You've run the numbers on a dozen Colorado listings this month, and every single one comes back negative once you actually subtract the mortgage, taxes, insurance, management, and vacancy from the rent. You know Colorado has one of the lowest property tax rates in the country. You know it's supposed to be a smart investor state. The spreadsheet keeps disagreeing with the pitch, and you're starting to wonder if the state simply doesn't work for buy-and-hold cash flow at today's rates, or if you're missing a market where it actually does.

Colorado's statewide median sold price was $547,300 in April 2026, down 0.83% year-over-year (Redfin). At 25% down and Freddie Mac's PMMS rate of 6.49% (July 9, 2026), that statewide median produces a debt service coverage ratio comfortably below 1.0 almost everywhere in the state. There is exactly one market in this analysis that gets close to clearing it, and it isn't Denver.

The real tax advantage: no non-homestead penalty

Colorado's average effective property tax rate runs around 0.51%, driven by a residential assessment ratio of just 6.7% of actual value, one of the lowest in the nation. County rates in this analysis range from 0.40% in Mesa County (Grand Junction) to 0.55% in Denver County. But the more important detail for an investor is one most competitor sites never mention: Colorado classifies property by use type, not occupancy. A single-family rental is assessed at the same residential ratio as an owner-occupied home. States covered in previous spotlights on this site, including Michigan and Alabama, charge investors a materially higher non-homestead rate on the identical property. Colorado doesn't. That means the 0.51% headline rate is the real rate an investor pays here, not a teaser number that doubles once the assessor reclassifies the deed.

That genuine tax advantage is real money in an investor's pocket every single month, but as the math below shows, it isn't nearly enough by itself to offset how far Colorado's rents lag its home prices in most cities.

City by city: the DSCR math

All figures assume 25% down, Freddie Mac's PMMS rate of 6.49% (July 9, 2026), an 8% property management fee, and a one-month vacancy allowance, matching this site's standard investor underwriting across every state spotlight.

Denver: median $635,000 (Redfin, 3 months ending May 2026). Estimated SFR rent $2,700/month. PITIA (principal, interest, tax, insurance) runs approximately $3,563/month. Gross DSCR: 0.76. Net cash flow after management and vacancy: approximately -$1,286/month. Denver is Colorado's worst-performing cash-flow market in this analysis, and it isn't close.

Colorado Springs: median $450,000 (Redfin, 3 months ending May 2026). Estimated SFR rent $2,150/month. PITIA approximately $2,499/month. Gross DSCR: 0.86. Net cash flow: approximately -$685/month. Fort Carson, NORAD, and Peterson Space Force Base anchor roughly 30,000 military and defense jobs, which stabilizes rental demand even as the DSCR math still fails.

Fort Collins: median $504,339 (Norada Real Estate, 2026). Estimated SFR rent $1,865/month, a price-to-rent ratio near 23, one of the weakest in the state (Innago, 2026). PITIA approximately $2,809/month. Gross DSCR: 0.66, the worst ratio of any market covered here despite pricing below both Denver and Colorado Springs. Net cash flow: approximately -$1,235/month.

Grand Junction: median $429,000 (Redfin, 3 months ending May 2026). Estimated 3-bedroom SFR rent $2,113/month (RentCafe, 2026). PITIA approximately $2,354/month. Gross DSCR: 0.90. Net cash flow: approximately -$572/month. The Western Slope's lower property tax rate (0.40%, Mesa County) helps, but not enough to close the remaining gap.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

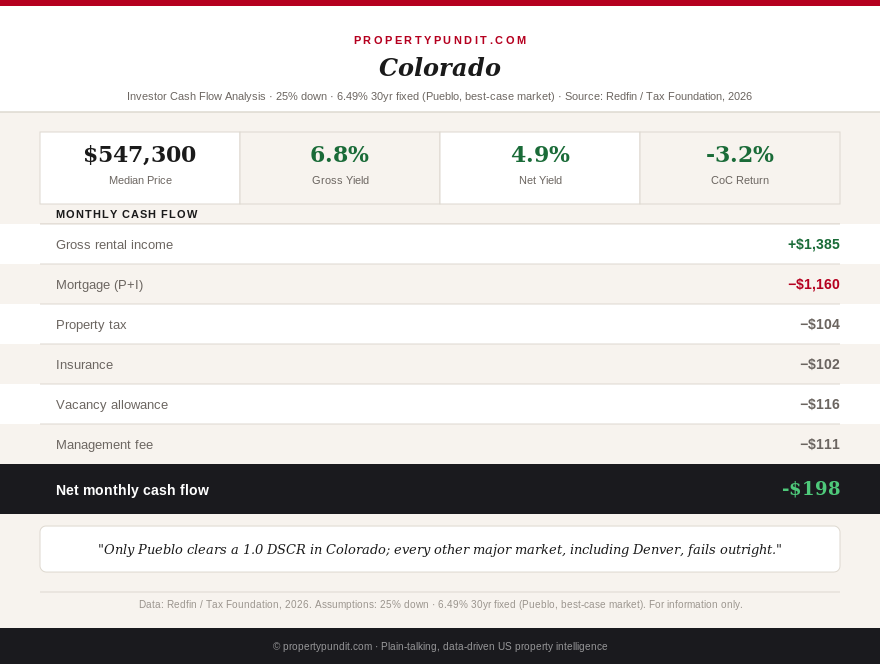

Pueblo: median $245,000 (Redfin, 3 months ending May 2026). Estimated SFR rent $1,385/month (Zillow Rental Manager, 2026). PITIA approximately $1,367/month. Gross DSCR: 1.01, the only Colorado market in this analysis that clears the 1.0 minimum most DSCR loan programs require. Net cash flow after management and vacancy: approximately -$198/month, still negative, but the smallest gap in the state by a wide margin.

Why Pueblo passes DSCR and still loses money

Pueblo's story is a pattern this site has documented in state after state this year: a property can clear the lender's DSCR threshold on gross rent alone while still running negative once real operating costs, an 8% management fee and roughly a month of vacancy per year, are subtracted. Pueblo's $245,000 entry price and comparatively strong $1,385 rent make it the closest thing Colorado has to a working SFR yield market right now, but "closest" is not the same as "positive." An investor putting down more than 25%, negotiating the purchase price, or self-managing to avoid the property management fee entirely could plausibly flip this specific deal into real positive cash flow. Nowhere else in the state offers that kind of margin for error.

The exit math: Colorado's flat tax cuts both ways

Colorado taxes ordinary income, including rental income, at a flat 4.4%. Capital gains are taxed the same way, as ordinary income at that same 4.4% rate, with no special real estate carve-out. A narrow exclusion exists for the sale of Colorado agricultural land or qualifying small-business assets held five years or longer, up to $100,000, but it doesn't apply to a standard residential rental property sale. That flat 4.4% is genuinely competitive against high-tax coastal states, but it offers no exit-tax advantage over a true no-income-tax state like Texas or Florida on a rental property sale.

If you're weighing Colorado against a no-income-tax state for a buy-and-hold rental, the property tax rate and lack of a non-homestead penalty are Colorado's real selling points, not the income tax rate, and neither one currently closes the cash-flow gap outside Pueblo.

So what this means for you

The math points toward treating Colorado as an appreciation and low-property-tax play right now, not a cash-flow play, with one narrow exception. Pueblo entry-level SFR at 25% down or more is the only market in this analysis worth underwriting for cash flow today, and even that deal needs a negotiated price, extra down payment, or self-management to move from near-breakeven into genuinely positive territory. Frankly, if you're set on buying in Denver, Colorado Springs, Fort Collins, or Grand Junction this year, you're buying for long-term equity and Colorado's real tax advantages, not for a check that clears every month. Most investors who run this exact math end up either targeting Pueblo specifically or looking one state over.