You're earning $112,000, you like the idea of Colorado, and every "moving to Denver" list you've read assumes you're either in tech at a six-figure-plus salary or you're not really considering it. Denver's median hit $635,000 over the three months ending May 2026, up 2.5% year over year, and the payment math on that number doesn't fit your income no matter how you angle it. An hour south on I-25, Colorado Springs is selling at a $450,000 median, down 3.3% over the same period. Same state, same flat income tax, same mountain views, a $185,000 gap in purchase price.

This comparison runs the full monthly cost side by side, checks both cities against the 28% housing-ratio rule at $112,000 income, and looks at why Colorado Springs has a demand floor Denver doesn't. The answer on which city actually works for a buyer at this income isn't close.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Monthly cost table: what you actually pay

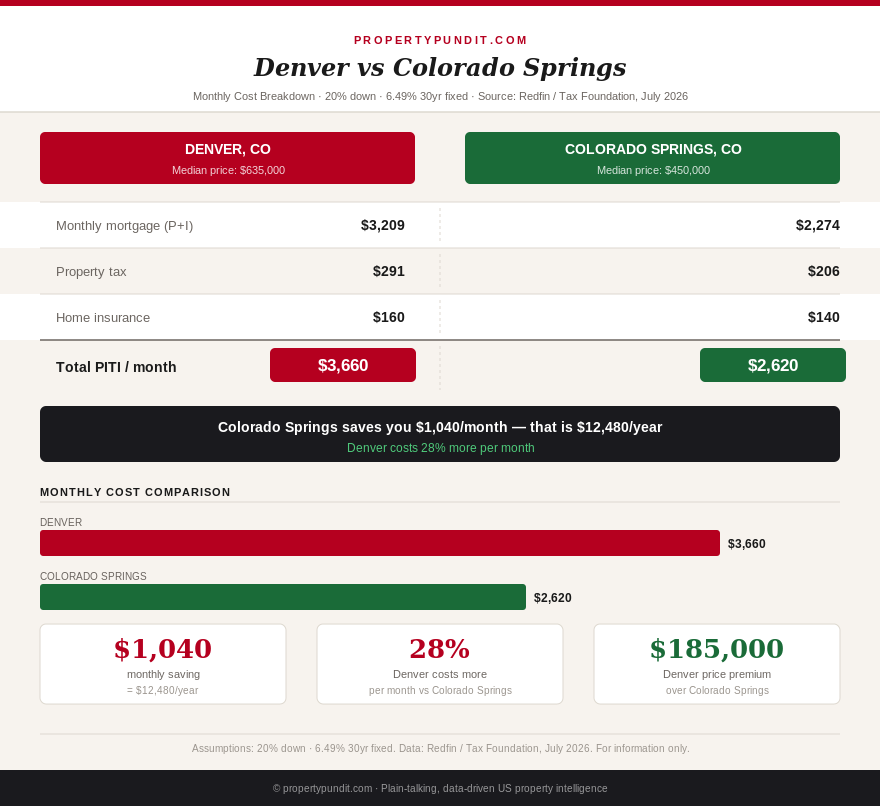

Both cities sit in Colorado, which charges a flat 4.4% state income tax on wages, so this comparison doesn't have a Nashville-versus-Memphis-style tax twist. The purchase price and the property tax dollar amount that follows from it do all the work. Colorado's residential property tax runs about 0.55% effective statewide (Tax Foundation, 2026), a genuinely low rate by national standards in both cities, so the gap below comes almost entirely from financing a $635,000 loan versus a $450,000 one.

Here's the full monthly cost comparison at 6.49%, with 20% down:

| Cost item | Denver ($635k) | Colorado Springs ($450k) |

|---|---|---|

| Down payment (20%) | $127,000 | $90,000 |

| Loan amount | $508,000 | $360,000 |

| P&I at 6.49% | $3,209/mo | $2,274/mo |

| Property tax (0.55% eff.) | $291/mo | $206/mo |

| Homeowner's insurance | $160/mo | $140/mo |

| Total PITI | $3,660/mo | $2,620/mo |

| Colorado income tax on $112k (4.4% flat) | $411/mo | $411/mo |

| Monthly gap | Colorado Springs saves $1,040/month | |

Because Colorado's income tax is a flat 4.4% rather than graduated, it adds the identical $411 a month in both cities and never changes which city wins, unlike a comparison between states with different tax structures. The entire gap here comes from the mortgage, the tax bill that follows the purchase price, and a modest difference in insurance. So what this means for you: in a same-state, same-tax-rate comparison like this one, the purchase price alone decides the outcome, which makes it one of the more mechanical calls in this format.

The 28% rule: one city clears it, one doesn't

At $112,000 income, the standard 28% housing-ratio guideline caps monthly housing cost at $2,613 ($112,000 / 12 x 0.28). Denver's PITI of $3,660 blows past that ceiling by $1,047 a month, roughly 40% over the guideline, the kind of gap that shows up as a hard decline or a much higher required down payment during underwriting. Colorado Springs' PITI of $2,620 comes in at almost exactly the ceiling, missing it by just $7 a month, close enough that a slightly better rate, a smaller insurance quote, or a few thousand dollars more down would put it under the line entirely.

So what this means for you: if you're earning $112,000 and set on Colorado, Denver isn't a stretch, it's a number that doesn't clear standard underwriting without a meaningfully larger down payment or a co-borrower. Colorado Springs is genuinely within reach, sitting right at the edge rather than well past it.

The military anchor Denver doesn't have

Colorado Springs carries a defense and military employment base that's large relative to the city's size: Fort Carson, NORAD, and Peterson Space Force Base together support an estimated 30,000-plus military and defense-connected personnel, whose housing allowance is set by federal Basic Allowance for Housing rates rather than local market conditions. That creates a demand floor for both rentals and starter homes that doesn't disappear when the broader economy softens, since a BAH-backed household's housing budget doesn't move with local layoffs the way a typical private-sector income does.

Denver's economy is more diversified, tech, aerospace, healthcare, and finance among them, and it generally pays higher salaries at the top end, but it doesn't have an equivalent floor under demand at the $112,000 income tier specifically. So what this means for you: if your $112,000 income needs a market where demand at your price point is unusually stable, Colorado Springs' military base gives it a structural advantage Denver's more cyclical, higher-paid job market doesn't replicate at this income level.

Appreciation check: the cheaper city is also the softer one

Denver appreciated 2.5% year over year through the three months ending May 2026 (Redfin), while Colorado Springs fell 3.3% over the same period. That's a real point in Denver's favor if appreciation is the priority, and it's worth naming directly rather than glossing over: Colorado Springs is currently the weaker market on price momentum, not just the cheaper one.

But run the return on the actual cash invested, not just the headline percentage. Denver's 2.5% gain on a $635,000 home is about $15,875 in first-year paper equity against a $127,000 down payment, a 12.5% return on capital invested. Colorado Springs' 3.3% decline on a $450,000 home is a paper loss of roughly $14,850 against a $90,000 down payment, a real hit if you needed to sell within the year, but a much smaller dollar amount at risk than Denver's larger loan and down payment carry in absolute terms if Denver's own momentum reverses. So what this means for you: Denver's appreciation edge is real, but it comes bundled with a monthly payment that doesn't fit a $112,000 income today, while Colorado Springs' softer market is the price of admission for a purchase that actually clears underwriting at your income right now.

Make the call

If you're earning $112,000 and choosing between these two Colorado cities, the math points toward Colorado Springs. It clears the 28% housing rule almost exactly, requires $37,000 less in down payment, and carries a military-anchored demand base that gives it more downside protection at your specific price point than Denver's cyclical, higher-income job market provides. Frankly, if you're stretching to make Denver work on this income, the $1,040-a-month gap is better spent as a bigger down payment on a Colorado Springs purchase, or saved for two more years before Denver becomes realistic. Before you make an offer in either city, it's worth reviewing the 20% down payment myth and what closing costs actually cover, since both change the real cash you need on either side of this comparison. For a look at how a similar military-anchored demand story played out in another state, see Virginia's Navy-base investor math.