You ran an online affordability calculator and it told you $310,000. Your loan officer came back with $265,000. Nothing about your income changed between those two numbers, and no one explained the gap. The gap is your debt-to-income ratio, and once you understand which of your monthly bills a lender actually counts, that $45,000 difference stops feeling like a mystery.

Debt-to-income ratio, or DTI, is simply your total monthly debt payments divided by your gross monthly income, before taxes come out. Most online calculators only ask about the mortgage you're hoping to get. Real underwriting adds in everything else you already owe, and that's where the online number and the real number diverge.

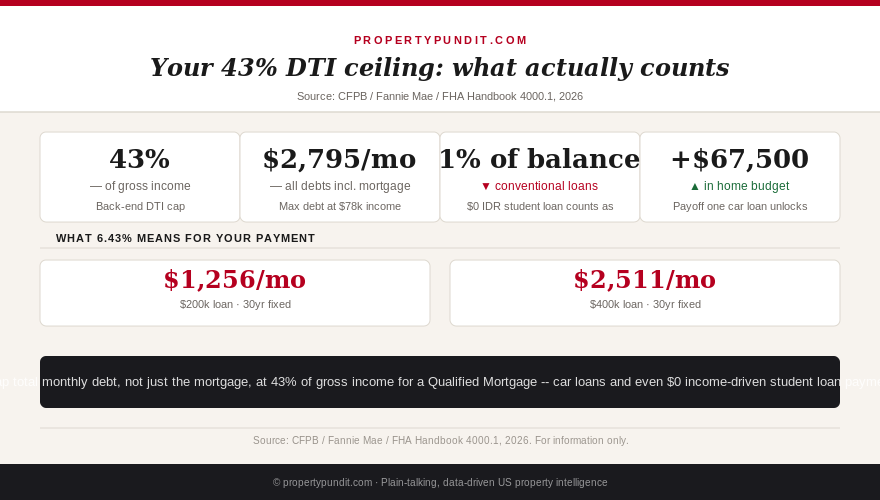

Front-end versus back-end: two ratios, not one

Lenders actually track two separate ratios. Front-end DTI covers only housing costs: principal, interest, property tax, homeowners insurance, and any HOA dues, generally capped around 28% to 31% of gross income depending on loan type. Back-end DTI adds every other debt payment on top of housing and is the number that usually determines your real ceiling, generally capped at 43% for a Qualified Mortgage, with some conventional loans stretching to 45% or even 50% for borrowers with strong credit or a large down payment.

The 43% figure isn't arbitrary. It traces back to the Consumer Financial Protection Bureau's Qualified Mortgage rule, created after Dodd-Frank, which originally set a hard cap at that number for a loan to count as a "qualified" mortgage with stronger borrower protections. The CFPB has since loosened the hard cap in favor of price-based thresholds for most conventional loans, but 43% remains the number every lender, and every calculator worth using, still treats as the real-world ceiling. If a house you're eyeing pushes your back-end DTI meaningfully past 43%, expect a harder conversation with your underwriter regardless of what the sticker price suggests you can afford.

What actually counts against you

Every recurring debt obligation on your credit report factors in: minimum credit card payments, car loans, personal loans, child support or alimony, and student loans. Student loans are the most misunderstood line item on this list. If your loan is on an income-driven repayment plan showing a $0 monthly bill, conventional loans (Fannie Mae and Freddie Mac guidelines) still count 1% of your outstanding balance as the qualifying payment, and FHA loans use whichever is greater: your actual reported payment or 0.5% of the balance. A $0 statement from your loan servicer does not mean $0 counted against you at the mortgage desk, and buyers who assume otherwise are routinely surprised by a lower pre-approval number than they expected.

What doesn't count: utilities, insurance premiums outside of homeowners insurance, subscriptions, groceries, and any expense that isn't a fixed, reported monthly debt obligation. Your DTI is a narrower measure than your real household budget, which is exactly why a mortgage payment that clears the DTI test can still feel tight once rent, groceries, and gas come out of the same paycheck.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The math at $78,000 income

At $78,000 a year, gross monthly income is $6,500. A 43% back-end cap allows total monthly debt of $2,795. Say you're carrying a $300 student loan payment, a $400 car payment, and $150 in credit card minimums, $850 a month in existing debt. That leaves $1,945 a month for the entire housing payment, principal, interest, taxes, and insurance combined.

On a $270,000 home in a typical Atlanta-area suburb, taxes and insurance run roughly $300 a month, leaving about $1,645 for principal and interest. At 6.43%, that supports a loan of roughly $262,000, which lines up almost exactly with a $270,000 purchase at 3.5% down on an FHA loan. That's not a coincidence: it's the ceiling your existing debt has already set, whether or not a listing agent ever mentions it.

Now remove just the $400 car payment from the picture. Your available housing budget jumps to $2,345 a month, supporting a loan of roughly $326,000 and a purchase price closer to $337,500, about $67,500 more home for the identical income and the identical mortgage rate. That single line item is worth more to your budget than most rate-shopping effort ever will be.

How to actually move the number

Paying off a loan entirely removes its payment from the calculation; paying it down without eliminating it usually doesn't help nearly as much, since the minimum payment often barely moves until the balance is very low. Prioritize the debt with the highest monthly payment relative to its remaining balance, which is frequently a car loan rather than a larger but slower-amortizing student loan. Avoid financing anything new, including furniture or a car, in the months before you apply, since a new account resets your DTI calculation right when you need it lowest. Adding a co-borrower can raise your combined income, but their debts get added to the ratio too, so it only helps if their income-to-debt profile is stronger than yours alone.

Most people who run these numbers find that one specific bill, not their overall spending habits, is the actual ceiling on their home search. Before you widen your price range or accept a smaller house than you wanted, pull your credit report, add up every payment a lender would count, and find that one bill. If a car loan, personal loan, or credit card balance is close to being paid off anyway, closing it out before you apply is frequently the single most effective move available to a first-time buyer, well ahead of the incremental gains from improving your credit score or shopping for a marginally lower rate.

DTI works alongside, not instead of, the other qualifying numbers a lender checks. Down payment size still matters, which is why understanding the real minimum down payment rather than the 20% myth changes how much cash you need to have ready. Loan type matters too: FHA and conventional loans apply the student-loan qualifying rule differently, covered in full in our FHA versus conventional breakdown. And once you know your real monthly ceiling, understanding how that payment actually gets applied to your loan each month shows you exactly what you're paying for.