You've $9,000 saved toward a down payment on a $270,000 house in Atlanta, and your parents just offered to cover the rest. The relief lasts about ten minutes, then the questions start. Does that money get taxed? Does it have to sit in your account for two months before a lender will touch it? Can you even use it, given that a friend swore last week that "gift money doesn't count" on some loans? None of those assumptions is quite right, and getting even one of them wrong can cost you your closing date.

Here is what the rules actually say, sourced from the loan programs and the IRS, not from whatever your cousin heard from a loan officer three years ago.

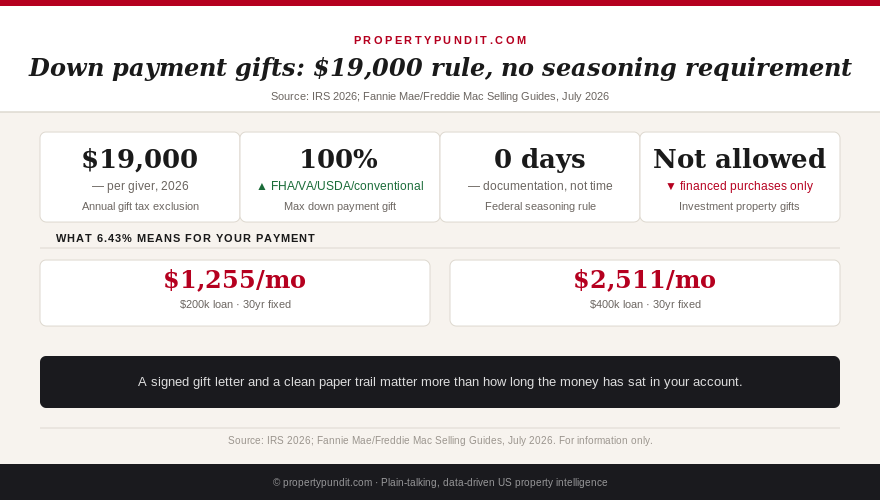

How much money can be gifted before anyone owes tax

In 2026, any individual can give any other individual up to $19,000 without filing a single form (IRS annual gift tax exclusion, 2026). Two parents giving jointly to one buyer can combine their exclusions to $38,000, tax-free, no paperwork required. If a family member wants to hand over more than that, the donor simply files an informational gift tax return (IRS Form 709); they still won't owe any actual tax unless they have already given away more than the lifetime exemption, which runs into the millions of dollars for nearly everyone. As the recipient, you never owe federal income tax on a gift, regardless of the amount.

So what this means for you: if your parents want to hand over $30,000 or $40,000 toward that Atlanta house, the tax code isn't the obstacle standing between you and the keys. The paperwork is a factor, but it is procedural, not a tax bill waiting to happen.

Which loans accept a 100% gift down payment, and which want your own money too

On a primary residence, FHA, VA, USDA, and conventional loans backed by Fannie Mae or Freddie Mac all permit gift funds to cover the entire down payment, not just part of it, provided the money comes from an eligible donor, typically a relative, and is properly documented. That is a meaningfully bigger allowance than the 3% minimum most buyers think they need to scrape together themselves. The main exception shows up on multi-unit primary residences or second homes, where some lenders require the borrower to contribute a minimum amount from their own funds rather than 100% gifted money; the exact threshold varies by lender and loan type, so it is worth asking directly rather than assuming.

On a $270,000 home at $78,000 income, that means the 3.5% FHA down payment of $9,450, or the 3% conventional minimum of $8,100, can be entirely gifted. Closing costs, typically 2% to 5% of the purchase price on top of that, can often be gifted too. So what this means for you: the cash-to-close number that feels impossible on your own salary isn't actually a savings target you've to hit alone.

The 60-day seasoning myth: what lenders actually require

Here is where most of the confusion lives. Fannie Mae, Freddie Mac, and FHA don't require gift funds to season, meaning sit untouched in your account, for 60 days or any fixed period. What they require is documentation: a signed gift letter stating the money is a gift with no expectation of repayment, plus a bank statement or wire confirmation showing the funds moved from the donor's account to yours (or directly to the title company at closing). Time in the account isn't the requirement. A clean paper trail is.

The 60-day myth likely comes from a different, unrelated rule: underwriters do scrutinize large, undocumented deposits that show up in a borrower's own account, because unexplained cash can signal an unverified loan or a compliance problem. Resolving that kind of ambiguity can genuinely take weeks. Separately, some individual retail lenders layer their own seasoning overlay on top of the investor guidelines, out of an abundance of caution, even though Fannie Mae and Freddie Mac don't ask for it. So what this means for you: if your loan officer tells you to let a gift "season" for 60 days, ask directly whether that is a Fannie Mae or FHA requirement or the lender's own overlay. The answer changes how fast you can move on an offer, and it is a fair question to ask before you assume you've to wait.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The one place gift funds don't work: a financed investment property

If you spend any time reading real estate forums while you research your own purchase, you will run into a different rule that doesn't apply to you: gift funds can't be used as the down payment on an investment property bought with a mortgage. That restriction is specific to financed rental purchases; it doesn't touch a primary residence purchase, which is the situation for the overwhelming majority of first-time buyers. Worth knowing anyway, because a lot of the confusion online comes from people quoting the investor-property rule as if it were universal. It isn't, and if you're buying a house you plan to live in, it doesn't apply to you.

How to document a gift so it doesn't blow up your closing date

The paperwork is short, but it needs to happen in the right order. First, get a signed gift letter, most lenders provide their own template, that states the donor's name, relationship to you, the dollar amount, and confirms it is a gift with no repayment expected. Second, keep proof of the donor's ability to give the money: a bank or brokerage statement showing the funds existed in their account before the transfer. Third, keep proof of the transfer itself, a wire confirmation, a copies of both sides of a cancelled check, or a deposit receipt. If the money lands in your account before closing rather than going straight to the title company, don't let it commingle with other undocumented deposits; that commingling, not the passage of time, is what actually triggers the "please explain this deposit" letters from underwriting that people mistake for a seasoning rule.

The math points toward asking early, not waiting until the week before closing, and not because of any 60-day clock. Gathering a gift letter and two sets of bank statements from a family member takes real calendar time on its own, especially if a parent is traveling or slow to respond to a document request. Most buyers who get this right start the conversation with family the same week they get pre-approved, not the week their offer is accepted. If a lender or a loan estimate has left you unsure what your full cash-to-close number actually includes, this is a good moment to walk through the full closing costs breakdown alongside your gift conversation, since both numbers move together. And if part of the reason you're leaning on a gift is to reach 20% down and avoid mortgage insurance, it is worth comparing that math against how FHA mortgage insurance actually compares to conventional PMI before you decide how large a gift you actually need. Your credit score also affects how much mortgage insurance costs, which can change how much of a gift makes sense to ask for in the first place.