You've been telling yourself you need 20% down before you can even start looking, which on a $78,000 salary in Atlanta feels like a number so far off it's barely worth thinking about. New data says you've had the target wrong. The median down payment nationally just fell to $23,400, the lowest level since 2021, while the home price everyone quotes at you keeps hitting records. Those two facts sound like a contradiction. They aren't, and understanding why changes what you should actually be saving toward.

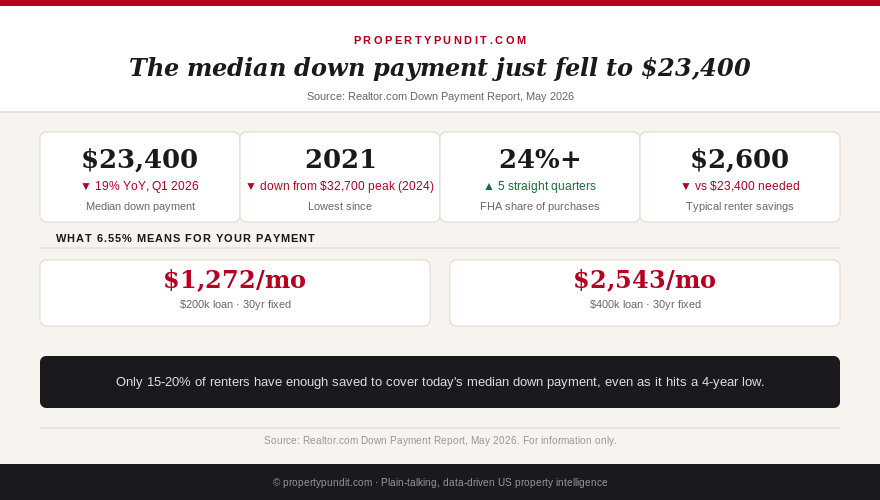

Realtor.com's Down Payment Report, released in May 2026, put the median down payment at $23,400 for the first quarter of the year, down 19% from a year earlier. That's the fourth straight quarterly decline, and it's a steep fall from the 2024 peak of $32,700. Meanwhile, the National Association of Realtors reported the median existing-home price hit a record $440,600 in June, the 36th consecutive month of year-over-year gains. Prices are up. The check buyers are writing at closing is down. Those numbers moving in opposite directions is the whole story here.

The reason is simple once you see it: down payment size and home price are set by two different groups of decisions. Sellers and the broader market set the price. Buyers, and increasingly the loan programs they use, set the down payment. As more buyers turn to FHA and VA financing, which require far less upfront cash than a conventional 20% down loan, the median check size falls even while the sticker price on the house doesn't.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why more buyers are choosing to put down less

FHA purchase loans have stayed above 24% of the market for five straight quarters, the longest stretch since 2016, and VA loans hit 11.7% of purchases in early 2026, a 10-year high, according to Realtor.com. Conforming conventional loans, the ones that typically carry the highest down payment expectations, dropped to their lowest share since 2019 over the same period. Hannah Jones, a senior economic research analyst at Realtor.com, called this a sign the market is "broadening," with buyers who might otherwise sit out turning to programs built for exactly this situation.

This isn't happening in a vacuum. Active listings have grown for 28 straight months, and roughly 40% of sellers are expected to offer concessions this year, up from 30% in 2025. A cooling, more balanced market gives buyers room to negotiate financing terms they wouldn't have gotten during the bidding wars of 2021 through 2023. If you've been assuming today's market works against you the same way it did back then, that assumption is now out of date.

The part of this that should still worry you

A smaller down payment target doesn't mean the money is easy to find. Realtor.com found the typical renter holds just $2,600 in liquid savings, a figure that only rises to $2,900 once retirement and stock accounts are included. Even at the new, lower $23,400 median, only about 15% to 20% of renters currently have enough saved to cover it. The down payment got smaller. The gap between what most renters have and what they'd need didn't close nearly as much.

That gap has a real cost attached to it beyond the frustration of waiting. Realtor.com's own research on generational wealth found that buying a home by age 30 is associated with 22.5% higher net worth by midlife, yet NAR data shows the median age of first-time buyers hit a record 40 in 2025. Every year spent trying to save a bigger down payment than you actually need is a year that compounding doesn't work in your favor.

What a smaller down payment actually looks like in dollars

Run the math on a home at the national median of $440,600. A conventional loan at 20% down requires $88,120 upfront. An FHA loan at 3.5% down requires $15,421, a difference of $72,699. Even a 10% down conventional loan, a common middle ground, runs $44,060. The $23,400 national median down payment sits closest to a blend of low FHA and VA down payments, not a 20% standard scaled down slightly. If you've been benchmarking your savings goal against 20%, you've been solving for a number the majority of today's buyers aren't actually using.

Where you live changes this math too. Down payments as a share of price run highest in the Northeast at 17.3% and lowest in the South at 11.1%, with the Midwest at 13.6% and the West at 15.2%, according to Realtor.com's regional breakdown. An Atlanta buyer sits in the cheapest region in the country to put down a smaller percentage, which is one more reason the 20% figure doesn't fit your specific situation as well as you might assume.

What this means for your own savings target

The math points toward recalculating your actual number before you decide homeownership is years away. Start with FHA's 3.5% down payment requirement, then check whether you qualify for one of the more than 2,600 down payment assistance programs now available nationwide, many of which stack directly on top of an FHA loan to cover part or all of that 3.5%. If you've been saving toward a 20% target on a $250,000 home, that's $50,000. The FHA equivalent is $8,750, a gap of $41,250 that likely represents years of your actual timeline to buy.

Frankly, if you're a first-time buyer sitting on a savings plan built around 20% down, most people who run the FHA and down payment assistance numbers end up moving their target purchase date up by a year or more once they see the real figure. The market shifted the goalpost closer. Make sure your plan reflects where it actually is now, not where it was during the last housing cycle.

Frequently asked questions

What is the actual median down payment right now?

The median down payment nationally was $23,400 in the first quarter of 2026, according to Realtor.com's Down Payment Report. That is the lowest level since 2021 and down 19% from a year earlier, the fourth consecutive quarterly drop since a 2024 peak of $32,700.

Do I really not need 20% down to buy a house?

No. 20% down isn't a requirement from any major lender or loan program. FHA loans require as little as 3.5% down, VA and USDA loans can require zero down for eligible borrowers, and conventional programs like HomeReady and Home Possible allow as little as 3%. The $23,400 median reflects that mix, not a 20% standard.

Why are down payments falling if home prices are at a record high?

Prices and down payments are set by different forces. Prices reflect what sellers can get; down payments reflect what buyers choose to put down, and more buyers are choosing smaller down payments through FHA and VA loans as the market shifts in buyers' favor, with rising inventory and seller concessions giving them more negotiating room.

What if I don't have $23,400 saved?

You're not unusual. The typical renter holds only about $2,600 in savings, meaning just 15% to 20% of renters could cover today's median down payment outright. Look into FHA, VA, USDA, and down payment assistance programs before assuming you need years to save a larger sum.

None of this erases the affordability problem this site covers every week, and it doesn't mean the math works everywhere at every price point. But if the 20% figure is the reason you've put a purchase date on hold, that reason no longer matches how most buyers are actually financing homes in 2026. Before you set your next savings goal, revisit our breakdown of the down payment myth and how PMI actually cancels once you cross 20% equity, since a smaller down payment now doesn't mean paying PMI forever. If you're weighing how long saving a bigger cushion would really take, our look at down payment savings timelines and the full rundown of closing costs you'll need on top of the down payment are the next two numbers worth getting right.