You make $112,000 a year, which sounds like real money until you start pricing homes in Denver or Salt Lake City and watch the payment blow past what any lender's rule of thumb says you should spend. You've been telling yourself one of these two cities has to be the answer, since they get compared constantly as the two big Mountain West tech-and-outdoors markets people your age actually want to live in. The honest answer is neither one currently fits your income on paper. But one of them misses by a lot less, and it isn't the one with the flashier reputation.

Denver's median sale price was $635,000 over the three months ending May 2026 (Redfin). Salt Lake City's was $584,650, up 3.5% year-over-year, over the same period (Redfin). At $112,000 income, the standard 28% housing-cost guideline caps your monthly payment at about $2,613. Neither city gets there. The gap between how badly each one misses is where this comparison gets useful.

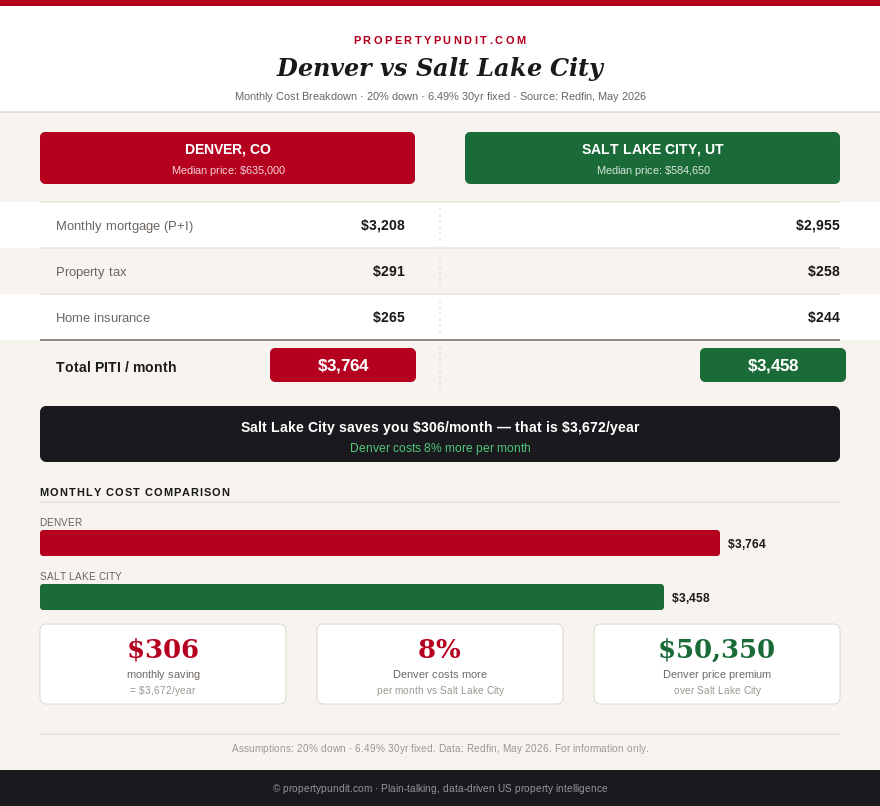

The monthly payment math

At 20% down and Freddie Mac's PMMS rate of 6.49% (July 9, 2026), Denver's $635,000 median produces a $508,000 loan, principal and interest of about $3,208/month, plus roughly $291/month in property tax and $265/month in insurance, for a total PITI near $3,764. That's $1,151 over the $2,613 ceiling at $112,000 income.

Salt Lake City's $584,650 median at the same 20% down produces a $467,720 loan, principal and interest of about $2,955/month, plus roughly $258/month in Utah property tax and $244/month in insurance, for a total PITI near $3,458. That's $845 over the same ceiling, a smaller miss than Denver's by $306 a month. Neither city currently works cleanly on paper at this income, but the size of the gap is the entire story here.

Why the tax code isn't the reason

Colorado's flat income tax is 4.4%. Utah's is 4.45%. At $112,000 income, that 0.05 percentage point difference works out to about $4.67 a month, favoring Colorado by a trivial margin. That means almost the entire $306 monthly gap between these two cities comes from the actual cost of the house and its carrying costs, not from a state tax quirk. When two states share nearly identical flat-tax rates, a comparison like this one isolates the pure housing-cost question far more cleanly than a comparison against a graduated-tax state ever could.

If you've been assuming Utah's tax structure is what makes it cheaper, it isn't. The state legislatures happen to have landed on almost the same number; the housing market did the rest.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The down payment gap

Twenty percent down on Denver's median is $127,000. Twenty percent down on Salt Lake City's median is $116,930, about $10,000 less cash needed at the closing table before you even get to the monthly closing costs both cities share. If you're not there yet on savings, that $10,000 gap is often the more immediate obstacle than the monthly payment math, and it compounds the case for Salt Lake City if your down payment fund is still growing. Either way, a smaller down payment doesn't require waiting for 20%. It changes which loan programs make sense, not whether you can move at all.

The counterintuitive part: cheaper is also appreciating faster

Salt Lake City's median rose 3.5% year-over-year as of May 2026 (Redfin). Denver's rose 2.5% over the same period. Normally a cheaper monthly payment signals a slower-growing market, a trade-off buyers are used to making. Not here. Salt Lake City is currently both the smaller monthly miss against your budget and the faster-appreciating of the two markets, which is the rare case where affordability and equity growth are pointing the same direction instead of pulling against each other. This site's Utah investor spotlight found the same underlying dynamic from the investor side: Salt Lake City's price-to-rent ratio has been stretched by Silicon Slopes tech-sector demand, the same demand now showing up as faster appreciation for anyone buying today.

The suburbs change the answer in both metros

Neither city's core median is the only option, and this is where the comparison gets more useful than a single headline number suggests. Denver's suburban ring, places like Aurora or Commerce City, prices meaningfully below the $635,000 core-metro median, and Salt Lake City's own suburbs, including West Valley City and Taylorsville, run below its $584,650 median in the same way. A buyer at $112,000 income who's willing to commute a bit further has a real shot at clearing the 28% rule in either metro's outer ring, even though neither core city clears it on its own. The comparison between Denver and Salt Lake City at the median is really a comparison between two commute-distance decisions, not just two markets.

That's a useful reframe if you've been treating this as a binary choice between two cities. The more honest question is how far outside each urban core you're willing to live in exchange for a payment that actually fits your income, and that distance-for-affordability trade tends to be a little more forgiving in the Salt Lake City metro simply because its starting median is lower to begin with.

So what this means for you

The math points toward Salt Lake City as the stronger near-term fit if you're choosing strictly between these two cities at $112,000 income, purely because the gap you have to close is smaller and the equity growth is currently running in your favor rather than against you. Neither city clears the 28% rule outright, so the real decision either way is whether you stretch past the guideline, look at a lower-priced submarket within one of these metros, or widen your search entirely. If low property taxes and no non-homestead penalty matter to you the way they do to investors, our Colorado market spotlight published today digs into that side of the Denver-area math in more detail. Most buyers who run these numbers end up either compromising on distance from the city core or extending their timeline by a year to close the gap with savings and a raise, rather than stretching to 32% or 33% of income on day one.