You've run the numbers on a $440,600 median-priced home more times than you'd like to admit, and it never quite works. At $78,000 a year, even a rate in the mid-6s puts the payment $700 or $800 past what a lender will approve, and the down payment feels like a decade away. Then a manufactured home listing shows up at $124,500, less than a third of the national median, and for the first time the payment actually fits. Your gut says it's a trap: something you'll be lucky to sell for what you paid, like driving a car off the lot. That instinct is wrong about the house. It's right about how a lot of buyers end up paying for one, and a law that became federal law this week just changed part of that math.

Here's what the data actually shows about appreciation, the one detail that decides whether a manufactured home is a real estate purchase or a very expensive rental, the financing mistake that costs tens of thousands of dollars, and what changed in Washington on July 11.

The depreciation you're picturing isn't happening

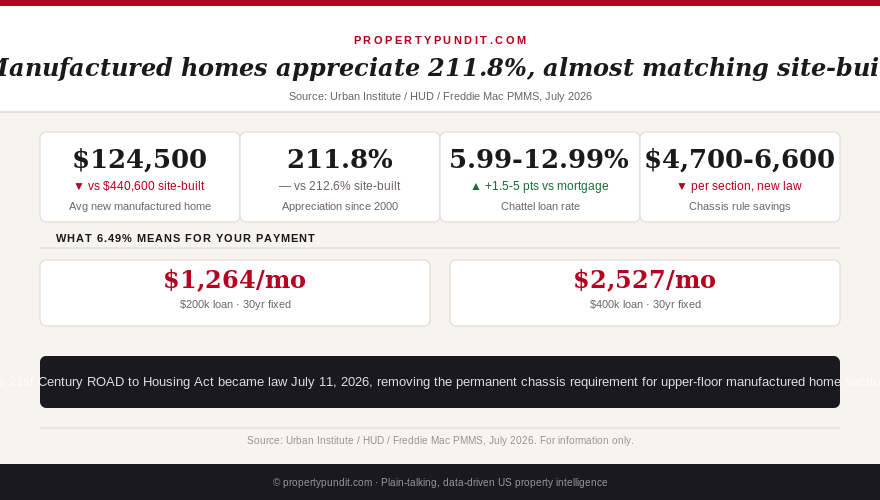

The comparison everyone reaches for is a car: drive it off the lot and it's worth less immediately. Manufactured homes don't behave that way as a category. Using repeat-sales data from Freddie Mac and the Federal Housing Finance Agency, the Urban Institute tracked purchase prices for both manufactured and site-built homes from 2000 through 2024 and found manufactured homes gained 211.8% in value over that period, against 212.6% for site-built homes, a gap of less than one percentage point over 24 years. Both worked out to roughly 5% annual appreciation. Since 2014, manufactured homes have actually out-appreciated site-built homes in nearly every quarter on a year-over-year basis.

The national average price for a new manufactured home in 2026 runs around $124,500, against NAR's $440,600 median for an existing site-built home, a discount of more than 70%. So what this means for you: the price gap between a manufactured home and a site-built one isn't a bet you're making against future resale value. On the numbers, a manufactured home tends to build equity at close to the same pace as anything else you'd buy at that price point.

The part of the myth that's actually true: who owns the ground under it

There's a real caveat buried inside that appreciation data, and it's the one thing that decides whether the statistic above applies to you. A manufactured home permanently affixed to land you own appreciates like any other home, because land, not the structure, drives most long-run value growth. A manufactured home sitting in a leased-land community, where you own the house but pay monthly lot rent to someone else, has a much weaker appreciation case, because you never capture the value of the land underneath it. It's closer to owning a very large, very durable version of the mobile home stereotype people have in their heads.

So what this means for you: before you fall for a listing price, find out whether the sale includes the land or just the structure, because that single answer decides whether you're looking at a real estate purchase or a depreciating asset with a rent bill attached.

The loan that quietly erases the deal

Assume you've found a manufactured home on owned land. The next decision, the loan type, matters more than almost anything else in the purchase. A manufactured home that isn't permanently affixed to a foundation, or that sits on leased land, typically only qualifies for a chattel loan, which finances it as personal property rather than real estate. Chattel loan rates currently run 5.99% to 12.99%, roughly 1.5 to 5 percentage points above a comparable site-built mortgage, with an average spread near 2.3 points. On a $125,000 loan, that gap adds something in the neighborhood of $200 a month, which works out to about $60,000 in extra interest over 25 years.

Once a manufactured home is permanently fixed to a foundation on land the buyer owns, it's legally reclassified as real property, and the financing options change completely. FHA Title II, VA, and USDA loans all cover permanently affixed manufactured homes, and so does conventional financing through Fannie Mae's MH Advantage and Freddie Mac's CHOICEHome programs, both built specifically to finance manufactured homes that meet certain design standards at rates close to a standard 30-year mortgage. Expect a small premium over the site-built benchmark, typically a quarter to half a percentage point, so against today's 6.49% Freddie Mac PMMS rate, a real-property manufactured-home mortgage runs closer to 6.75% to 7%. On a $112,050 loan (10% down on a $124,500 home) at 6.85%, principal and interest comes to roughly $735 a month, before property tax and insurance on whatever land the home sits on.

So what this means for you: ask a loan officer for a real-property mortgage quote before you sign anything with a manufactured-home retailer, because the type of loan, not the home itself, is what turns $124,500 into either a genuine bargain or a $60,000 mistake spread over the loan term. The math here rhymes with a mistake buyers make on the 20% down payment myth: the sticker price gets all the attention, and the financing terms quietly do the real damage.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What just changed in Washington

The 21st Century ROAD to Housing Act became law at midnight on July 11, 2026, without President Trump's signature. Congress passed it by wide bipartisan margins, 85-5 in the Senate and 358-32 in the House, and it took effect automatically after the president declined to sign it in a dispute unrelated to housing policy. The Bipartisan Policy Center and multiple outlets covering the bill describe it as the most significant federal housing supply legislation since the Cranston-Gonzalez National Affordable Housing Act of 1990. Most of the bill targets new construction red tape and, separately, restricts large institutional investors from buying new single-family homes, a provision this site covered when the House first passed it in June.

The piece that matters here: the law eliminates the requirement that the upper-floor section of a multi-section manufactured home be built on a permanent steel chassis. HUD's own analysis estimates that change saves $4,700 to $6,600 per section, since manufacturers no longer have to engineer and ship a heavy steel undercarriage for a floor that will never be transported again once the home is assembled on site. A parallel proposed HUD rule, published in the Federal Register on June 12, would extend similar changes to the broader legal definition of a manufactured home, though that rule hasn't been finalized. Together, the direction is unmistakable: multi-section manufactured homes are getting cheaper to build, not more expensive, and they're likely to look and integrate into neighborhoods more like standard site-built houses as the chassis mandate fades.

So what this means for you: if you're weighing a manufactured home against waiting another year or two to save more for a site-built purchase, the direction of travel favors buying sooner. Multi-section manufactured homes are getting cheaper and more mortgage-friendly, not the reverse, which is the opposite of the trend in the site-built market this year.

Make the call

Run through the actual decision points instead of the stereotype. Confirm the home comes on land you own or will own, because that answer alone determines whether the appreciation data above applies to your purchase. Get a real-property mortgage quote, not just a chattel loan offer from the dealer's in-house lender, and compare the monthly payment difference over the life of the loan before you sign. Factor in that the federal government just made new multi-section homes cheaper to build, which should show up in retail pricing over the next year or two.

Most buyers who run these numbers end up treating a manufactured home on owned land, financed with a real-property mortgage, as a legitimate first purchase rather than a placeholder to be embarrassed about. At a 70% discount to the national median with appreciation that tracks site-built homes almost dollar for dollar, the math points toward manufactured housing as one of the few remaining paths into ownership that doesn't require a six-figure income. Before you make an offer, it's worth reviewing what closing costs actually cover and how your credit score affects the rate you're quoted, since both apply just as much to a manufactured-home mortgage as to any other. For more on how the new housing law affects buyers generally, see our earlier coverage of the institutional investor restrictions in the same bill.