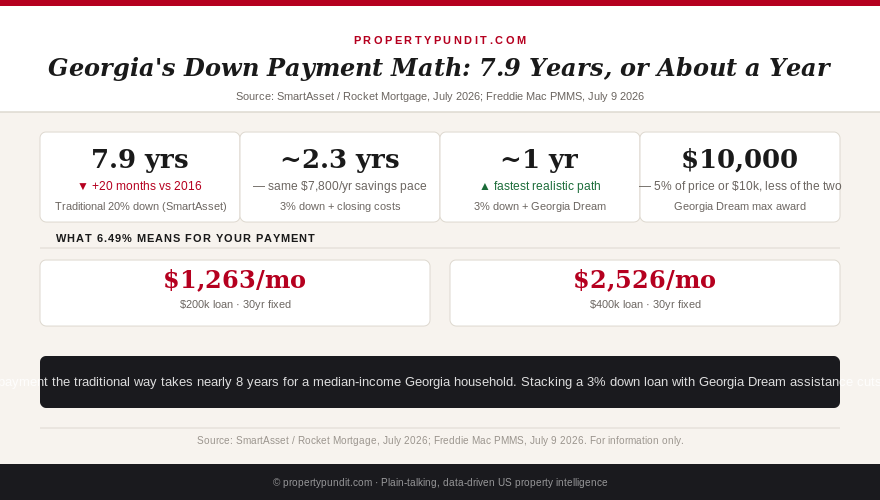

A median-income household in Georgia now needs 7.9 years to save a 20% down payment, according to a SmartAsset analysis published July 10, 2026. That is 20 months longer than the same calculation in 2016. The typical Georgia home value jumped from $166,473 to $333,559 over that decade, essentially doubling, while median household income rose from $53,559 to $84,344, not nearly enough to keep pace. The study assumes a household sets aside 10% of its income every year toward the down payment, with no adjustment for investment returns along the way.

If you earn closer to $78,000, the picture looks similar in shape even if the exact numbers shift. On a $300,000 starter home in the Atlanta metro, a 20% down payment is $60,000. Saving 10% of a $78,000 income puts $7,800 a year into that fund, which means about 7.7 years before you have enough to write the check. That is nearly eight years of rent payments, moving trucks you don't control the timing of, and watching home prices climb while you wait. The good news: that 7.7-year number describes a path almost nobody actually takes.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why the "save it yourself" number is worse than it looks

The 7.9-year figure isn't an outlier. A separate Rocket Mortgage analysis of 49 major metro areas found a typical household needs 65.2 years to save the median first-time buyer down payment in New York City, 41.5 years in Los Angeles, and 37.8 years in Boston. On the other end, Detroit comes in at 3.9 years and Warren, Michigan at 3.1 years. Georgia sits in the middle of that national range: not as brutal as the coasts, but far from fast. Nationally, coastal markets require decades of saving, and even in Missouri, the most forgiving state in a related minimum-wage calculation, a minimum-wage earner still needs 17 years to reach a 20% down payment.

Here is the part that gets lost in headlines like these: the entire 7.9-year, 65-year, and 3.9-year framework assumes you're saving toward 20% down and nothing else. That assumption is the actual myth, and it's one that has been repeated so often that most first-time buyers never question it. Lenders don't require 20% down. They never have, outside of a handful of niche loan products. The 20% figure is a rule of thumb for avoiding mortgage insurance, not a minimum to qualify, and treating it as a minimum is what turns an achievable timeline into a demoralizing one. For more on how the 20% figure became the default assumption for an entire generation of buyers, see our breakdown of the down payment myth.

So what does this mean for you: if you're budgeting your homeownership timeline around a 20% down payment, you're measuring yourself against a goal almost no first-time buyer actually needs to hit, and the years you're counting are years you may not need to wait.

The 3% down path cuts years to about two

Run the same $300,000 home through a conventional 3% down loan instead. The down payment drops to $9,000. Add typical closing costs of around 3%, roughly $9,000 more, and total cash to close comes to about $18,000. Saving the same $7,800 a year gets you there in about 2.3 years, not 7.7. Mortgage insurance applies on this path, and it will add somewhere between $100 and $250 a month depending on credit score, but it's not permanent. Under the federal Homeowners Protection Act, PMI on a conventional loan cancels automatically once you reach 78% loan-to-value, and you can request cancellation at 80%. It disappears with equity, not with another decade of saving. FHA loans start even lower, at 3.5% down, though FHA mortgage insurance behaves differently and can last the life of the loan if your down payment is under 10%.

Closing costs themselves are worth understanding before you assume you need a bigger cushion than you actually do. Our full breakdown of closing costs explained covers exactly which fees are negotiable, which are fixed, and where sellers commonly cover part of the bill for you, especially in a market where price cuts and concessions are already common. For a buyer at $78,000 income, that alone can shave months off the 2.3-year estimate.

So what does this mean for you: the real choice isn't between waiting 7.9 years or buying with no down payment cushion at all. It is between an eight-year plan built on an assumption you don't need to follow and a roughly two-year plan built on the loan products lenders actually offer first-time buyers every day.

Stacking assistance brings the timeline under a year

Georgia Dream, the state's down payment assistance program run through the Department of Community Affairs, is designed specifically to pair with a first mortgage like the 3% down loan above. The standard award is 5% of the purchase price or $10,000, whichever is less, structured as a deferred second loan with no monthly payment, repaid when you sell, refinance, or pay off the home. On a $300,000 purchase, 5% would be $15,000, so the program caps out at $10,000. Eligible teachers, nurses, veterans, active-duty military, and first responders can access the same $10,000 through the PEN track with fewer restrictions. Income limits run up to roughly $99,360 for a one to two person household in metro Atlanta counties, well above a $78,000 income, and the minimum credit score is 640.

Put the $10,000 Georgia Dream award against the $18,000 in down payment and closing costs from the 3% path, and $8,000 is left to save. At the same $7,800-a-year pace used throughout this article, that is about 12 to 13 months. Some buyers get there faster by adding gift funds from family, which federal guidelines allow for the full down payment on FHA, VA, USDA, and conventional loans with no required seasoning period beyond a documented paper trail; our guide to gift funds for a down payment walks through exactly what lenders need to see. Others layer in additional local or employer-based programs; a fuller rundown of what is available nationally is in our down payment assistance explainer.

So what does this mean for you: the "normal" savings path and the assisted path aren't two versions of the same timeline separated by a little effort. They are separated by roughly seven years, and the second path is available to almost anyone earning under the Georgia Dream income limits with a 640 credit score.

What the math actually points toward

None of this means saving is pointless or that assistance programs are a shortcut with no tradeoffs. A deferred second loan still has to be repaid eventually, and a smaller down payment means a larger loan balance and a bigger monthly payment. But the math points toward a clear conclusion: if you're putting off a purchase because you believe you need 20% down and years you don't currently have, you're solving the wrong problem. The real homework is qualifying for a 3% down loan, checking your eligibility against Georgia Dream's income and credit thresholds, and figuring out your actual closing-cost number with a specific lender and a specific home price, not the generic $60,000 figure that made the 7.9-year study go viral in the first place.

Most people who run these numbers end up realizing the gap between "I can't afford this for years" and "I can afford this within a year" is a paperwork problem, not a savings problem. If a 20% down payment has been the reason you haven't started the process, that is the assumption worth revisiting first, before anything else.