You watched a rate lock request cost you money you didn't have to spend, and it wasn't because of a jobs report or an inflation print. It was because two countries on the other side of the world started shooting at each other again. If you've been sitting on a pre-approval, refreshing rate trackers every morning, and wondering whether the number you're seeing has anything to do with your actual finances, it doesn't. Not this week's move, anyway.

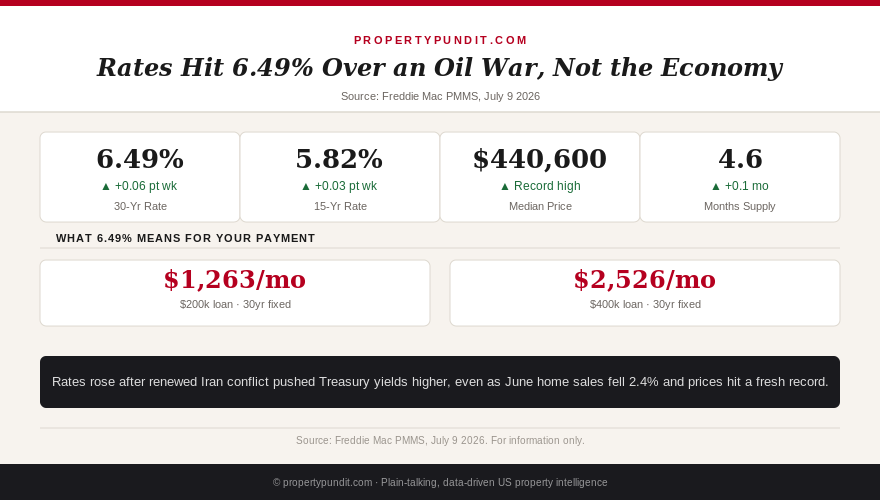

Freddie Mac's Primary Mortgage Market Survey put the 30-year fixed at 6.49% for the week ending July 9, 2026, up from 6.43% the week before. Daily lender quotes from Zillow and other trackers are already running closer to 6.7%. The trigger: the US and Iran traded new strikes this week, a ceasefire that had been holding fell apart, and Treasury yields, which mortgages track, moved higher on fears that oil prices will keep inflation elevated. None of that has anything to do with your credit score, your income, or the house you're looking at.

What actually moved this week

Mortgage applications fell 2.2% for the week ending July 3, according to the Mortgage Bankers Association, with purchase applications down 1% and refinance applications down 4%. That's the applications data catching up to a rate environment that was already drifting higher before this week's escalation. The 15-year fixed also ticked up, to 5.82% from 5.79%.

Here's the part that gets lost in the daily rate-tracker panic: a 0.06-percentage-point move is real money, but it is not the thing that should be driving your decision. On a $451,250 loan, the gap between 6.43% and 6.49% is about $18 a month. That's roughly the cost of a couple of coffee runs, not the difference between affording a house and not affording one. So what for you: if you're refreshing rate alerts three times a day over half-a-point movements caused by a war you have no control over, you're spending anxiety on the wrong number.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

A record price complicates the "just wait" instinct

The National Association of Realtors released its June 2026 existing-home sales report this week: sales fell 2.4% from May to a 4.09 million annualized pace, but the median price hit $440,600, a record for the month and the 36th straight month of year-over-year price gains. That looks like a contradiction. Fewer people bought homes, and the ones who did paid more than ever.

It isn't actually a contradiction once you separate volume from price. Sales volume can fall because affordability is squeezing out marginal buyers, while the median price still climbs because the buyers who remain, often move-up buyers with more equity or cash, skew toward higher-priced homes. NAR's own Housing Affordability Index actually improved to 102.3 in the same period, up from 95.5 a year earlier, meaning a household earning the median income can technically afford the median home again, barely, mostly because incomes have grown faster than rates have. So what for you: a record headline price doesn't mean the math got worse for you specifically. It means the mix of buyers shifted, and your actual affordability may be better than the headline suggests.

What waiting for a better rate actually costs

Say you're eyeing a $475,000 home in Nashville, close to the current three-month median there, with 5% down. That's a $451,250 loan. At this week's 6.49%, principal and interest runs about $2,850 a month. Add Davidson County property tax at roughly 0.81% ($321/month), landlord-grade homeowners insurance around $120/month, and PMI in the $230/month range at a mid-tier credit score, and you're at roughly $3,521 a month. On $112,000 in annual income, that's about 37.7% of gross pay going to housing, well past the 28% rule most lenders and planners use as a comfort line.

That math doesn't fix itself by waiting for rates to drop half a point. It fixes itself by changing the price, the down payment, or the terms. And this is where the current market actually works in your favor: Nashville has a 39.1% price-cut rate right now and roughly 70 days on market, both signs of a market where sellers are negotiating, not dictating. So what for you: the lever you can actually pull this week isn't the 10-year Treasury. It's the asking price, and in this market, that lever has real give in it.

Why the daily rate you see online looks even worse

If you've checked a rate quote online this week and seen something closer to 6.7% rather than the 6.49% PMMS headline, you're not imagining it. Mortgage rates normally trade about 1.7 to 2.0 percentage points above the 10-year Treasury yield. That spread has been running wide this year, closer to 2.0 points than the historical norm, and war-driven Treasury spikes tend to widen it further before lenders' daily pricing catches up to the official weekly survey. The PMMS is still the right number to anchor your expectations to, since it reflects an actual weekly average of closed-loan pricing rather than a single lender's live quote, but expect the number your loan officer quotes you to run somewhat hotter than the headline for the next week or two.

Here's what that means in real payment terms across a few loan sizes at this week's 6.49% PMMS average: a $200,000 loan runs about $1,263 a month in principal and interest, a $300,000 loan about $1,895, and a $400,000 loan about $2,526. Compare that to 6.43% the week before, where the same $400,000 loan would have run about $2,510, a $16 difference that scales roughly in proportion to loan size. So what for you: whatever loan amount you're actually shopping at, you can translate this week's headline into your own real number in about thirty seconds, and it's almost certainly smaller than the anxiety the headline itself is generating.

Lock, float, or negotiate: the real decision

The classic advice, lock if you're closing soon, float if you have time and can stomach the risk, still applies, but it's the smaller decision this week. The bigger one is whether to chase a lower rate that geopolitics may or may not deliver, or use the negotiating room that already exists. A seller in a market with a 39% price-cut rate is a seller who will often take a lower offer, cover part of your closing costs, or fund a temporary rate buydown rather than watch the listing sit. None of that requires the Iran conflict to resolve.

Run the numbers on your own closing costs before you decide how much negotiating room to ask for, and if you're financing with less than 20% down, check where your credit score actually lands you on the rate sheet, since that spread often dwarfs a single week's PMMS move. And if the 20% down payment number is the thing keeping you on the sidelines, it shouldn't be: most first-time buyers don't put down anywhere near that much.

The call

Frankly, if you're a Nashville buyer sitting on a pre-approval and waiting for the Iran conflict to cool off before you write an offer, the math points toward acting on price instead. A rate that moves half a point on war headlines can move back just as fast, or it can stay elevated for months, and nobody, including us, can tell you which. What you can control this week is the offer you make in a market where more than a third of sellers have already cut their price once. Most buyers who run these numbers end up negotiating the purchase price down rather than gambling on a geopolitical outcome they can't influence.