You're staring at a rate sheet that says 6.55%, and your gut says wait, because rates have bounced around all month and surely they'll come back down before your closing date. Your loan officer just mentioned something called a float-down option: lock in today's rate but keep the right to grab a lower one if rates drop before you close. It sounds like a free win. It isn't free, and whether it's worth paying for comes down to arithmetic most buyers never actually run before they say yes.

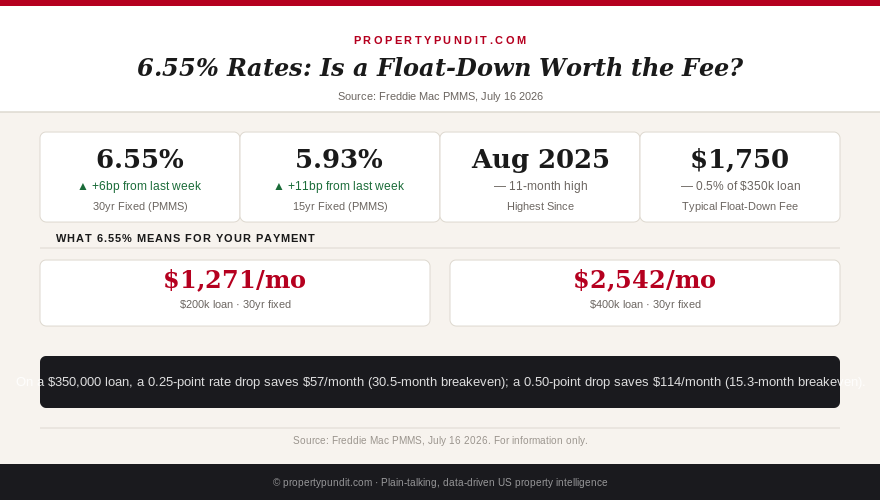

Freddie Mac's Primary Mortgage Market Survey put the 30-year fixed at 6.55% for the week ending July 16, 2026, up from 6.49% the week before and the highest reading since August 2025. The 15-year fixed rose to 5.93% from 5.82%. If you're mid-search or already under contract, that move is exactly the kind of moment a lender will pitch you a float-down. Before you pay for one, run the numbers below on your own loan size.

This week's rate move, and why it's an 11-month high

The jump from 6.49% to 6.55% wasn't driven by a jobs report or an inflation print. It followed renewed fighting between the US and Iran, which pushed oil prices back above $85 a barrel and sent Treasury yields, which mortgage rates track, higher along with them. The Mortgage Bankers Association's own weekly survey has been running even hotter, hitting 6.65% for the week ending July 10, and daily rate trackers have disagreed with each other by double-digit basis points on the same day this month. Whichever number you're watching, they all point the same direction right now: up.

So what for you: the specific trigger behind this week's spike is a war, not a slow-moving economic trend, and that distinction matters a lot for whether a float-down bet makes sense. You're not betting against a data release with a known publication date. You're betting against a conflict with no calendar at all.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What a float-down option actually buys you

A float-down lets you lock a rate today and still switch to a lower one if rates fall by a minimum threshold, usually 0.25 to 0.5 percentage points, before your loan closes. Lenders charge for that insurance: typically 0.25% to 1% of the loan amount, sometimes billed as a flat fee, sometimes folded into a slightly wider rate margin so you never see a separate line item. Most float-downs can be exercised only once, close out a few days before settlement, and aren't offered on every loan program, so ask specifically if yours applies to an FHA, VA, or USDA loan before assuming it does.

Your credit score still sets your base rate regardless of whether you add a float-down on top, and that spread is often larger than anything a float-down could recover. So what for you: get the exact trigger threshold and the exact dollar fee in writing before you agree to anything. "Up to 1%" language covers a wide range of real costs, and the number that matters is the one on your loan estimate, not the marketing copy.

The break-even math on a $350,000 loan

Here's the arithmetic in real numbers. At this week's 6.55%, principal and interest on a $350,000 loan runs $2,224 a month. If your rate fell 0.25 points to 6.30%, the payment drops to $2,166, a saving of $57 a month. A typical mid-range float-down fee of 0.5% on that loan is $1,750, which means it takes just over 30 months, more than two and a half years, to recoup the fee from a quarter-point move.

If rates fell twice as far, 0.50 points to 6.05%, the payment drops to $2,110, saving $114 a month, and that same $1,750 fee pays for itself in about 15 months. At the cheaper end of the fee range, 0.25% or $875 on this loan, a quarter-point drop alone earns the fee back in roughly the same 15 months. So what for you: both the size of the fee you're quoted and the size of the rate move you're betting on decide whether this makes sense, and neither number is fixed. Get both before you decide, not just the marketing pitch.

Why the odds don't favor a fast drop

The Federal Reserve's June 17, 2026 meeting removed its easing bias from the dot plot, and futures markets aren't pricing a rate cut until 2027. The next FOMC meeting lands July 28 to 29, and nothing in the current tone suggests a move that would pull mortgage rates down meaningfully by then. Meanwhile, the specific driver behind this week's 6.55% print, renewed Iran conflict and an $85-plus oil price, is a geopolitical shock that could ease as quickly as it appeared or could persist for months. Nobody, including us, can put a date on that.

So what for you: paying for a float-down right now is a bet that a war cools off and yields retreat inside your specific lock window, not a bet on a Fed decision you can actually see coming on a calendar. That's a materially different, and materially riskier, kind of bet than the marketing pitch usually implies.

The call

Frankly, if you're locking a rate this week with a standard 30 to 45 day window, the math argues against paying extra for a float-down: you'd need a rate drop bigger and faster than anything the current Fed calendar or this week's geopolitical driver makes likely. The math only flips with a longer 45 to 60 day lock and a specific, evidence-based reason to expect rates to ease, not just hope that they will. Most buyers who run these numbers are better off skipping the float-down fee and putting that money toward closing costs instead, or asking the seller for a temporary rate buydown, which costs you nothing and delivers a real reduction rather than a maybe. And if rates do fall substantially after you've already closed, refinancing at that point will very likely beat anything a float-down could have captured for you today.