You've been eyeing Idaho because it's the state everyone mentions when the coasts get too expensive, and on paper the property tax rate looks like a gift: 0.53% to 0.69%, among the lowest in the country. Run the actual investor numbers on any Idaho city at today's rates, though, and that gift evaporates. Every market examined here loses money on a rental purchased at the median price with 25% down, and the cheapest one, a college town three hours from Boise, still comes up $289 short every month.

Idaho's statewide median home price reached $490,757 in May 2026, up 2.9% year over year, with sales volume up 20% from a year earlier, according to Redfin. That statewide figure hides enormous variation, from Boise's $525,000 median down to Pocatello's $299,000. But the price spread doesn't fix the underlying problem: rents across the state simply haven't kept pace with a run of appreciation driven substantially by out-of-state buyers, the same pattern that broke the investor math in Utah's Silicon Slopes corridor last month.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Boise: the California transplant boom broke the math first

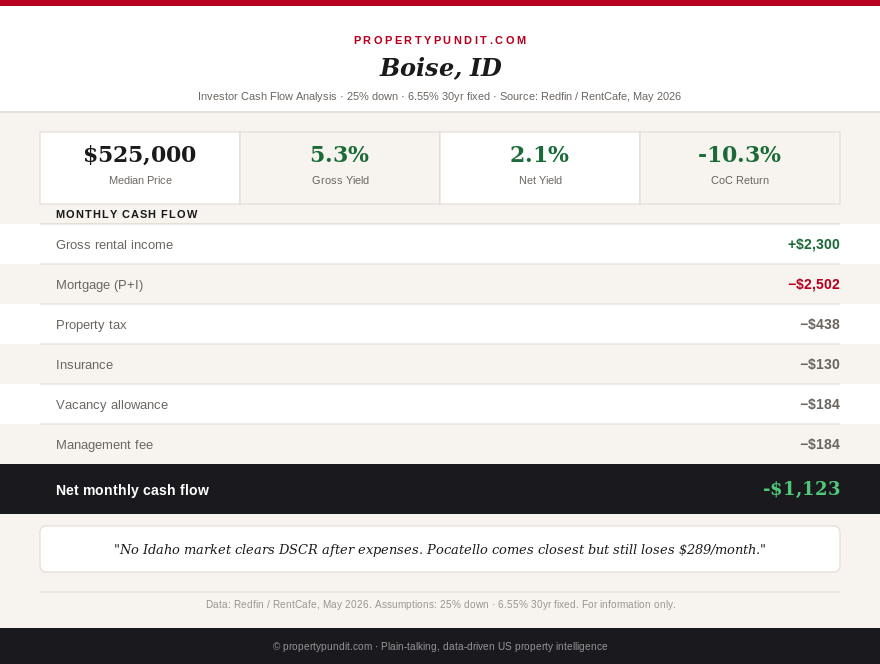

Boise's median sale price hit $525,000 over the three months ending May 2026, up 1.9% year over year, per Redfin. A 25% down purchase at 6.55% carries a $393,750 loan, a principal-and-interest payment of roughly $2,502, plus an estimated $438 in property tax and $130 in insurance, for total monthly costs near $3,069. A three-bedroom single-family rental in Boise runs about $2,300 a month. That's a DSCR of 0.75, well under the 1.0 lenders require, and a cash flow of negative $1,123 a month once an 8% management fee and 8% vacancy allowance come out of the rent. Boise's price growth has tracked a wave of buyers relocating from higher-cost, higher-tax states, pushing values up faster than local wages or rents could follow. The state's own tax marketing material leans into this exact pitch, which makes it worth remembering that a lower cost of living for a homeowner and a cash-flowing deal for an investor are two entirely different calculations.

Nampa and Idaho Falls don't escape the same trap

Nampa, in the same Treasure Valley market as Boise, posted a $420,000 median over the three months ending May 2026, up 2.8% year over year. At the same financing terms, that pencils out to a $2,466 monthly cost against roughly $1,900 in achievable rent, a DSCR of 0.77 and a cash flow of negative $858 a month. Idaho Falls, on the opposite side of the state and driven by a different economy anchored around the Idaho National Laboratory, fares only somewhat better: a $350,000 median produces a DSCR of 0.85 and a monthly loss of about $583. Neither market is close to break-even, but Idaho Falls at least demonstrates that distance from Boise's transplant-driven pricing helps, even if it isn't nearly enough on its own.

Pocatello: the closest thing to a deal, and it's still a loss

Pocatello, home to Idaho State University, is the cheapest market in this analysis at a $299,000 median, down 5.7% year over year. On paper, its DSCR of 0.99 is essentially at the lender's minimum threshold before any operating costs are subtracted, the best ratio of any Idaho city examined. But run the same 8% management and 8% vacancy allowance through the numbers and the property still loses roughly $289 a month. A market that looks like it clears the bar on a lender's back-of-envelope math still fails once you account for the costs of actually running the rental, which is exactly the trap that catches investors who stop their analysis at the DSCR ratio alone.

The tax advantage that doesn't actually apply to you

Idaho's marketed property tax rate of 0.53% to 0.69% already bakes in the state's Homeowner's Exemption, which shields 50% of a home's value, up to $125,000, from taxation, but only for an owner-occupied primary residence. Investment properties don't qualify, and pay closer to 0.95% to 1.10% effective, the rate used in every calculation above. Idaho's 5.3% flat state income tax, meanwhile, applies to rental income the same as any other earnings, with no exemption or preferential rate for landlords. Unlike Texas, Tennessee, or Florida, Idaho carries a real income tax bill and loses its headline property tax advantage the moment you stop living in the house yourself.

What this means if you're underwriting an Idaho deal

The math points toward treating Idaho as an appreciation and long-hold play right now, not a monthly income strategy. If you're set on Idaho specifically, Pocatello's college-town rental base and Idaho Falls' National Laboratory-anchored demand are the two markets closest to viable, and either could cross into positive territory with a larger down payment, a rate in the low 5% range, or a below-median entry price. Frankly, if a deal only pencils out on the strength of Idaho's advertised property tax rate, run the investor rate instead before you make an offer, because that's the number your actual tax bill will use.

Frequently asked questions

Does any Idaho market produce positive rental cash flow right now?

No. At a 6.55% mortgage rate and 25% down, Boise, Nampa, Idaho Falls, and Pocatello all fail to produce positive cash flow after management and vacancy costs. Pocatello comes closest, with a DSCR of 0.99 before operating expenses, but still runs a monthly loss of about $289 once those costs are included.

Why is Boise so expensive relative to its rents?

Boise and the surrounding Treasure Valley saw a sharp wave of appreciation driven partly by California-origin buyers relocating for a lower cost of living, pushing home prices up faster than local rents could follow, the same dynamic that drove Utah's Silicon Slopes corridor into negative cash flow territory.

Does Idaho's low property tax rate offset its weak cash flow?

Not for investors. Idaho's often-quoted 0.53% to 0.69% average effective rate already includes the state's 50% Homeowner's Exemption, which only applies to owner-occupied primary residences. Investment properties don't qualify and pay closer to 0.95% to 1.10% effective, the rate used in the calculations here.

Is Idaho at least tax-friendly for landlords in other ways?

Idaho has a flat 5.3% state income tax as of 2026, which applies to rental income like any other income. Unlike Texas, Tennessee, or Florida, Idaho offers no state income tax advantage to offset its currently negative cash flow math, making it a pure appreciation play rather than a monthly income strategy today.

Idaho joins a growing list of fast-appreciating Western states where the math has stopped working for buy-and-hold cash flow, at least at today's rates and median prices. If you're comparing markets before committing capital, our Utah investor breakdown covers the closest parallel case, our DSCR loan guide explains how lenders calculate the ratio used throughout this piece, and our county-level SFR yield map is a faster way to screen markets before you spend time underwriting a specific address. For a comparison of how a different transplant-driven state is pricing out investors at the county level, see our latest California market update.