You've narrowed your relocation search to two cities that keep showing up on "best for first-time buyers" lists, and you're stuck picking between them with a $112,000 income and a move date creeping closer. Jacksonville and Birmingham both made Fox Business's 2026 rankings of the best US markets for first-time buyers, and the instinct is to assume Florida's zero income tax settles it. Run the actual numbers and it doesn't. Birmingham wins, and it isn't close on housing costs alone.

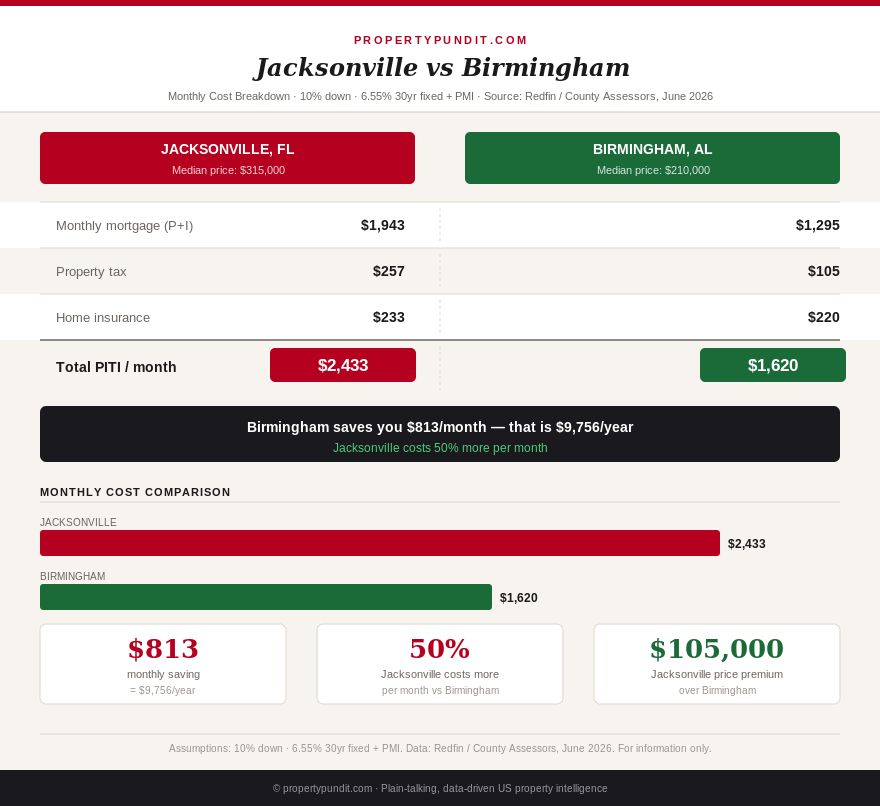

Jacksonville's median sale price sits at $315,000, up 8.6% year over year according to Redfin, while Birmingham's median is $210,000, up 15.6% over the same period, both hot markets by percentage growth but starting from very different price bases. On a 10% down, 30-year loan at 6.55%, Jacksonville's principal, interest, mortgage insurance, property tax, and homeowners insurance total roughly $2,433 a month. The identical structure in Birmingham comes to about $1,620. That's an $813 monthly gap, or $9,756 a year, before either state's income tax enters the picture.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why the price gap is bigger than the appreciation headlines suggest

Duval County's effective property tax rate runs close to 0.98%, adding about $257 a month on Jacksonville's median price. Jefferson County, home to Birmingham, comes in far lower at roughly 0.60% effective, about $105 a month on its lower base price. Add typical homeowners insurance, roughly $233 a month in Jacksonville against $220 in Birmingham, a gap driven mostly by Florida's higher storm risk, and every individual line item favors Birmingham before a single dollar of state income tax is considered. The two cities aren't close in raw housing cost, no matter how similarly their price-growth headlines read.

What Florida's zero income tax is actually worth here

Alabama taxes income at rates that work out to roughly 5% effectively at a $112,000 salary, which adds about $467 a month that a Jacksonville resident simply doesn't pay. That's real money, and it's the number every "Florida has no income tax" argument leans on. But $467 doesn't come close to closing an $813 monthly housing cost gap. Add Alabama's income tax back into Birmingham's side of the ledger and its all-in monthly cost rises to about $2,087, still $346 a month cheaper than Jacksonville's $2,433. Florida's tax advantage is real. It just isn't large enough to overcome how much more house costs in Jacksonville.

The down payment gap most buyers overlook

At 10% down, Jacksonville requires roughly $31,500 upfront against about $21,000 in Birmingham, a $10,500 difference. If you're still building savings rather than sitting on a large cushion, that gap can matter as much as the monthly payment difference, since it directly affects how soon you can actually close. A buyer targeting a specific move date should weigh the down payment timeline alongside the monthly cost, not just the sticker price of the home.

The job market difference behind the price tags

Part of why these two cities carry such different price tags is what's actually anchoring their local economies. Jacksonville's job base leans on financial services, logistics, and a large Navy presence at Naval Station Mayport and NAS Jacksonville, industries that have drawn steady in-migration and pushed housing demand up alongside them. Birmingham's economy centers on healthcare and higher education, led by UAB, one of the largest employers in Alabama, plus a legacy banking sector that has kept the local job market stable without the same population surge that's driven Jacksonville's price growth. Neither city has a weak job market. Jacksonville's has simply attracted more buyers relative to its housing supply, which shows up directly in the price gap above.

That distinction matters if you have a choice of where to work rather than a fixed job offer pulling you to one city. A buyer moving for a healthcare or education role, or simply prioritizing the lower cost of living, has a straightforward case for Birmingham. A buyer whose career depends on logistics, finance, or a Navy assignment may have no real choice between the two, in which case the $346 a month becomes a cost of the job rather than a decision at all.

What this means for your move

The math points toward Birmingham if your decision is driven primarily by monthly cost and down payment size at a $112,000 income. Most people who run these numbers side by side end up surprised that a no-income-tax state loses to one with a real income tax bill, but the lesson generalizes: a state's tax headline is one input, not the whole equation, and a large enough price gap between two cities will swallow a tax advantage every time. If job opportunities, family, or lifestyle tip meaningfully toward Jacksonville, that $346 a month may be a price worth paying. If the decision is close to a coin flip otherwise, the math says flip it toward Birmingham.

Frequently asked questions

Which city is actually cheaper to buy in, Jacksonville or Birmingham?

Birmingham is cheaper on nearly every measure. Its median home price runs roughly $105,000 lower than Jacksonville's, its property tax rate is lower, and its monthly housing cost comes in about $813 below Jacksonville's before any income tax is factored in.

Doesn't Florida's lack of income tax make Jacksonville the better deal?

No, not at this income level. Alabama's roughly 5% effective income tax on a $112,000 salary adds about $467 a month, but Birmingham's much lower housing costs still leave it ahead by about $346 a month all-in, even after that tax is added back.

Why are both of these cities getting attention for first-time buyers right now?

Jacksonville and Birmingham were both named among the best US markets for first-time buyers in 2026 by Fox Business, alongside San Antonio, Atlanta, and Houston, based on a combination of affordability, inventory, and job growth.

How much less would I need saved for a down payment in Birmingham?

At 10% down, a Birmingham purchase requires about $21,000 versus roughly $31,500 in Jacksonville, a gap of about $10,500 that can matter as much as the monthly payment difference if you're still building savings.

Both of these markets can work for a first-time buyer at $112,000 income, but only one of them stretches that income further every month. Before you commit to either city, run your own numbers through the same framework we use for down payment sizing and the full list of closing costs you'll pay on top of the mortgage, since both cities' closing cost norms differ enough to shift this comparison further. For the fuller state-level picture behind each city, see our latest Alabama market breakdown and Florida market update.