You've been eyeing Sacramento because it's the cheaper ticket into California without the coastal premium, and you keep glancing at Reno because it's two hours away, has no state income tax, and the listings look scarier on price alone. You've been running the comparison backward. The city with the lower sticker price is not the city with the lower bill, and at $112,000 a year, the gap between what you'd pay on paper and what actually leaves your account every month is bigger than either city's asking price suggests.

Sacramento's median sale price has held in the $500,000 range through the first half of 2026, according to Redfin's three-month tracking. Reno is meaningfully more expensive on paper, with a median in the $554,000 to $575,000 range depending on the source; call it $560,000. On sticker price, Sacramento wins by $60,000. On the number that actually determines your monthly budget, it doesn't win at all.

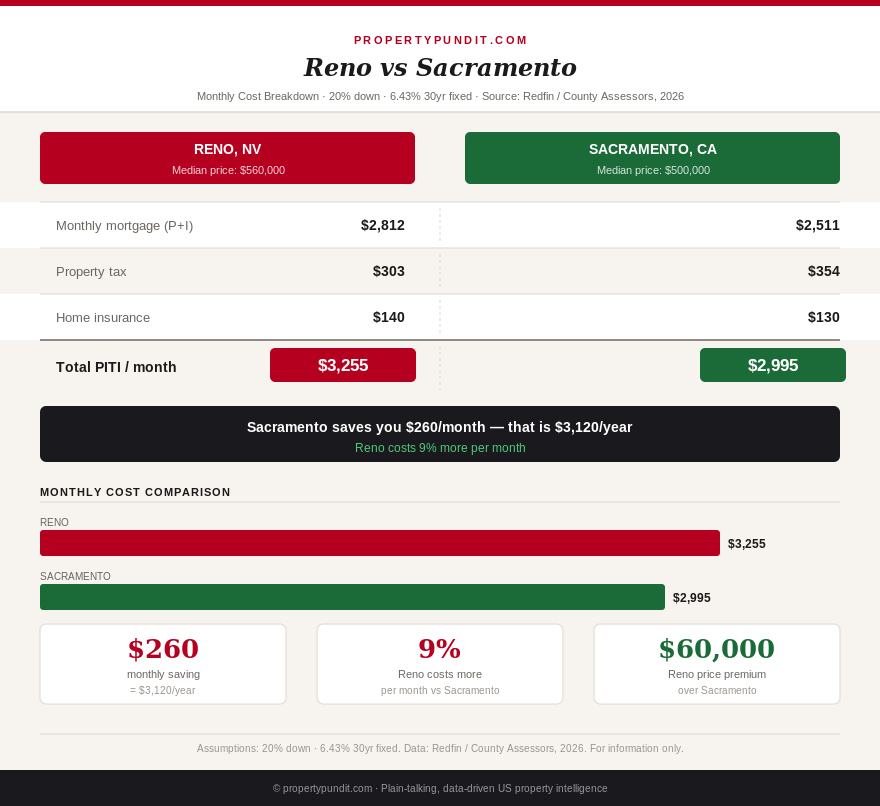

The mortgage and tax math, side by side

Assume 20% down and today's 6.43% 30-year fixed rate for both. On Sacramento's $500,000 median, a $400,000 loan runs $2,511 a month in principal and interest. Add Sacramento County's roughly 0.85% effective property tax, once modest special assessments common in newer developments are factored in, for $354 a month, plus an estimated $130 in homeowner's insurance. That's a $2,995 PITI.

Reno's $560,000 median, financed the same way, means a larger $448,000 loan and a $2,812 monthly principal and interest payment, meaningfully more than Sacramento's. Washoe County's effective property tax runs lower, around 0.65%, adding $303 a month, with an estimated $140 in insurance given Reno's wildfire exposure from the nearby Sierra foothills. That's a $3,255 PITI, $260 a month more than Sacramento before a single tax return is filed.

| Monthly line item | Sacramento, CA | Reno, NV |

|---|---|---|

| Median price | $500,000 | $560,000 |

| Down payment (20%) | $100,000 | $112,000 |

| Principal & interest | $2,511 | $2,812 |

| Property tax | $354 | $303 |

| Insurance (est.) | $130 | $140 |

| PITI | $2,995 | $3,255 |

| State income tax (est., $112k income) | $580 | $0 |

| All-in monthly cost | $3,575 | $3,255 |

Sacramento's PITI alone is $260 a month cheaper than Reno's. But California's graduated state income tax, up to 13.3% at the top bracket, costs a $112,000 earner an estimated $580 a month, using 2026 California Franchise Tax Board brackets. Nevada has no state income tax on wages at all. Add that back in and Sacramento's advantage doesn't just shrink, it flips: Reno comes out $320 a month cheaper, all in, despite a $60,000 higher purchase price and a $12,000 bigger down payment. If your down payment fund is the binding constraint on your timeline to buy, that extra $12,000 upfront is real, but it's a one-time cost against a monthly saving that compounds for as long as you own the home.

Why the "cheaper" city isn't actually cheaper

This is the same trap this newsletter has flagged in Texas-adjacent and no-income-tax comparisons all year: a lower purchase price and a lower property tax rate both look like savings on a listing page, but neither number tells you what actually leaves your paycheck. California's property tax is capped near 1% of purchase price under Prop 13, which sounds like a win next to Reno's own moderate rate, but California's income tax is the real cost driver here, and it applies whether you rent or own. Most buyers comparing Sacramento to a no-income-tax city price the mortgage and stop there. The mortgage was never the whole bill.

If you're weighing a move for the tax savings alone, run your specific income through both states' brackets before you assume Reno wins by default. The $580-a-month gap modeled here is specific to a $112,000 salary; earn less and California's lower brackets close some of the gap, earn more and the 9.3% and 13.3% brackets widen it further in Reno's favor.

The honest number: neither city clears the affordability rule

At $112,000 income, the standard 28% housing-cost guideline caps monthly PITI near $2,613. Sacramento's $2,995 PITI blows past that ceiling by $382 a month before state tax is even considered. Reno's $3,255 PITI misses it by an even wider $642 a month. Neither city is a comfortable fit for a single $112,000 income with just 20% down, and pretending otherwise would be the kind of vague advice this newsletter doesn't do. A bigger down payment, a co-borrower's income, or a lower-priced entry neighborhood within either metro, think Elk Grove or Rancho Cordova outside Sacramento, or Sparks and Cold Springs outside Reno, are the realistic paths to making either market work on this income.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The call

If you're set on one of these two cities specifically, and your credit and down payment plan are otherwise ready, the math points toward Reno despite the scarier-looking price tag. The $60,000 premium is a one-time number on a purchase contract; the $580-a-month California income tax bill follows you every year you live and earn there, whether you rent or own. Most people who run these numbers end up surprised that the "expensive" city was the better deal, and factor that into their search radius before they factor in closing costs or anything else. If neither PITI fits your budget today, that's the more urgent number to solve before the state-tax question matters at all.