You've heard the pitch a dozen times: Arizona has some of the lowest property taxes in the country, so the cash flow has to work. You've run enough of these numbers by now to know that a low tax bill is only one line in a much longer spreadsheet, and this week you decided to actually check whether Phoenix or Tucson clears the bar before you wire a deposit. They don't, and the reason isn't the tax line at all.

Arizona's statewide effective property tax rate averages roughly 0.58%, and Maricopa County, home to Phoenix, runs even lower at about 0.46%. That's genuinely one of the cheapest carrying costs in the Western US. But a full PITIA underwriting of both of Arizona's largest metros at current prices and rates shows the tax advantage isn't nearly enough to close the gap between what these homes cost and what they rent for.

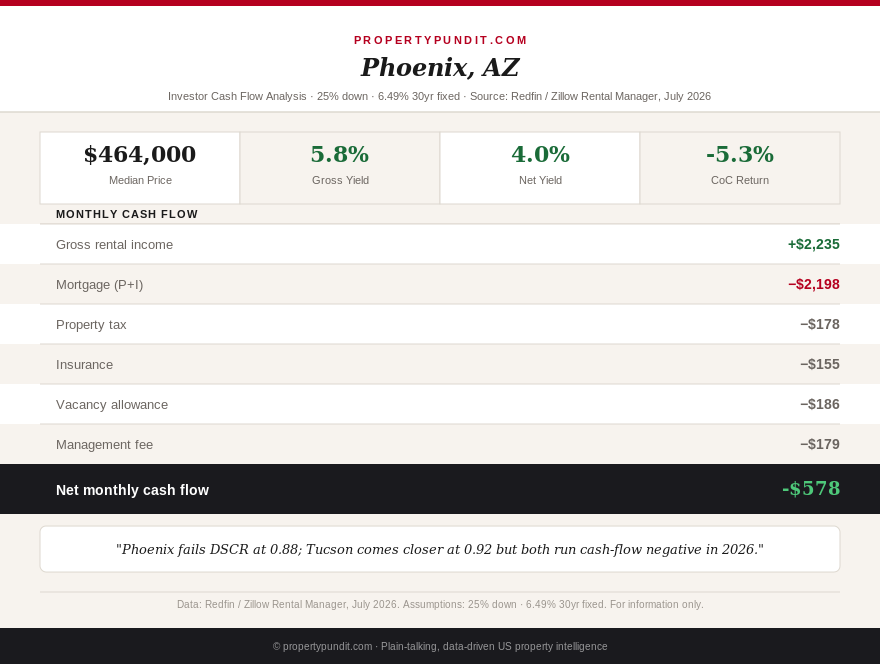

Phoenix at $464,000: the math doesn't close

Phoenix's median sale price sits at $464,000 over the three months ending May 2026, per Redfin, up 0.9% year-over-year. Zillow's broader home value index runs lower, at $411,563, reflecting the difference between actual closed sales and an estimate across the full housing stock, a gap worth knowing before you anchor on a single number. Inventory is up 15-20% year-over-year and more than a quarter of listings have taken a price cut, so this is no longer the seller's market Phoenix was known for a few years ago.

At 25% down and this week's 6.49% rate, a $464,000 Phoenix purchase carries a $348,000 loan with principal and interest of about $2,198 a month. Add Maricopa County property tax at 0.46% ($178/month) and landlord insurance around $155/month, and PITIA lands near $2,531. A typical 3-bedroom single-family rental in Phoenix brings in about $2,235 a month, per Zillow Rental Manager. That's a DSCR of 0.88, below the 1.0 minimum most DSCR lenders require, and after an 8% management fee and a 5% vacancy allowance, actual cash flow runs about negative $578 a month. So what for you: Phoenix's cheap property tax bill isn't the obstacle. The purchase price relative to achievable rent is.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Tucson at $320,000: closer, but still short

Tucson is the cheaper entry point in the state, with a median sale price near $320,000 over the same three-month window, down 1.6% year-over-year, according to Redfin. A 25% down purchase produces a $240,000 loan, with principal and interest near $1,516 a month. Pima County's property tax rate is Arizona's highest at 0.78%, adding $208 a month, and insurance runs an estimated $107 a month. PITIA totals roughly $1,831.

Tucson's median house rent is about $1,685 a month, giving a DSCR of 0.92, better than Phoenix but still short of the 1.0 minimum. After management and vacancy, cash flow comes in near negative $358 a month, the smaller loss of the two cities mainly because the entry price is lower, not because the underlying rent-to-price ratio is meaningfully stronger. So what for you: if you're set on Arizona, Tucson is the closer bet, but "closer to breakeven" and "cash-flow positive" are not the same claim, and the gap here is real money every month, not a rounding error.

The 2.5% flat tax nobody mentions in the pitch

Arizona has carried a flat 2.5% state income tax since the 2023 repeal of the Prop 208 surcharge, and it applies to rental income the same as any other earnings. It's a modest rate next to California's top bracket, but it isn't zero, and every dollar of it stacks on top of cash flow that is already negative in both Phoenix and Tucson. Compare that to a no-income-tax state like Texas or Nevada, where an investor in an equally underwater cash-flow position at least isn't handing over a slice of what little rental income does arrive. So what for you: Arizona's low property tax gets the headline, but the income tax line is the one competitor cap-rate pitches tend to leave out entirely.

The state-level picture behind both cities

Zoom out from Phoenix and Tucson and the statewide numbers tell a similar story. Arizona's median sale price sits near $448,000 as of late spring 2026, up a modest 0.8% year-over-year, per Redfin, a far cry from the double-digit appreciation years that made Arizona an investor darling earlier this decade. Inventory has grown meaningfully across Maricopa County, and that growth is exactly why so many listings are now carrying price cuts rather than multiple offers. A market that used to reward fast, aggressive DSCR-loan offers now rewards patience and a lower opening bid instead. So what for you: the Arizona of 2021, where almost any purchase worked because prices rose fast enough to bail out weak cash flow, isn't the Arizona you're underwriting in 2026.

What the low tax bill is actually good for

None of this means Arizona's tax structure is worthless to an investor, it just isn't a cash-flow fix today. A durably low property tax rate matters most over a long hold period, where it compounds as a smaller drag on net operating income year after year, and it matters more to an appreciation-focused buyer than to someone underwriting month-one cash flow on a DSCR loan. Phoenix's population and job growth remain a genuine long-run demand story; the tax rate is a tailwind for that thesis, not a substitute for it. Compare this to Anchorage, Alaska, where military housing-allowance-backed rent actually pushes DSCR above 1.0, a rarer outcome across this year's full state rotation.

The call

The math points toward treating Arizona's property tax advantage as a long-term carrying-cost benefit, not a reason to expect positive cash flow at today's prices and rates. Neither Phoenix nor Tucson clears a 1.0 DSCR at 25% down and 6.49%, and both run negative after realistic management and vacancy assumptions. Most investors who run this same underwriting on Arizona end up either lowering their offer well below list, hunting for a genuine entry-level submarket below Tucson's $320,000 median, or redirecting new capital toward a market elsewhere in our rotation that already clears the bar, like West Virginia's Martinsburg for appreciation or Anchorage for cash flow. If you're underwriting a specific Arizona property, run the full DSCR loan math yourself before you trust a cap-rate headline, and check county-level yield data on our SFR yield county map before assuming Maricopa or Pima behaves like the state average.