You've been running the numbers on a rental in Hartford for a week, and on paper it looks like the deal of the year: a home valued around $173,000 in a state where the statewide median just hit $458,372. Then you pull the actual mill rate, do the assessment math, and the property tax line alone comes to $1,404 a month, more than the mortgage payment on the same house. That's not a rounding error. That's Connecticut's entire property tax system doing exactly what it's designed to do, and it changes which town you should be looking at before you write an offer.

Connecticut's statewide median sale price reached $458,372 in May 2026, up 7.9% year over year, with some live June tracking running as high as $498,000 depending on the data source (Redfin, May-June 2026). But the state number hides enormous variation, and nowhere is that clearer than Connecticut's own property tax structure: a mill rate system, applied to 70% of fair market value, that can make a cheap-looking home in one town cost more to carry than an expensive one in the next town over.

Why Connecticut's mill rate breaks the usual investor math

Every Connecticut town sets its own mill rate, the tax charged per $1,000 of assessed value, and state law assesses property at 70% of fair market value before that rate is applied. Connecticut carries the third-highest effective property tax rate in the nation for the third consecutive year (Tax Foundation, 2026), and the town-by-town spread is dramatic: mill rates run under 12 in some of the wealthiest Fairfield County suburbs and above 60 in core cities like Hartford, Waterbury, and New Britain. Hartford's FY2025-26 mill rate sits at 74.29, among the highest of any city in the country, a direct consequence of a small taxable base carrying the cost of state government buildings, hospitals, and universities that pay no property tax at all.

That structural quirk means the usual investor shortcut, "cheaper home equals better cash flow," breaks down badly in Connecticut. Before you run a single DSCR calculation on a Connecticut property, pull the specific town's mill rate first. It matters more to your monthly payment than the purchase price itself.

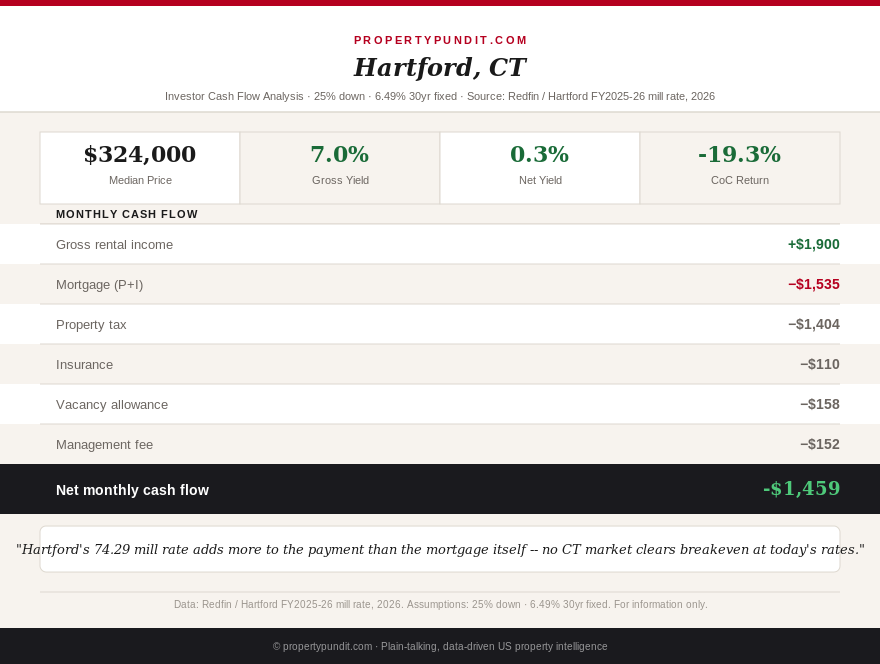

Hartford, New Haven, and Bridgeport: the DSCR math

Here's how three of Connecticut's largest markets underwrite at 25% down and 6.49% rates (Freddie Mac PMMS, July 9 2026), using an 8% property management fee plus a one-month vacancy allowance:

| Market | Price | Mill rate | PITIA | Est. rent | DSCR | Cash flow |

|---|---|---|---|---|---|---|

| Hartford | $324,000 | 74.29 | $3,049 | $1,900 | 0.62 | -$1,459/mo |

| Bridgeport | $368,133 | 53.99 | $3,038 | $2,350 | 0.77 | -$1,071/mo |

| New Haven | $387,000 | 43.88 | $2,939 | $2,450 | 0.83 | -$888/mo |

The pattern is the opposite of what you'd expect from headline home values alone. Hartford is the cheapest of the three markets by sale price and by far the worst on cash flow, purely because its mill rate is 69% higher than New Haven's. Worth noting: Hartford's own Zillow home value index runs closer to $173,276, a much lower number than the $324,000 Redfin sale median used above, because Zillow's index smooths across the full housing stock while Redfin only reflects homes that actually sold. Either way, the mill rate math applies at any price point in that town, and it's the single biggest line item working against you. That gap between the "index price" and the "transaction price" is exactly why pulling both numbers before you underwrite a Hartford deal matters more than it would almost anywhere else, in the same way it does with the county-level yield data we've mapped elsewhere.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The one real advantage: no landlord penalty rate

Unlike South Carolina, which taxes investment property at 6% of fair market value against 4% for owner-occupants, or Rhode Island's 3.5x non-owner-occupied classification covered in our Rhode Island spotlight, Connecticut applies the same mill rate to every property in a town regardless of who lives in it. That's a genuine structural advantage: your tax bill as an investor is identical to what an owner-occupant would pay on the same home. It just doesn't help much when the base mill rate in the state's biggest rental markets is already this high. A landlord-neutral tax code is worth far more in a low-mill-rate suburb than it is in Hartford, which is exactly why the town you pick matters more here than the "Connecticut has no landlord penalty" headline suggests on its own.

Exit taxes cut the other way too. Connecticut taxes capital gains as ordinary income with a top rate of 6.99% and no preferential long-term rate at the state level, unlike Washington's real-estate-exempt capital gains tax covered in our New Jersey spotlight's neighboring-state comparisons. Combined with federal long-term capital gains and the 3.8% net investment income tax, a high-income Connecticut investor can lose close to 31% of a gain at sale. That's a real number to model before you assume a Connecticut property is a straightforward buy-and-hold-then-sell play.

What this means if you're underwriting Connecticut right now

None of Hartford, New Haven, or Bridgeport clear positive cash flow under standard passive underwriting at today's rates, which puts Connecticut in the same camp as most states we've covered in this second-pass rotation: an appreciation and tax-efficiency thesis for patient, well-capitalized buyers, not a cash-flow market for a first rental purchase on a DSCR loan. If you're set on Connecticut, the math argues for shopping mill rates as hard as you shop price, since a lower-mill-rate suburb near, but not in, one of these three cities can shrink your PITIA by several hundred dollars a month on a comparable home. Frankly, if positive cash flow on day one is your bar, Connecticut isn't where you'll find it this year; if you're underwriting for a 7-to-10-year hold with a modest amount of debt and you've already priced in professional management costs, the calculus looks different, and the mill rate becomes a number to negotiate around rather than a reason to walk away entirely.