You keep hearing that Arkansas is a hidden gem for investors: rock-bottom property tax, a state government that keeps cutting income tax, and home prices that still look like 2019 numbers in the rest of the country. All of that is true. None of it means the numbers actually clear once you run a real mortgage payment against real rent. If you have $60,000 or so sitting in a self-directed IRA or a brokerage account waiting for the right DSCR loan deal, Arkansas deserves a serious look, but not the uncritical one it usually gets in national "best states for landlords" roundups.

Arkansas's headline numbers are genuinely strong. The state's effective property tax rate averages roughly 0.52% to 0.53%, the second-lowest in the country behind only Alabama, according to Tax Foundation and county assessor data compiled in 2026. On May 6, 2026, Governor Sarah Huckabee Sanders signed HB 1001 and SB 1 following a special legislative session, cutting the top individual income tax rate to 3.7%, retroactive to January 1, 2026. That is the fourth consecutive annual cut and the lowest the rate has been since Arkansas's income tax began in 1929. For an out-of-state investor comparing Arkansas against a higher-tax market on rental income, that combination is real money.

Where the story gets more complicated is the Homestead Tax Credit under Arkansas's Amendment 79, worth roughly $375 a year off the property tax bill. It applies only to a homeowner's primary residence. Investment property gets none of it, which means the advertised statewide 0.52% average overstates what an investor actually pays. A non-homestead property in Pulaski County, home to Little Rock, runs closer to 0.90% to 1.0% effective once that credit and local millage are accounted for. It is the same pattern PropertyPundit has now confirmed in half a dozen states this year: the tax rate everyone quotes is the owner-occupied rate, and the investor rate is meaningfully higher.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

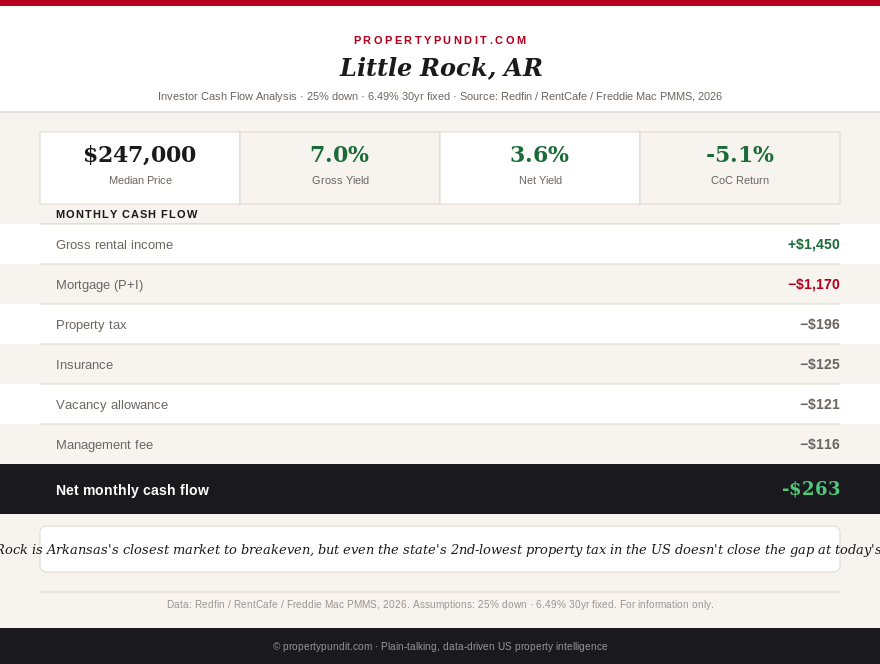

Little Rock: the state's closest call on cash flow

Little Rock's median sale price sits at $247,000 (Redfin, February 2026, up 5.3% year over year), while Zillow's home value index for the metro runs lower, around $197,594, a divergence pattern that shows up whenever Redfin's transaction-based median and Zillow's smoothed value index are pulled from different slices of the same market. Using the $247,000 transaction price, a 25% down payment is $61,750 on a $185,250 loan. At 6.49% over 30 years, principal and interest runs about $1,170 a month.

A 3-bedroom single-family rental in Little Rock rents for roughly $1,450 a month, based on RentCafe's 2026 metro average, though citywide indexes like this one typically understate true single-family rent compared to apartment stock. Add Pulaski County's non-homestead property tax at an estimated 0.95% ($196/month) and landlord insurance around $125/month, factoring in Arkansas's real exposure to hail and tornado claims, and total PITI lands near $1,490. That puts gross DSCR at 0.97, just under the 1.0 minimum most DSCR lenders require to qualify a deal without additional reserves. After an 8% property management fee and an 8% vacancy allowance applied to gross rent, effective cash flow comes out to roughly negative $263 a month.

So what does this mean for you: Little Rock isn't a cash-flow machine, but it's the only market in this spotlight that gets within shouting distance of breakeven, and a buyer willing to put 30% or more down, or negotiate below list in a market with rising inventory, has a real shot at flipping that DSCR above 1.0.

Northwest Arkansas: Walmart's gravity, not rent, drives the math

Fayetteville, Bentonville, and Rogers make up the Fayetteville-Springdale-Rogers metro, anchored by Walmart's global headquarters, J.B. Hunt, Tyson Foods, and the University of Arkansas. It is one of the fastest-growing corporate and population corridors in the South, and prices reflect it. Fayetteville's median sale price is $395,000 (Redfin, three months ending May 2026), Bentonville sits at $430,000, and Rogers leads the region at $440,000, according to 2026 year-to-date sales data compiled by NWA Look.

Run Fayetteville through the same underwriting: 25% down on $395,000 is $98,750, financing $296,250 at 6.49% for a principal and interest payment near $1,871. Washington County's non-homestead property tax runs an estimated 0.60% effective ($198/month), and insurance adds roughly $140/month, putting PITI at about $2,208. Against a 3-bedroom rent of roughly $1,550, DSCR comes in at 0.70. After management and vacancy, cash flow runs about negative $896 a month. Bentonville isn't meaningfully better: on the $430,000 median with an estimated $1,850 rent, DSCR lands at 0.77 and cash flow after expenses runs roughly negative $829 a month.

So what does this mean for you: Northwest Arkansas is an appreciation and corporate-relocation thesis, not a rental-yield thesis. If you believe Walmart's continued headquarters investment and the university's growth will keep pushing prices up for another five to ten years, the equity case may still work. If you are underwriting for monthly cash flow today, the numbers say to look elsewhere in the state.

The tax advantage is real, it just doesn't rescue the deal

It is worth being precise about what Arkansas's tax structure actually buys an investor. On a $247,000 Little Rock property, the property tax gap alone between Arkansas's 0.95% non-homestead rate and a higher-tax state like New Jersey's 2.23% works out to roughly $2,633 a year, or about $219 a month, entirely in Arkansas's favor. The income tax cut to 3.7% adds further savings on any positive taxable rental income, though depreciation typically shelters most or all of that in the early years of ownership anyway. Both of those are genuine, durable advantages that will still be there in five years.

What they aren't is a fix for a negative DSCR. A $219 monthly property tax advantage doesn't close a $263 monthly cash flow gap in Little Rock, let alone the $829 to $896 gap in Northwest Arkansas. The math points toward a specific kind of Arkansas deal working today: an entry-level Little Rock property purchased below the $247,000 median, with 30% or more down, ideally near military or state-employment demand that keeps vacancy low, rather than the median-priced property in either Little Rock or the Northwest Arkansas growth corridor.

For a closer look at how DSCR math shifts once you factor in property management costs specifically, see our breakdown of property management fees for investors. If HOA-encumbered properties are part of your search in either market, our analysis of HOA fees and investor cash flow shows how quickly a modest monthly fee can push a marginal DSCR below the 1.0 lending threshold. And for the broader mechanics of how DSCR lenders qualify a deal in the first place, our guide to DSCR underwriting walks through the qualification math step by step.

Most investors who run Arkansas's full numbers, not just the headline tax rates, end up in the same place: this is a state worth watching for the next rate-cut cycle, and worth buying into selectively below-median today, rather than a market where the median listing is the deal.