You've run the math a dozen times. At 6.43%, a $450,000 house needs roughly $90,000 down before the monthly payment stops eating a third of your paycheck. So you keep renting, keep saving $400 a month, and keep watching the number you need move further away every time prices tick up. That gap, not the mortgage rate everyone talks about, is what's actually keeping you out. And there's real money sitting in more than 2,000 programs nationwide built specifically to close it.

Down payment assistance is not a rumor and it's not a scam pitch from a late-night infomercial. It's a mix of state housing finance agency loans, regional Federal Home Loan Bank grants, and city or county programs, and most first-time buyers never apply because they assume they won't qualify or that the paperwork isn't worth it. Neither assumption holds up once you look at the actual numbers.

What down payment assistance actually is

Down payment assistance (DPA) comes in three basic forms, and the difference between them determines whether you'll ever write a check to repay it. Grants are cash that never gets repaid, full stop. Deferred second mortgages charge 0% interest and sit silently behind your first mortgage until you sell, refinance, or pay off the loan. Amortizing second mortgages get repaid every month alongside your primary payment, usually at a rate close to your first mortgage. A fourth type, forgivable loans, cancels a portion of the balance for each year you stay in the home, often reaching zero after five to ten years.

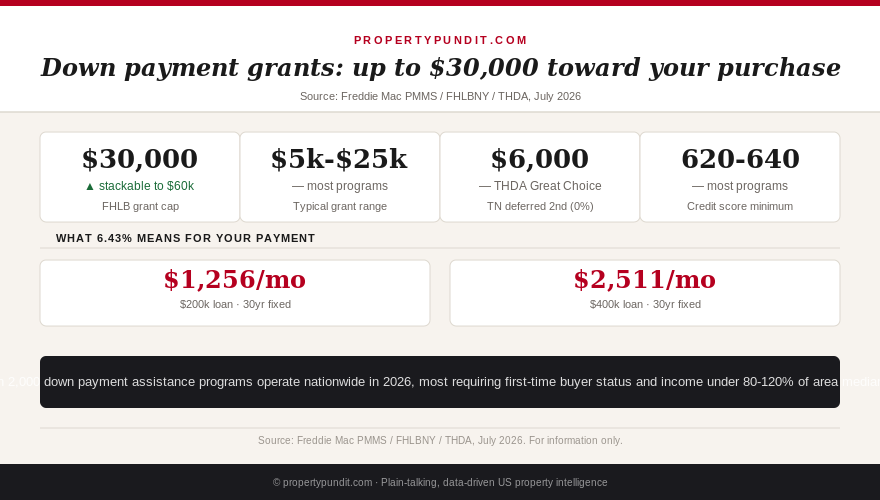

Tennessee's THDA program shows the range in one place: buyers can take a $6,000 deferred second mortgage at 0% interest with no monthly payment, or an amortizing option worth up to 5% of the purchase price, capped at $15,000, priced at the same rate as the first mortgage. THDA also raised its Nashville-area acquisition cost limit from $400,000 to $500,000 this year, which matters if you've been told you're "too expensive" for assistance programs based on outdated caps.

The type of assistance you're offered changes the real cost of the money. A $6,000 deferred loan at 0% is close to free until you sell. A $15,000 amortizing loan adds a second monthly payment on top of your mortgage. Before you accept an offer, ask your lender which type it is, not just how much it's worth.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

How much you can actually get

Grant sizes vary more than most buyers expect, and the ceiling is higher than the "$10,000 here and there" reputation DPA has earned. Each of the 11 regional Federal Home Loan Banks runs its own homebuyer grant program, and the Federal Home Loan Bank of New York allocated $31.67 million to its 2026 Homebuyer Dream Program rounds, offering up to $30,000 per household, stackable to $60,000 when layered with its HDP Plus tier. Amounts and availability differ by district, so a program running in Buffalo isn't automatically running in Boise, but the model, a large annual grant pool split among member lenders, repeats across most of the 11 districts.

Beyond the FHLB system, typical state and local grants run $5,000 to $25,000, deferred loans reach $50,000 in high-cost metro areas, and outliers exist: New York City's HomeFirst program offers up to $100,000 toward a down payment or closing costs for qualifying buyers. On a $450,000 purchase, a $30,000 FHLB-style grant covers the entire 3% conventional minimum with room left over for closing costs or a rate buydown, before you've touched your own savings.

The dollar amount only matters if you can actually get it before the round closes for the year. Ask your lender which grant rounds are currently open in your state, not which programs exist in theory.

Who actually qualifies

Most DPA programs share the same four gates: first-time buyer status, defined as no home ownership in the past three years, not literally never having owned; household income under 80% to 120% of area median income (AMI); a credit score of 620 to 640 or higher; and a completed homebuyer education course, usually a few hours online. The income limit trips people up the most, because AMI is set county by county, not as one national figure. A household earning $112,000 can be well under the limit in a higher-cost metro area and simultaneously over the limit in a cheaper one, so the income cutoff that ruled you out in one county may not apply in another.

Buyers who assume assistance is only for very low incomes are often the ones leaving the most money on the table, because they never check their county's actual AMI table before writing off the idea entirely. Pull your county's number from your state housing finance agency before assuming the door is closed.

The catch: timing and stacking

Most DPA funding is distributed first-come, first-served within an annual or quarterly allocation, and popular rounds close early. A program with a healthy budget in January can be fully committed by summer, which is exactly the window most buyers are shopping in. That urgency is real, not a sales tactic: once a region's allocation is spent, the next opportunity is often months away.

DPA also stacks with other sources more often than buyers realize. A down payment assistance grant, a gift from family, and your own savings can typically all sit on the same loan, provided the combined total doesn't exceed the purchase price plus closing costs and each source comes with its own paper trail. If a relative is planning to help, understanding how gift funds actually work alongside an assistance program can stretch a modest family contribution much further than either source alone.

Apply for open grant rounds now, even before you've found a house, so the assistance is already secured when you're ready to make an offer.

What this changes about the 20% down assumption

The idea that you need a large sum saved before you can buy is, on its own, one of the most persistent pieces of misinformation in housing. Conventional loans start at 3% down, FHA starts at 3.5%, and the 20% down payment myth has already cost buyers years of appreciation while they saved for a number lenders never required. Down payment assistance attacks the smaller, real number directly: the 3% to 5% minimum, plus closing costs, which typically run 2% to 5% of the purchase price on top of the down payment itself. A full breakdown of what's actually inside that figure is in our closing costs explained guide.

Credit score matters here too, since it affects both your mortgage rate and, in some cases, your DPA eligibility tier. If yours needs work before you apply, the fastest wins are in our credit score and mortgage rate breakdown.

Frankly, if you've been waiting to save the full down payment on your own before even looking at listings, the math points toward applying for assistance first and shopping second. Most people who run these numbers end up finding that the gap between renting and owning was never as wide as the sticker price suggested, once a grant or a low-interest second mortgage is doing part of the work.

How to actually apply

Start with your state's housing finance agency, since nearly every state runs at least one first-time buyer program, then ask whether your regional Federal Home Loan Bank has an open grant round. Your lender should be your third stop, not your first, since many loan officers keep a running list of city and county programs that a general search won't surface, but you'll get a straighter answer once you already know roughly what you qualify for. Bring your last two years of tax returns, two months of bank statements, and your credit score to that first conversation. The homebuyer education requirement can usually be completed online in an evening, so it shouldn't be the reason you delay applying.

The buyers who benefit most from these programs are the ones who apply before they've picked a house, not after. Funds committed to an accepted offer close faster and face less risk of the round running dry mid-transaction.