You've run the numbers on Memphis, on Oklahoma City, on every zero-income-tax state this newsletter has covered this year, and Anchorage never came up because it never felt like a real option. It should. At a $410,000 median, backed by a military base that pays market-rate rent through the Pentagon every month without fail, Anchorage is one of the only markets in the entire 50-state rotation this cycle where the debt service coverage ratio actually clears 1.0 on paper. The catch is that "clears the lender's minimum" and "makes you money" are two different sentences, and this week's math shows exactly where they split.

Alaska's statewide median sits at $420,506 as of May 2026, up 2.6% year over year on Redfin's tracking, while Zillow's smoother home value index puts the average closer to $395,622, up a faster 5.4%. Anchorage itself, the state's largest market by a wide margin, has a $410,000 median that is essentially flat year over year, moving in just 13 days with only 1.1 months of supply and homes closing at 99.84% of asking price. That is a tight seller's market by any national standard, even while most of the Lower 48 has swung toward buyers this year.

Why Anchorage is different from every other no-income-tax state

Every no-income-tax state covered this cycle, Texas, Tennessee, Wyoming, South Dakota, Washington, has produced the same conclusion: the tax advantage is real, but it doesn't rescue a bad price-to-rent ratio on its own. Anchorage breaks that pattern, and the reason has a name: Joint Base Elmendorf-Richardson. JBER houses tens of thousands of active-duty personnel and their families, and roughly a quarter of them, those with dependents, receive a Basic Allowance for Housing that ran 25% above the without-dependents rate in 2026, with typical enlisted rates around $2,874 to $3,045 a month before the added Cost of Living Allowance that applies specifically because Anchorage is expensive to live in. Alaska BAH rates rose about 5.4% in 2026, faster than the 4.2% national average increase. That is rent the Pentagon pays on a fixed schedule, in a market where 1.1 months of supply means a vacant unit rarely stays vacant long.

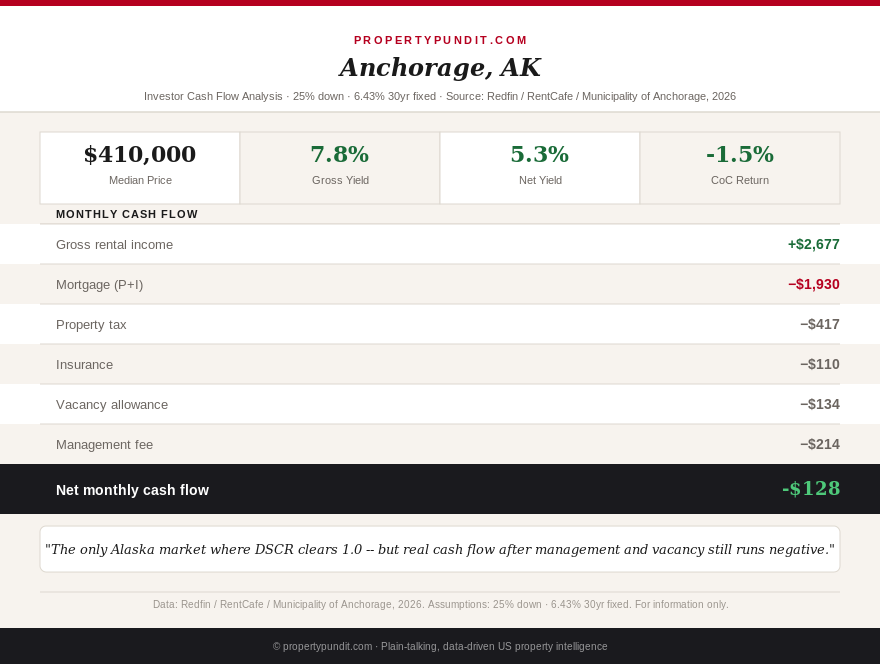

Run the numbers on a typical Anchorage single-family rental at the $410,000 median, 25% down, 6.43% rates: principal and interest is $1,930 a month, the Municipality of Anchorage's roughly 1.22% property tax adds $417, and insurance runs an estimated $110. That's a $2,457 PITI. Against a three-bedroom rent of $2,677 (RentCafe, 2026), the debt service coverage ratio comes out to 1.09, clearing the 1.0 minimum most DSCR lenders require, a bar that failed in every single state covered in the past six weeks of this rotation, from Wisconsin to Wyoming to West Virginia. If you're comparing this to the other BAH-anchored market covered this cycle, Virginia Beach's Navy-driven DSCR of 1.15 is the closest analog: a military housing allowance is doing the same heavy lifting there that JBER does here.

The DSCR pass doesn't survive contact with real expenses

A DSCR above 1.0 measures whether gross rent covers the mortgage, taxes, and insurance. It says nothing about vacancy or the cost of a property manager, and once you subtract both, the Anchorage math flips negative. Apply an 8% management fee plus a realistic vacancy allowance, roughly 13% of gross rent combined, and the effective rent drops to $2,329. Against the $2,457 PITI, that's a net cash flow of about -$128 a month. The DSCR ratio passes; the actual bank account does not. This is the same pattern this newsletter flagged in Spokane, Washington, in early July: a property can look approved on a lender's spreadsheet and still lose money every month once the true cost of property management is subtracted rather than assumed away.

The lesson for anyone underwriting an Anchorage deal from a spreadsheet in the Lower 48: DSCR is the lender's hurdle, not your hurdle. If a rental strategy depends on breaking even, model management and vacancy explicitly, or the deal that "passed DSCR" will still surprise you every month.

Fairbanks and Juneau don't even get this far

Fairbanks, home to the University of Alaska and within commuting distance of Eielson Air Force Base and Fort Wainwright, has a lower entry price at a $325,000 median, but its rental market is thinner outside student and military niches. Property tax in the Fairbanks North Star Borough runs roughly 1.3%, among the higher effective rates in the state, and estimated citywide SFR rent of around $1,800 a month produces a DSCR of just 0.90, with net cash flow after management and vacancy closer to -$446 a month. As in Morgantown, West Virginia, a citywide rent average may understate what a by-the-bedroom student rental actually earns near UAF, but that requires active, hands-on management, not passive DSCR-loan underwriting.

Juneau is the hardest of the three to underwrite cleanly. It's reachable only by air or ferry, which pushes up both construction costs and everyday maintenance and insurance expenses, and Zillow's average home value of $480,801, up 4.5% year over year, is the more reliable figure given how thin and noisy Juneau's month-to-month sale-price data can run. At an estimated $2,500 monthly SFR rent, a $480,800 purchase produces a DSCR of about 0.90 and a net cash flow near -$601 a month, the weakest of the three Alaska markets. If isolation and shipping costs sound like a niche concern, they are the entire reason Juneau's numbers don't work: the state capital has steady government employment and no shortage of demand, but every dollar of that demand runs through a supply chain that costs more to maintain than the mainland comparisons in this newsletter's county-level yield map ever have to account for.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What the $1,200 dividend does and doesn't change

Alaska pays every eligible resident an annual Permanent Fund Dividend, funded by the state's oil-wealth investment portfolio, set at $1,200 for 2026: a $1,000 base dividend plus a $200 energy relief payment. It's a real, once-a-year cash injection for tenants and a talking point in every Alaska real estate conversation, but it is not a monthly demand driver the way BAH is. One thousand two hundred dollars a year works out to $100 a month if a tenant were to spread it evenly, a fraction of the $2,457 to $2,776 in monthly housing costs modeled above. If you're underwriting Alaska rental demand, weight JBER's recurring BAH far more heavily than the dividend; one arrives every month regardless of oil prices or the state legislature's budget fights, and the other has been a subject of genuine political dispute over its size for years.

What this means if you're actually considering it

Alaska earns its place among the no-income-tax states with a genuine structural advantage: no state income tax, no statewide sales tax, and in Anchorage's case, a rental demand base that a federal paycheck effectively guarantees. But the math this week says the same thing it has said for every zero-income-tax state this newsletter has covered: the tax efficiency helps the long-run return, it doesn't turn a marginal cash-flow deal into a profitable one today. If you're underwriting a DSCR loan against Anchorage, go in expecting a modest monthly shortfall you'll cover out of pocket in exchange for appreciation and tax-free rental income, not a property that pays for itself from day one. Fairbanks and Juneau, on today's numbers, don't clear that bar even as a break-even hold, and most investors comparing all three should start, and likely stop, at Anchorage.