Virginia sets itself apart from most states by splitting cleanly into three investor categories: a corridor where the math comes closest to working (Hampton Roads, anchored by the largest naval base in the world), a corridor that fails comprehensively (Northern Virginia, priced at federal contractor premiums), and a middle market that sits between the two (Richmond) but generates cash flow that goes the wrong direction regardless of which county you buy in. This is not a state where you can point to a hidden gem. The Hampton Roads military market is the open secret, and even there the numbers run negative after management and vacancy.

The state median sits at approximately $453,000 (Redfin, May 2026). Virginia's effective property tax rate is 0.73% statewide, ranking in the lower third nationally (Tax Foundation, 2026). The state income tax tops out at 5.75% on income above $17,000, which applies to net rental income after depreciation. At 6.43% rates (Freddie Mac PMMS, July 3, 2026), only a narrow sub-segment of the market produces DSCR ratios above 1.0 at standard 25% down.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Northern Virginia: $650k of appreciation and $1,017/month of negative cash flow

Fairfax County is the economic heart of Northern Virginia. The median SFR price runs at approximately $650,000, driven by federal contractor employment at agencies clustered around Tysons, Reston, and the Route 28 technology corridor. At 25% down, the loan is $487,500. At 6.43%, principal and interest is $3,059/month. Fairfax County's effective property tax rate is 1.135 per $100 assessed value, adding $615/month on a $650k purchase. Homeowner's insurance runs approximately $200/month on a home at this price point. Total PITIA: $3,874/month.

Average SFR rents in Fairfax run $3,000 to $3,200/month (Zillow Rental Manager, June 2026). Using $3,200, the DSCR is 3,200 divided by 3,874 = 0.83. This fails the standard 1.0 DSCR minimum by a wide margin, and fails the typical DSCR loan lender threshold of 1.0-1.25. Cash flow before management and vacancy: -$674/month. After 8% management ($256) and 7% vacancy ($224), cash flow falls to approximately -$1,017/month.

The investment thesis in Northern Virginia is capital appreciation, not rental income. The region has added federal employment steadily for 20 years, Amazon's HQ2 in Arlington continues to pull tech-adjacent jobs, and supply remains constrained by zoning across the inner suburbs. Investors who bought five years ago are sitting on 20-30% appreciation, which on a $650k purchase represents $130k to $195k in equity gains. That appreciation story is real. But at current prices and rates, you're paying $1,017/month for the privilege of holding that appreciation thesis. If you're underwriting a Northern Virginia SFR as a rental property in 2026, the math does not support it.

Richmond: high city tax wipes out the Midwest-style entry price

Richmond city carries a headline median of $414,000 (Redfin, May 2026). That price looks approachable relative to Northern Virginia. What the listing pages don't show is the city's property tax rate: $1.20 per $100 assessed value, which is the highest rate of any major Virginia locality. On a $414k purchase, property tax adds $414/month. With 25% down ($103,500), the loan is $310,500. P&I at 6.43%: $1,948/month. Insurance: $160/month. Total PITIA: $2,522/month.

Average SFR rents in Richmond city run approximately $1,800 to $2,000/month (Zillow, June 2026). At $1,900, DSCR is 1,900 divided by 2,522 = 0.75. That fails the investor minimum. Cash flow before management: -$622/month. Henrico County (suburban Richmond) offers slightly better math: at $380k with Henrico's 0.83% property tax rate ($263/month), PITIA falls to $2,206/month. At $1,900 SFR rent, DSCR is 0.86. Still fails, but the cash flow improves to -$306/month.

Richmond's appeal for long-hold investors is its trajectory. The city has added residents at a faster rate than most mid-Atlantic cities since 2018, VCU anchors a healthcare and education employment base, and the Scott's Addition and Manchester neighborhoods have drawn significant developer activity. As a pure appreciation play with a long horizon and sub-$320k entry prices in Henrico, the Richmond market has a case. As a cash-flow rental market at today's rates, it does not. The Richmond investor needs either a lower entry price (sub-$280k in Chesterfield or Henrico) or a rate drop of at least 100 basis points to push DSCR meaningfully above 1.0.

Hampton Roads: the military anchor that makes Virginia Beach almost work

Naval Station Norfolk is the largest naval base in the world. Naval Air Station Oceana sits in Virginia Beach. Fort Eustis (now Joint Base Langley-Eustis, combined with Langley Air Force Base) is in Newport News. The combined active-duty population across Hampton Roads exceeds 75,000 service members, each eligible for Basic Allowance for Housing (BAH) that scales with local rental market rates. In the Norfolk-Virginia Beach area, BAH for an E-5 with dependents runs approximately $1,900 to $2,100/month in 2026 (DoD BAH rates, 2026). That allowance creates a structural rental floor that civilian-only markets don't have.

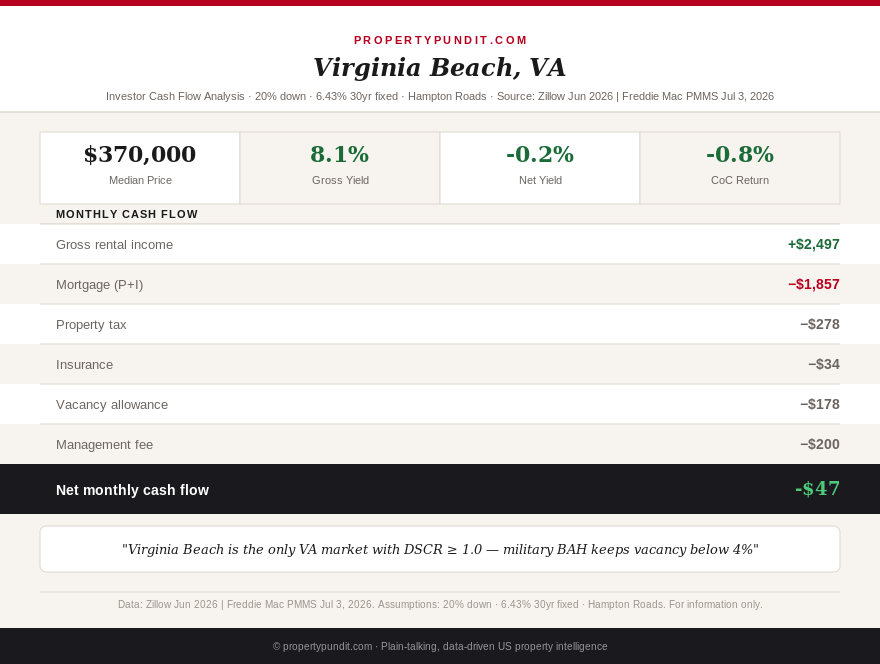

The Virginia Beach SFR market shows the direct result. Average rent for a single-family home in Virginia Beach: $2,497/month (Zillow Rental Manager, June 2026). At an investor entry price of $370,000 with 25% down ($92,500), the loan is $277,500. P&I at 6.43%: $1,741/month. Virginia Beach city property tax: $0.90 per $100 assessed value, adding $278/month. Insurance: $150/month. Total PITIA: $2,169/month.

DSCR: 2,497 divided by 2,169 = 1.15. This passes the standard DSCR investor threshold of 1.0, and qualifies for a DSCR loan product. For a full breakdown of how DSCR loans are underwritten, the key point is that a ratio above 1.0 means the gross rent covers the full PITIA payment. After 8% management ($200/month) and 7% vacancy allowance ($175/month), net effective rent is $2,122/month. Cash flow versus PITIA: -$47/month. That's essentially breakeven at the operating level, before accounting for maintenance reserves.

Norfolk city offers a lower entry point. SFR median near the base corridor runs approximately $285,000. At 25% down ($71,250), loan of $213,750, P&I at 6.43%: $1,341/month. Norfolk city property tax: $0.97 per $100 assessed value, adding $230/month. Insurance: $130/month. PITIA: $1,701/month. SFR rents near Naval Station Norfolk run approximately $1,900/month for a three-bedroom. DSCR: 1,900 divided by 1,701 = 1.12. Passes. After management and vacancy, cash flow is approximately -$86/month. Still negative, but within a reasonable maintenance reserve allowance for a property in this price range.

Chesapeake, the next city over, carries a 1.09% property tax rate: higher than Virginia Beach and Norfolk. At $350k entry, PITIA lands at $2,176/month against $1,900 SFR rents, producing DSCR of 0.87. That fails. Stick to Virginia Beach and the Norfolk base corridor if Hampton Roads is your target market.

Virginia income tax: what it actually costs on rental income

Virginia taxes rental income as ordinary income at rates up to 5.75%. The top bracket applies to income above $17,000, so for most investors, rental income is taxed at the full state rate after deducting depreciation. On a Virginia Beach SFR generating $29,964 in annual gross rent ($2,497/month), straight-line depreciation on the building portion at 27.5 years adds approximately $13,455/year in deductions (on a $370k purchase with 80% allocated to the structure). Net taxable rental income: approximately $16,509. State tax: 5.75% of $16,509 = $950/year, or $79/month. That turns the -$47/month operating cash flow into approximately -$126/month after the state income tax drag.

This is still far better than Northern Virginia's -$1,017/month or Richmond's -$622/month. The Virginia Beach investor is holding a property that qualifies for DSCR financing, operates near breakeven on a cash basis, and participates in a rental market with structural BAH-driven demand that does not evaporate in recessions the way civilian employment can. For an investor whose primary thesis is equity accumulation and moderate appreciation over a five-to-ten year hold, Hampton Roads is the only Virginia market that pencils. Virginia Beach SFR has appreciated at roughly 4.5% annually over the past five years (Redfin), and the restricted supply environment near the base corridors supports continued modest appreciation.

What the numbers say

Virginia gives investors one viable market, a highly restricted set of entry parameters within that market, and a state tax structure that is moderately unfriendly to rental income. Compare that to Tennessee (zero income tax, Memphis sub-$155k at DSCR 1.30) or Oklahoma (0.92% property tax, Tulsa sub-$185k at DSCR 1.27), and Hampton Roads looks expensive for what it delivers in current cash flow. The case for Virginia Beach and Norfolk is specifically: a property that qualifies for DSCR financing, a tenant base with federally-funded housing allowances, and 4-5% historical appreciation in a supply-constrained coastal market.

If you're comparing Virginia to adjacent states, North Carolina's Fort Liberty corridor (Fayetteville/Spring Lake) delivers slightly positive cash flow at lower entry prices with a 4.75% income tax. If you're committed to Virginia, buy within the military rental radius in Virginia Beach or Norfolk, target sub-$385k SFR, use 25% down, and model the operating cash flow as approximately -$100 to -$150/month after all costs. The return on this investment is equity, appreciation, and DSCR financing eligibility, not monthly positive cash flow. The math points toward patience on a Virginia investment rather than expecting it to carry itself from month one.