You've heard Atlanta pitched as the Southeast's can't-miss investor market for a decade, and the state income tax headline, a flat 4.99% now, sounds like one more reason to write the offer. Before you do, run the actual numbers: at today's rates, Atlanta rental properties lose money every month, and the Georgia markets that genuinely cash flow aren't the ones getting the podcast coverage.

Georgia's statewide median sale price reached $369,687 in May 2026, up 1.3% from a year earlier, according to Redfin. That statewide figure hides a state that is splitting in two: Atlanta and Savannah prices are both falling from their pandemic-era peaks, while the state's smaller, military-anchored metros are quietly the only places where the investor math still works.

Georgia's price picture: a state median that hides a divided market

The $369,687 statewide median is a blend of two very different stories. Atlanta's metro median sits around $434,000, down 4.7% year over year, with homes now taking roughly 70 days to sell, well above the roughly 58-day statewide average. Savannah's city-level median has pulled back even harder, down about 11% year over year to roughly $330,000, a genuine correction off its pandemic peak rather than a gentle cooling.

Meanwhile, Georgia's smaller metros, Macon and Augusta among them, never ran up the way Atlanta and Savannah did, so they don't have a correction to work through. So what for you: a single statewide number tells you almost nothing useful in Georgia this year. The metro you pick matters more here than in almost any other state on our list so far.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why Atlanta doesn't pencil for investors anymore

Underwrite Atlanta's $434,000 median at 25% down and this week's 6.55% rate: a $325,500 loan runs $2,068 a month in principal and interest, plus roughly $344 in Fulton County property tax at its 0.95% effective rate and about $145 in landlord insurance, for a PITIA of $2,557. Against a realistic $1,950 monthly rent for a 3-bedroom single-family rental, that's a DSCR of just 0.76, well below the 1.0 minimum most DSCR lenders require. After an 8% management fee and a one-month vacancy allowance, net cash flow lands at roughly negative $926 a month.

The falling year-over-year price doesn't fix this. Atlanta's median is still close to its all-time high in absolute terms, and rents haven't caught up to what today's prices and rates require to break even. So what for you: treat Atlanta as an appreciation and equity-building play only, if you buy there at all, and go in knowing you're subsidizing the property out of pocket every month while you wait for that appreciation to show up.

Savannah's correction hasn't fixed the math either

Savannah looks like the more interesting story on the surface: an 11% year-over-year price drop should, in theory, get a market closer to cash-flow territory. Underwritten at $330,000, 25% down, and 6.55%, the numbers are better than Atlanta's but still negative: a $247,500 loan runs $1,573 in principal and interest, plus about $206 in Chatham County property tax and $180 in insurance (coastal Georgia carries a real premium here), for a PITIA of $1,959. Against $1,850 in rent, DSCR comes in at 0.94, close to breakeven on paper but still roughly negative $411 a month after management and vacancy.

Savannah does have a genuine long-term catalyst: Hyundai's $7.6 billion Metaplant, about 25 miles west of the city, is now in full production and the Port of Savannah remains the second-busiest container port on the East Coast by tonnage. So what for you: if you're buying Savannah today, you're betting on that employment wave to lift rents faster than prices recover, not buying a deal that already works on its own terms. That's a legitimate five-to-seven-year thesis, but know that's the bet you're making before you sign.

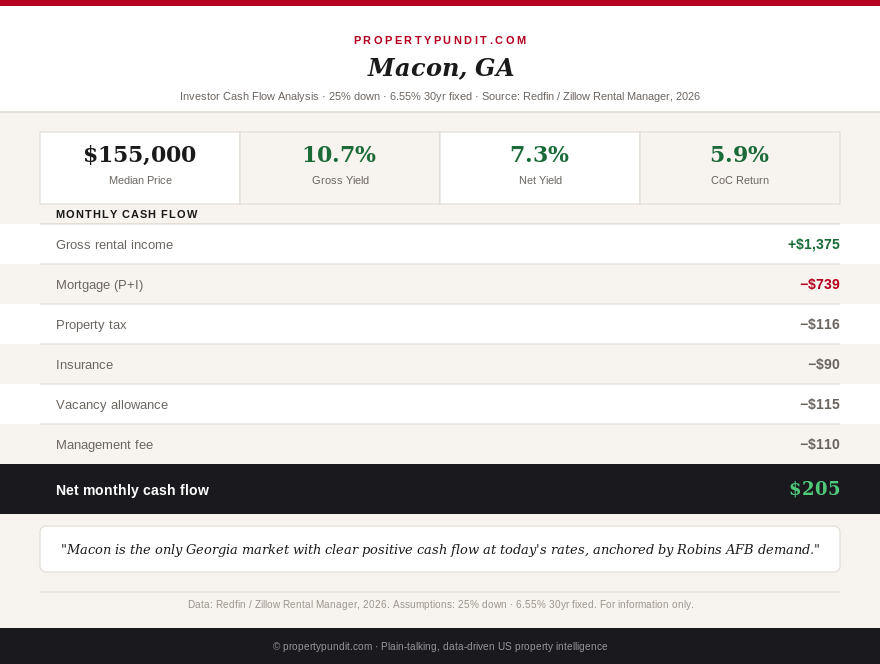

Where Georgia actually clears the bar: Macon and Augusta

Macon is the standout. At a $155,000 entry-level price, 25% down, and 6.55%, a $116,250 loan runs $739 a month in principal and interest, plus roughly $116 in Bibb County property tax and $90 in insurance, for a PITIA of $945. Against $1,375 in rent, DSCR comes in at 1.46, comfortably above the 1.0 lending threshold, and net cash flow after management and vacancy runs about positive $205 a month. Robins Air Force Base, with more than 23,000 military and civilian personnel just outside Macon in Warner Robins, anchors a stable tenant base that doesn't disappear with the next tech layoff cycle.

Augusta is close behind. A $220,000 property at the same terms puts a $165,000 loan at $1,048 a month in principal and interest, plus about $145 in Richmond County property tax at its 0.79% effective rate and $105 in insurance, for a PITIA of $1,298. Against $1,650 in rent, DSCR comes in at 1.27 and net cash flow lands around positive $83 a month. Fort Eisenhower, formerly Fort Gordon and home to the Army Cyber Command, brings more than 30,000 personnel and a similarly durable renter base. So what for you: the metro everyone searches for isn't the one that clears the underwriting bar in Georgia right now. The unglamorous, military-anchored markets are, a pattern that also showed up when we ran the same county-level analysis on Alabama and, on the coast, on Florida's condo-heavy investor math.

Georgia's tax picture: a real but modest edge

Georgia taxes all property, rentals included, at 40% of fair market value, and investment properties don't qualify for the homestead exemption owner-occupants get, so a rental's tax bill runs higher than the advertised county rate implies. Effective rates land around 0.95% in Fulton County, 0.75% to 0.80% in Chatham County, 0.90% in Bibb County, and 0.79% in Richmond County, all well inside the range covered in our county-by-county SFR yield map. The state also carries a 4% state sales tax plus local add-ons, so it isn't a no-sales-tax state the way some of its Southeastern neighbors are.

The bigger investor headline is the flat 4.99% income tax, down from 5.49% in 2024 under House Bill 463's accelerated schedule, which genuinely lowers your after-tax return on rental income compared with a graduated-rate state. So what for you: bank that savings on a deal that already clears DSCR, like Macon or Augusta, where it meaningfully improves your net return. It's not remotely large enough on its own to rescue Atlanta's roughly $926 monthly shortfall, so don't let a favorable tax headline talk you into an underwater property.

Frankly, if you're evaluating Georgia for a buy-and-hold single-family rental in 2026, the math points toward Macon and Augusta, not Atlanta or Savannah. Both military-anchored markets clear the 1.0 DSCR minimum with room to spare, both carry meaningfully lower entry prices, and neither requires you to bet on an appreciation story to make the deal work today. Most investors who run these numbers end up passing on the metro they've heard of and buying the one they haven't.