You've built a two-property Texas and Tennessee portfolio on the no-income-tax thesis, and now you're eyeing Delaware because you've heard it's tax-friendly too. It's true, in one specific way, and it just went through a wrenching, decades-overdue correction in another. Before you run the same playbook you used in Nashville or Houston, you need to understand what actually just happened to property taxes in every one of Delaware's three counties, because the state you're underwriting today is not the state the old spreadsheets were built for.

Here's the headline number: New Castle County's average assessed home value rose 433% this year. That sounds like a tax catastrophe. It isn't, or at least not for the reason you'd assume. A 2020 Delaware Court of Chancery ruling found the state's property tax system unconstitutional, because all three counties were still calculating tax bills off assessed values frozen decades ago: New Castle County from 1983, Kent County from 1987, and Sussex County from 1974 (Court of Chancery ruling, 2020; Spotlight Delaware, 2025). Kent County issued the first new bills in 2024. New Castle and Sussex followed in 2025. This year is the first time in living memory that Delaware's property tax base actually reflects what homes are worth.

Why the rate fell as values rose

Counties are required to reset their tax rates so that reassessment doesn't hand them a windfall. New Castle County's residential rate dropped from $0.8054 to $0.1575 per $100 of assessed value specifically to keep total tax collections roughly flat year over year, not including new construction (New Castle County, fiscal year 2026 rate notice). That's not a typo: the rate fell by more than 80% in the same year assessed values jumped by more than 400%, because the assessed value and the rate are two sides of the same equation. Individual homeowners still saw their own bills move up or down depending on how their specific property's value had drifted from its 1983, 1987, or 1974 baseline relative to everyone else's, which is why some Sussex County beachfront owners in Rehoboth and Lewes reported bill increases of 400% to 532% even as the county-wide rate fell (WDEL, 2025).

If you're underwriting a Delaware purchase off a listing agent's quoted "historical" tax bill, stop. That number reflects the pre-2025 assessment in most cases and tells you almost nothing about what you'll actually owe. Pull the current post-reassessment bill for the specific parcel before you run any cash flow model, the same way an assessment-ratio state like Connecticut requires a second look before trusting a listed mill rate.

The tax-friendly reputation only tells half the story

Delaware has no state sales tax, and that single fact has given it an outsized reputation as a low-tax haven. It's not a no-income-tax state. Delaware levies a graduated state income tax that tops out at 6.6% on taxable income above $60,000 (Delaware Division of Revenue, 2026), and rental income is taxed at that same rate alongside your other earnings. If you're comparing Delaware to Texas, Tennessee, or Florida on the assumption that it belongs in the same no-income-tax bucket, that assumption is wrong and will throw off every after-tax cash flow projection you build.

What Delaware does offer, genuinely, is one of the lowest effective property tax rates in the country, roughly 0.53% to 0.57% of market value on average even after the reassessment reset (Tax Foundation, SmartAsset, 2026), well below the 1.07% national average. That's a real, durable advantage for a buy-and-hold investor, just not the specific advantage you might assume from the "no sales tax" headline.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Where the actual cash flow is

Delaware's statewide median sale price hit $398,585 in April 2026, up 2.6% year over year (Redfin, 2026), but that median is pulled sharply upward by high-priced Sussex County beach communities. The city-level picture is very different. Assuming 25% down at 6.49% (Freddie Mac PMMS, July 9, 2026), an estimated 0.55% effective property tax rate, and typical landlord insurance, here's how three Delaware markets actually underwrite using the same DSCR loan math lenders apply nationally:

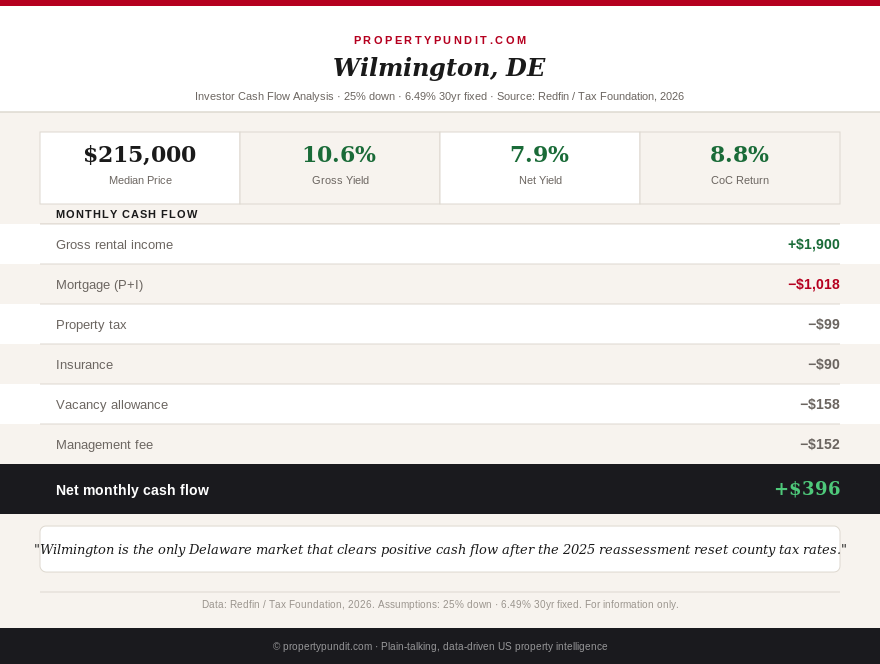

Wilmington, at a median of $215,000 (Redfin, February 2026, down 4.4% year over year), produces a loan of $161,250, monthly principal and interest of about $1,018, property tax near $99, and insurance around $90, for total PITIA of roughly $1,206. Against an estimated three-bedroom rental of $1,900 a month, that's a DSCR of 1.58 and positive cash flow of about $396 a month after an 8% management fee and a one-month vacancy allowance. Wilmington is the one market in this state where the numbers clearly work today.

Dover, at a median of $289,827 (Redfin, May 2026, down 4.7% year over year), runs a loan of $217,370, principal and interest near $1,372, tax around $133, and insurance near $95, for PITIA of about $1,600. Against an estimated rent of $1,850, DSCR comes in at 1.16, clearing the lender's 1.0 minimum, but net cash flow after management and vacancy runs slightly negative at roughly negative $40 a month. Dover passes the loan test and still loses money in practice, a gap worth checking on every deal you underwrite, not just this one.

The statewide median at $398,585 tells a worse story: a loan of $298,939, principal and interest near $1,887, tax around $183, and insurance near $110, for PITIA of roughly $2,180. Against an estimated rent of $1,950, DSCR falls to 0.89, failing outright, with cash flow after management and vacancy running about negative $535 a month. That statewide figure is not a market you'd actually buy in; it's an average skewed by beach-town price tags that don't come with beach-town rents.

If you're underwriting Delaware for cash flow rather than appreciation, Wilmington is the only market on this list worth a serious look, and Dover is close enough to justify a deeper dive on a specific below-median listing. The statewide number that shows up in most listing-site headlines should not anchor your expectations at all.

What the five-year reassessment clock means for your hold period

A 2023 Delaware law now requires every county to reassess property every five years, meaning the next reset lands around 2030 (Delaware Code Title 9, Chapter 83). That's a genuinely new planning input for anyone underwriting a multi-year hold in this state. Previously, an investor could reasonably assume decades would pass before their assessed value caught up to market reality, effectively baking in a long-running tax discount. That discount is gone. If you buy in Delaware today and the property appreciates meaningfully before 2030, expect your assessed value, and your tax bill, to move with it at the next reassessment instead of lagging for another 40 years.

The bottom line for investors

Delaware's reassessment headline number looks alarming out of context, but the mechanics behind it are a rate reset, not a tax hike, for most owners. The real work is checking the actual post-2025 bill on any specific parcel, correcting your model if you were assuming Delaware is a no-income-tax state, and picking Wilmington over the statewide average if cash flow, not appreciation, is your goal. Most investors who run these numbers end up passing on the beach-town median and looking at Wilmington's entry-level stock instead, where the math actually clears today's rates.