You've probably heard two Florida stories this year that seem to contradict each other: insurance rates are finally falling, and condo owners are getting hit with assessment bills large enough to wipe out a decade of rent. Both are true, and if you're weighing a Florida rental purchase right now, the property type you choose determines which story you land in. A single-family home in the right price band still has a path to positive cash flow. A condo in the wrong building can hand you a bill measured in six figures before you've collected a single month's rent. This is the difference that actually matters for your underwriting, not the statewide headline number.

What Florida's median price actually buys you

Florida's statewide single-family median sits near $425,000, with roughly 4.7 months of supply and homes taking a median of about 84 days to sell (Redfin, June 2026). Over the three months ending May 2026, the statewide median ran closer to $450,000, up 5.8% year over year (Redfin). Zillow's ZHVI, a smoothed value index across the full housing stock rather than a straight sales median, put the average Florida home value at $378,126, down 2.8% year over year. That's an unusually wide gap for a large, high-volume state, and it isn't just measurement noise: Zillow's index blends in Florida's large, currently struggling condo segment, while Redfin's sales-based median skews toward the single-family and townhome sales that are actually closing and holding up better. If a listing's "median price" claim doesn't specify property type, ask which one you're looking at before you compare it to a neighborhood you know.

The metro-level math: three cities, three failing grades

Running full PITIA underwriting at 25% down and 6.49% (Freddie Mac PMMS, July 9, 2026) across Florida's three largest non-Miami metros tells a consistent story. In Jacksonville (Duval County), a $319,000 median home (Redfin, June 2026) carries a $1,511 principal-and-interest payment, $199 in monthly property tax at Duval's 0.75% effective rate, and roughly $175 in landlord insurance, for a $1,885 PITIA. Against a $1,690 monthly rent (Zillow Rental Manager, July 2026), that's a 0.90 DSCR, a fail. Tampa (Hillsborough County) is worse: a $443,000 median home runs a $2,587 PITIA against $2,195 in rent, a 0.85 DSCR. Orlando (Orange County) lands at a $410,000 median, a $2,311 PITIA, and $1,937 in rent, an 0.84 DSCR. None of the three major metros clears the lender minimum at their current median price, which means an investor buying at the median in any of them is underwriting appreciation and insurance relief, not monthly cash flow.

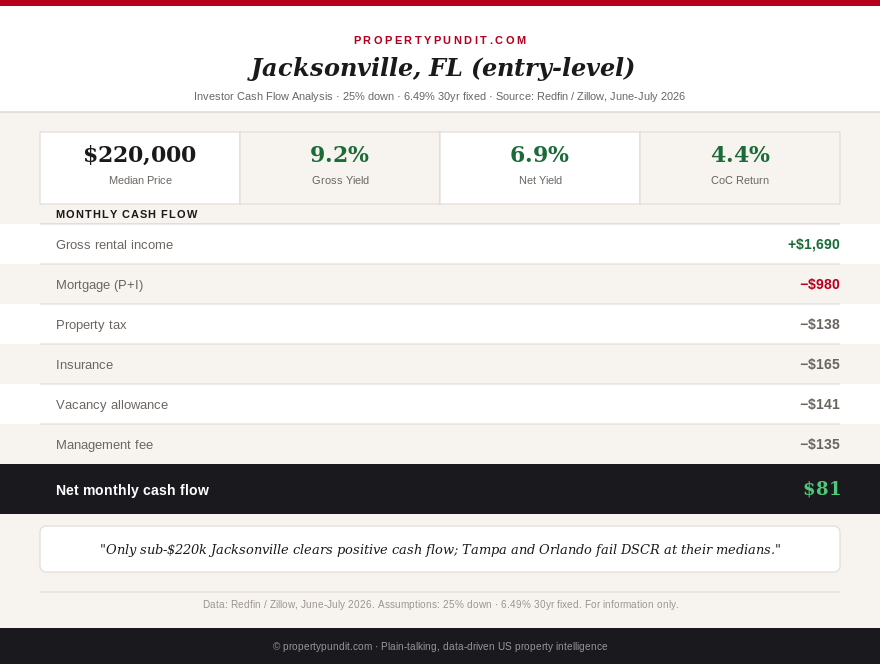

The one price point that actually works

Drop below Jacksonville's median into its entry-level stock, roughly $220,000 and under, and the math flips. At that price, with the same 25% down and 6.49% rate, PITIA runs $1,344, against the same $1,690 average rent. That's a 1.26 DSCR, comfortably above the lender minimum, and after an 8% management fee and a one-month vacancy allowance, the property still nets about $81 a month in positive cash flow. It's a thin margin, and it depends on holding insurance near $165 a month, which is realistic for an inland or moderate-risk Duval zip code but not for a coastal one. Still, it's the only positive number among four scenarios tested across Florida's largest metros. If you're underwriting Florida SFR purchases, the price band matters far more than the city name, and Jacksonville's entry-level stock is currently the state's clearest working example of that rule.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Insurance really is getting cheaper, for single-family homes

The single-family insurance story is genuinely improving, and it's worth separating from the condo story below. Florida's litigation reforms, which eliminated one-way attorney fees and cracked down on abusive assignment-of-benefits claims, have drawn 17 new insurers into the state. Citizens Property Insurance policyholders are seeing a statewide average rate reduction of 8.7% starting this spring at renewal, with more than 150,000 policyholders getting cuts of 10% or greater, and Miami-Dade and Broward homeowners specifically seeing average reductions of 13.9% and 14.1% (Florida Governor's Office, January 2026). This is the tailwind behind the Jacksonville entry-level math above; a $165-a-month insurance line would have looked closer to $220 two years ago. If you priced a Florida SFR deal off 2023 or 2024 insurance quotes and walked away, it's worth re-running the numbers with a current quote before you write the state off entirely.

The condo risk nobody's insurance discount fixes

Florida's condo market is living through a completely separate crisis, and it has nothing to do with weather risk. Since the Surfside collapse, the state has mandated Structural Integrity Reserve Studies for condo and co-op buildings three stories or higher that have reached 30 years of age, or 25 years within three miles of the coast. As of January 1, 2026, reserve waivers are banned outright for eight structural components, including roofing, load-bearing walls, plumbing, and waterproofing, and boards must now fully fund those reserves rather than deferring the cost. The result is a wave of special assessments, typically $10,000 to $100,000 per unit in older coastal buildings with real deferred maintenance, and in the most extreme documented cases as high as $134,000 per unit at a North Miami building and $175,000 per unit at a Miami Beach-area property (industry reporting, January 2026). A condo priced well below the SFR comps in the same zip code is often cheap for a reason that has nothing to do with the unit itself. Before making any offer, request the building's SIRS report and milestone inspection results directly, not just the HOA's stated monthly dues, since dues alone won't show you a special assessment that hasn't been voted on yet.

The no-income-tax math, and where it actually helps

Florida charges no state income tax, which is worth roughly $150 to $300 a month to an investor who'd otherwise be paying 4% to 5% state tax on rental income in a state like Georgia or a comparable Southeast market. That advantage is real and it compounds every year you hold the property, but it doesn't rescue a deal that's already underwater on DSCR. Compare it to Alabama, a neighboring no-income-tax-adjacent state with a lower entry price point: the tax savings matter most when they're the deciding factor on a deal that's already close to cash-flow neutral, not when they're being asked to cover a $700-a-month monthly shortfall like Tampa's or Orlando's median-price math above. Florida's tax advantage is a genuine tailwind for the right deal. It is not, on its own, a reason to buy at the metro median.

What this means for your next move

If you're underwriting Florida right now, the math points toward two specific moves rather than a single statewide verdict. First, if single-family cash flow is the goal, target Jacksonville's sub-$220,000 stock specifically, confirm your insurance quote is current (not a 2023 or 2024 number), and treat anything at or above metro median price as an appreciation bet, not a cash-flow deal. Second, if you're looking at any Florida condo priced attractively below nearby SFR comps, request the SIRS report and milestone inspection results before you make an offer; a below-market condo price with an unfunded reserve behind it isn't a discount, it's a deferred bill with your name on it once you close. Most investors who get burned in Florida right now aren't getting burned by the insurance market, they're getting burned by a condo board's balance sheet they never asked to see. Review our full DSCR loan underwriting guide and the county-level SFR yield map before you commit to either play.