You have $20,000 saved. The home you want costs $270,000. Every mortgage calculator you have tried tells you the down payment should be $54,000. So you are doing the math on how many more years of renting it takes to close that gap, watching prices tick upward while your savings account earns 4.8%. That belief — that 20% is the entry ticket — is almost certainly wrong, and in a market where monthly payments have hit a one-year high of $2,647 (Redfin, June 2026), the cost of waiting on a myth is not abstract.

The 3% minimum for conventional loans has existed for years, but Fannie Mae surveys consistently show that buyers dramatically overestimate what they need to put down. The gap between the myth and reality runs to tens of thousands of dollars and, at a 20% savings rate on $78k income, three or more years of unnecessary renting.

Here is what the rules actually say in 2026, what PMI really costs and when it goes away, and the math on waiting versus buying now with 3% down.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What the minimum down payment actually is in 2026

There are five main loan types available to first-time buyers right now, and only one of them requires 20% down — and that one is entirely optional.

Fannie Mae HomeReady and Freddie Mac Home Possible: These are standard conventional loans with a 3% minimum down payment. Both programs are specifically designed for buyers at or below 80% of area median income. On a $270k purchase, that is $8,100 down. Both require completion of a homebuyer education course (free online, about four hours) and have no income limit beyond the 80% AMI cap.

Standard conventional loan: 5% minimum for most buyers not meeting the HomeReady or Home Possible income criteria. On $270k, that is $13,500 down. No income cap.

FHA loan: 3.5% minimum with a credit score of 580 or above. On $270k, that is $9,450 down. With scores between 500 and 579, FHA requires 10% down. Note that FHA's mortgage insurance premium (MIP) works differently from conventional PMI — if you put less than 10% down after June 2013, MIP stays on the loan for its entire life. That detail changes the long-term math significantly, which we address in the FHA vs. conventional comparison.

VA loan: Zero down payment, available to veterans, active-duty service members, and eligible surviving spouses. No PMI. The funding fee (typically 2.15%) can be rolled into the loan.

USDA loan: Zero down payment in eligible rural and suburban areas. Many suburban ZIP codes qualify — the USDA eligibility map covers roughly 97% of US land area. Income limits apply (generally 115% of area median income).

The 20% threshold is not a regulatory requirement. It is the point at which conventional lenders waive the PMI requirement. That is the entire origin of the myth. If you can handle PMI, the 20% floor does not exist for conventional loans.

What PMI actually costs and when it ends

PMI on a conventional loan with 3% down runs 0.6% to 1.2% of the loan amount per year, depending on credit score. On a $261,900 loan (3% down on $270k) at a credit score of 720, you are looking at roughly $131 to $157 per month at the 0.6%-0.72% range.

At a score closer to 680, that pushes toward 0.9% to 1.0%, or $196 to $218 per month. Below 660, you are at the high end: $1.0% to 1.2%, or $218 to $262 per month. Credit score matters here. If yours needs work, the move from 640 to 720 saves you approximately $65 to $105 per month in PMI alone on a loan this size.

The critical fact most buyers do not know: PMI is not permanent. Under the Homeowners Protection Act of 1998, your lender must cancel PMI automatically when your loan balance drops to 78% of the original purchase price through regular payments. You can also request cancellation at 80% LTV — no need to wait for the automatic trigger. On a $270k home purchased with 3% down, the 80% LTV mark sits at $216,000. Starting from a loan balance of $261,900, you cross that threshold through scheduled payments in roughly 7 to 8 years. If your home appreciates even modestly — say 3% per year, turning $270k into $313k within 5 years — you may be able to request cancellation much earlier via a new appraisal. The full PMI cancellation guide walks through the appraisal-based route step by step.

The PMI math changes your monthly payment, but it does not change it forever. That distinction shapes the waiting-versus-buying calculation entirely.

The actual cost of waiting to save 20%

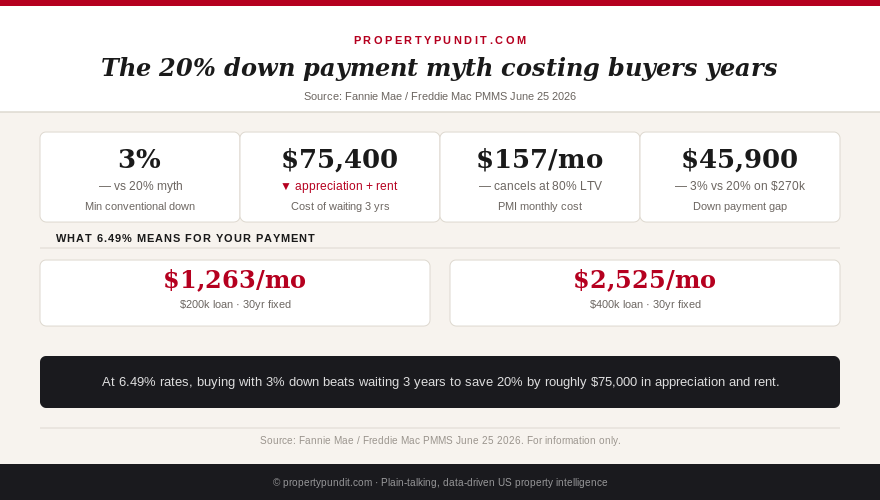

This is the math that most buyers never run. At $78k income with a 20% savings rate — a disciplined but achievable target — you are saving about $15,600 per year toward a house. On a $270k home, the gap between 3% down ($8,100) and 20% down ($54,000) is $45,900. Time to close that gap: just under 3 years.

During those 3 years, three things happen that work against you.

First, the home appreciates. At 3% annual appreciation (conservative for most markets with sub-5-month supply), a $270k home is worth $295,000 in year three. That adds roughly $25,000 to what you will need to borrow, which adds about $158 per month to your payment — more than the PMI you were trying to avoid.

Second, you keep paying rent. At a typical $1,400 per month for someone earning $78k and renting in an affordable market, 36 months of rent is $50,400 that builds zero equity.

Third, down payment assistance programs expire or change. The average DPA benefit nationally is $18,000, and many programs have first-come, first-served funding that gets depleted during peak buying seasons. Waiting three years does not guarantee those programs still exist in the same form.

Total cost of waiting to save 20%: approximately $75,400 in a realistic scenario ($25,000 in additional price appreciation plus $50,400 in rent). The cost of buying now with 3% down and carrying PMI for three years at $157 per month: roughly $5,652. The math points toward buying now with 3% down for almost every buyer in this income and savings range.

The side-by-side monthly payment comparison

On a $270,000 purchase at the current 30-year fixed rate of 6.49% (Freddie Mac PMMS, June 25 2026):

| Scenario | Down payment | Loan amount | P&I | PMI | P&I + PMI |

|---|---|---|---|---|---|

| 3% down (HomeReady) | $8,100 | $261,900 | $1,652 | $157 | $1,809 |

| 5% down (conventional) | $13,500 | $256,500 | $1,618 | $128 | $1,746 |

| 3.5% down (FHA) | $9,450 | $260,550 + 1.75% UFMIP = $265,106 | $1,673 | $121 (annual MIP forever) | $1,794 |

| 20% down (conventional) | $54,000 | $216,000 | $1,363 | $0 | $1,363 |

The gap between 3% down and 20% down is $446 per month in P&I plus PMI. That is meaningful. It is not, however, $75,400 over three years of waiting. Property taxes and homeowner's insurance apply to all scenarios equally and are excluded here for comparison purposes.

Which loan fits your situation right now

If your credit score is 720 or above and your income is at or below 80% of area median income: Fannie Mae HomeReady or Freddie Mac Home Possible at 3% down is the right tool. PMI will be at the low end of the range, and the homebuyer education requirement (free, online) adds no meaningful burden. Check whether your income qualifies at the Fannie Mae income lookup tool before assuming you do not.

If your credit score is 680-719 and you do not meet the income cap: Standard 5% conventional is likely your best route. PMI at this credit tier runs around 0.6% to 0.8% on a 5% down loan — roughly $107 to $171 per month on a $257k loan. That is manageable and it cancels.

If your credit score is below 680: FHA starts to become competitive because the rate difference between FHA and conventional at lower scores often outweighs the permanent MIP penalty. Run both scenarios side by side — or see the full FHA vs. conventional breakdown. The crossover is around 680, where conventional PMI and FHA MIP roughly equalize on a monthly basis.

If you are a veteran or active-duty service member: VA is almost always the right answer. Zero down, no PMI, and competitive rates below the conventional market. The 2.15% funding fee on a first use with full entitlement costs $5,805 on a $270k loan — but it is rolled in and you avoid years of PMI payments.

If your target home is in a suburban or rural area: Check the USDA eligibility map before ruling out a zero-down USDA loan. The income limit (115% of area median income) is generous enough that many buyers who assume they do not qualify actually do.

How to stack down payment assistance on top

Low-down-payment loans layer cleanly with down payment assistance programs. DPA does not replace the loan — it covers part or all of the down payment and sometimes closing costs through a grant or a second forgivable loan. With 2,679 DPA programs operating nationally and an average benefit of $18,000 (as covered in our DPA deep dive), the practical question is whether your income and home price qualify.

On a $270k home with 3% down required ($8,100), an $18,000 DPA grant covers the entire down payment and can absorb closing costs. Seller concessions — available on 46.2% of spring 2026 sales nationally (Redfin, June 2026) — can cover the remaining closing costs. The realistic out-of-pocket cash at closing for a buyer who properly stacks all three can be under $2,000.

The 20% myth is not just factually wrong. For buyers at sub-$100k income in markets where $270k homes exist, it functions as a years-long delay tax — a toll you pay for believing a number that does not appear anywhere in the actual mortgage underwriting guidelines. The math points toward buying now with 3% down, a PMI plan, and a clear timeline to cancellation. Most buyers who run these numbers end up wishing they had started sooner.