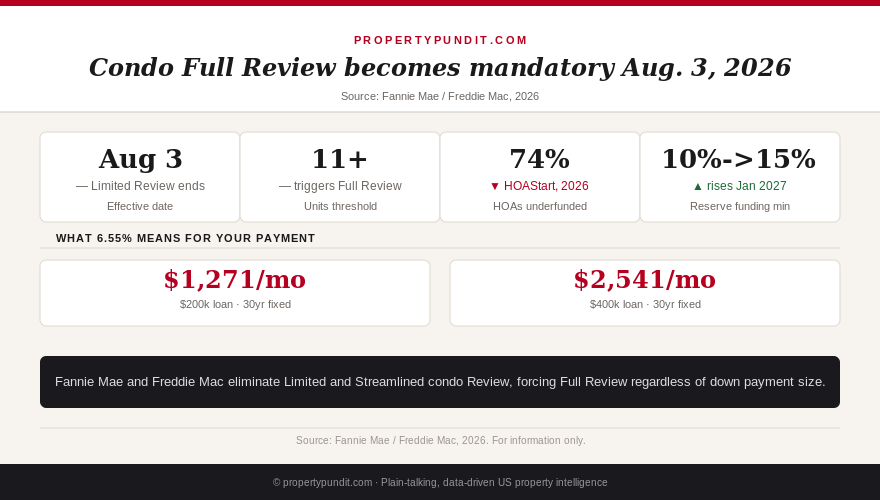

You found a condo you can actually afford on $78,000 a year, made an offer, and got it accepted. Then your loan officer mentions something called a "Full Review," and suddenly nobody can promise you the closing date is still real. Starting August 3, 2026, that scramble becomes the normal condo-buying experience for almost everyone, not a rare complication reserved for troubled buildings.

Here's what's changing. Fannie Mae is retiring its Limited Review process, and Freddie Mac is retiring its matching Streamlined Review pathway, effective August 3, 2026. Before that date, a buyer putting down 10% or more on a primary residence in a condo project could often skip a deep look at the condo association's own finances. The lender checked basic property data and confirmed insurance existed, and that was largely it. After August 3, that shortcut is gone. Every condo loan in a building with more than ten units goes through Full Review, the same rigorous underwriting the GSEs use for buildings already flagged as financially shaky.

This is the most significant change to condo mortgage underwriting since Fannie Mae and Freddie Mac tightened the rules across the board following the 2021 Champlain Towers South collapse in Surfside, Florida. That earlier round of reform targeted specific red flags: deferred maintenance, structural damage, litigation. This round removes the exemption that let well-qualified buyers avoid that scrutiny altogether. Your credit score, your income, and your down payment size no longer determine whether the underwriter opens the HOA's books. The building does.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why your excellent credit doesn't override a broke HOA

An estimated 74% of U.S. homeowners association reserve funds are underfunded relative to what their own reserve studies recommend, and about 35% expect to need a special assessment within five years, according to a 2026 HOAStart survey. Under the old Limited Review rules, a well-qualified buyer with 15% or 20% down could close on a unit in one of those underfunded buildings without the lender ever pulling the reserve study. The buyer's own strength as a borrower substituted for scrutiny of the building's health.

That substitution ends August 3. If you're putting 25% down on a condo with a 720 credit score, and the building next door has 5% down buyers, both of you now face the same documentation requirements on the association itself, because the risk the GSEs are underwriting isn't really about you. It's about whether the building can pay its own bills if the roof needs replacing in year three of your loan. Your qualifications get you approved as a borrower. They no longer get the building a pass.

What Full Review actually digs into

Full Review means the underwriter requires a current reserve study that recommends, and the association actually follows, its highest suggested funding level. Baseline or "adequate" funding levels, which some associations used to get by, are no longer accepted for this loan type. For now, the minimum share of the annual budget an association needs to allocate toward reserves stays at 10%, but that threshold rises to 15% on January 4, 2027, which is a separate deadline buyers shopping into 2027 should also flag. The underwriter also reviews the certificate of insurance, meeting minutes for signs of pending litigation or major deferred maintenance, and the association's operating budget line by line.

None of this is exotic paperwork in a well-run building. A financially healthy HOA can usually produce all of it within days. The problem is that most buyers have no idea whether their target building is well-run until a lender goes looking, and by then there's already earnest money at risk.

How much time this can add to your closing

Gathering budgets, reserve studies, and insurance documentation from an HOA board or management company routinely takes several days to a few weeks on its own, and any issue the underwriter flags adds another round of back-and-forth. An underfunded reserve account is close to impossible to fix mid-transaction. It typically requires the board to call an emergency meeting, vote to raise dues, and formally adopt a new budget, a process that can stretch a closing by weeks or months and has already caused frustrated buyers to walk away from otherwise good deals.

There's one piece of near-term relief: a transaction that's already fully underwritten before August 3, 2026 can generally still close under the existing Limited or Streamlined Review rules. But if your closing extends past that date for any reason, a financing delay, an appraisal that comes in low, last-minute seller repairs, your lender may pull you into Full Review mid-stream. That means the calendar itself is now a variable in your condo purchase, not just your own paperwork.

What to do before you sign a contract

The math points toward front-loading the diligence you'd normally leave for after an accepted offer. Before you write on any condo in a building with more than ten units, ask the listing agent or the HOA's management company for four things: the current reserve study, the most recent annual budget, the certificate of insurance, and minutes from the last two board meetings. If the building can't produce a recent reserve study at all, or the budget shows reserves well under the funding level the study recommends, that's your answer before you've spent a dime on an inspection or an appraisal.

If you're specifically trying to avoid this layer of scrutiny altogether, buildings with ten units or fewer aren't subject to the same mandatory Full Review trigger, and small, well-run associations of that size are worth asking about directly. If you're already under contract with a closing date creeping toward August 3, ask your lender today whether your file is far enough along to close under the old rules, and if not, build extra time into your financing contingency now instead of discovering the gap two weeks before your rate lock expires.

Frequently asked questions

What is Fannie Mae's condo Full Review, and why does it matter now?

Full Review is the deepest level of underwriting scrutiny Fannie Mae and Freddie Mac apply to a condo association's finances, insurance, and legal history before approving a loan in that building. Starting August 3, 2026, it becomes mandatory for nearly every condo project with 11 or more units, replacing the lighter Limited and Streamlined Review paths many buyers used to qualify quickly.

Does putting 20% or more down protect me from Full Review?

No. Before August 3, 2026, a down payment of 10% or more on a primary residence often qualified a buyer for Limited Review, skipping a deep look at the association's books. That exemption disappears. After August 3, a 20% down buyer and a 5% down buyer face identical documentation requirements on the building itself.

Can my closing still happen after August 3 under the old rules?

Transactions already fully underwritten before August 3, 2026 can generally still close under the prior Limited or Streamlined Review rules. But if your closing slips past that date, your lender can require you to restart under Full Review, which resets the documentation clock.

What condo documents should I ask for before I make an offer?

Ask for the current reserve study, the most recent annual budget, the certificate of insurance, and minutes from the last two board meetings before you write an offer. These four documents reveal most of what a Full Review underwriter will scrutinize, and they let you walk away before you have earnest money on the line.

Most buyers who run into a stalled condo closing this fall will trace it back to one of these four documents, not their own finances. If you're shopping in a building with more than ten units, treat the HOA's paperwork as due diligence you do before the offer, the same way you'd check comparable sales. It costs you a phone call. Skipping it can cost you a closing date, and possibly the earnest money that came with it. For more on protecting that earnest money once you're under contract, see our guide to closing costs, and if you're weighing a condo against a single-family purchase on a tight budget, our breakdown of the down payment myth and how PMI actually cancels covers the financing side most buyers get wrong. Investors weighing the same buildings should read how a special assessment can wreck a DSCR loan before they underwrite a deal on the old numbers.