You make $112,000 a year, the job could take you to Phoenix or Tampa, and you have already made up your mind based on the obvious story: Arizona has cheap property tax, Florida has no income tax at all, so it should be a coin flip that leans slightly toward whichever city has the better weather in July. Run the actual numbers, including the insurance bill nobody mentions until you are already under contract, and the coin flip resolves. It just does not resolve the way the obvious story predicts.

Here is the full monthly cost table for both cities, and the one line item that flips the entire comparison.

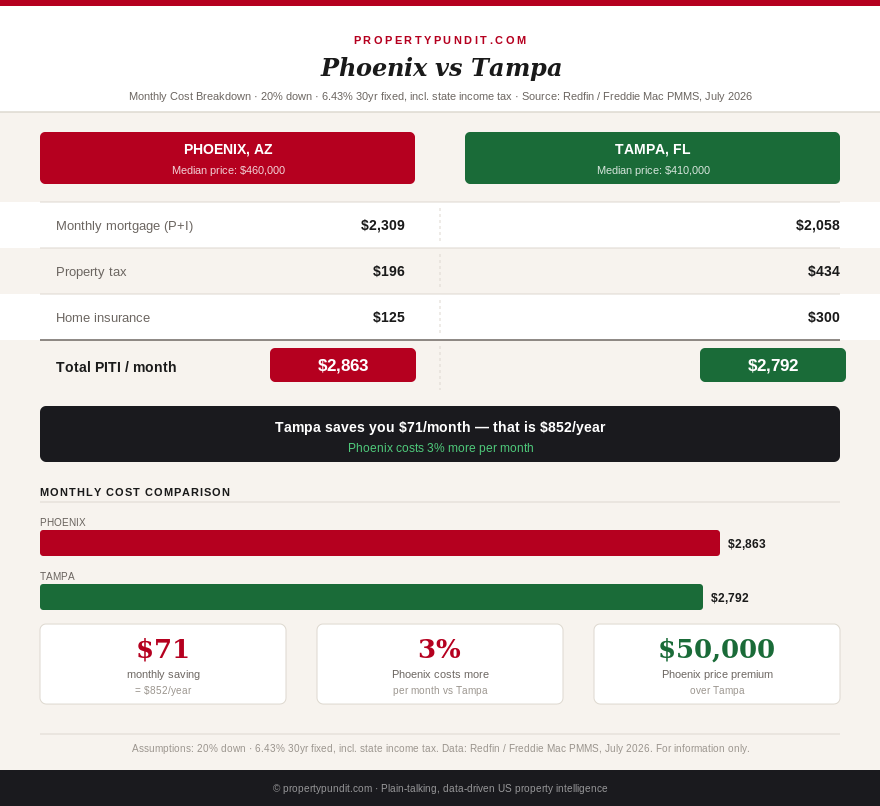

The side-by-side monthly cost table

All figures below use 20% down payment and a 6.43% 30-year fixed rate (Freddie Mac PMMS, July 2, 2026). Income tax uses 2026 state rates at $112,000 gross income.

| Item | Phoenix, AZ | Tampa, FL |

|---|---|---|

| Median home price | $460,000 | $410,000 |

| 20% down payment | $92,000 | $82,000 |

| Loan amount | $368,000 | $328,000 |

| Monthly P&I at 6.43% | $2,309 | $2,058 |

| Property tax/month | $196 (0.51%, Maricopa Co.) | $434 (1.27%, Hillsborough Co.) |

| Homeowner's insurance | $125 | $300 |

| PITI total | $2,630 | $2,792 |

| PITI as % of $112k income | 28.2% (at the ceiling) | 29.9% (over the ceiling) |

| State income tax/month | $233 (2.5% flat, AZ) | $0 (no state income tax) |

| All-in monthly cost | $2,863 | $2,792 |

| Tampa monthly advantage | $71/month |

Sources: Redfin median home prices (Phoenix, Tampa; three months ending May 2026), Maricopa County Assessor effective rate (SmartAsset, Tax Foundation, 2026), Hillsborough County Property Appraiser (2026), Arizona Department of Revenue flat rate (2.5%, 2026), Florida Department of Revenue (no state income tax), Freddie Mac PMMS (July 2, 2026), Insurance industry premium estimates for Tampa metro (2026).

The so-what for you: Phoenix's PITI alone is genuinely lower than Tampa's, by $162 a month, and if you stopped the analysis there, Phoenix would look like the clear winner. It is only once Arizona's income tax gets added to the comparison that the full picture flips, and $71 a month is not a rounding error over a 30-year hold. It is $852 a year, and roughly $25,600 over a decade if neither state changes its tax code.

The line item everyone skips: what insurance actually costs in each city

Arizona's low property tax gets mentioned in almost every "best states for homeowners" list. Tampa's hurricane exposure gets mentioned too, but usually as a vague warning rather than a specific dollar figure. The reality: homeowners insurance estimates for a typical Tampa-area home at this price point range from roughly $2,000 to $6,000 a year depending on dwelling coverage, deductible, and whether the home has had a wind mitigation inspection, which can meaningfully lower a premium (various Florida insurance industry sources, 2026). Phoenix carries essentially no comparable catastrophe-risk premium; a typical policy runs closer to $1,200 to $1,800 a year.

The math above uses a middle-of-range $3,600 annual estimate for Tampa, which is already a real cost disadvantage of $2,100 a year against Phoenix before any other factor is considered. So what this means for you: if you are the kind of buyer who assumes "no income tax" automatically means "cheaper," Tampa's insurance bill is the specific number that should make you run your own quote before assuming that logic holds. It very nearly does not.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Neither city comfortably clears the 28% rule at $112k

This is the part of the comparison that matters more than which city wins by $71. Phoenix's mortgage-only PITI sits at 28.2% of gross income, essentially right at the ceiling most lenders and financial planners use as a comfort threshold. Tampa's runs to 29.9%, already over that line before Florida's higher property tax and insurance are even weighed against Arizona's income tax. Once Phoenix's income tax is added into an all-in comparison, its real burden climbs to 30.7% of gross income, worse than Tampa's mortgage-only 29.9%.

So what this means for you: at $112,000 income, neither city is a comfortable purchase at 20% down under today's rates. Both are financially feasible, not comfortable, and a buyer choosing between them should plan for near-zero monthly slack rather than assuming the winning city has meaningful breathing room. If a raise, a bonus, or a larger down payment is on the table before you buy, either city becomes materially easier to carry; without one, both require a tight household budget from day one. The closing costs breakdown is worth reading before you commit to either market, since the cash-to-close number, not just the monthly payment, is what determines how much cushion is left after moving day.

What the spreadsheet does not capture

Phoenix offers a genuinely lower cost of living outside of housing in several categories, a large and growing tech and semiconductor employment base anchored by Taiwan Semiconductor's Arizona expansion, and a dry climate that some buyers strongly prefer over Florida humidity. Tampa offers coastal access, no state income tax on any future raises or bonuses, which matters more the higher your income climbs over time, and a lower cost of living than Miami or South Florida while still offering beach proximity. Neither advantage shows up in a monthly PITI table, and both are legitimate reasons a buyer might choose one city over the other regardless of the $71 gap.

Climate risk is the other consideration the spreadsheet understates. Tampa's insurance premium reflects hurricane exposure that is a real, ongoing risk to the property itself, not just a cost line, and Florida's insurance market has seen multiple carriers exit or restrict new business in the past several years. Phoenix carries its own long-term risk in extreme heat and water availability, which is a slower-moving concern but a real one for anyone planning to hold the property for decades.

The verdict at $112k income in July 2026

The math points toward Tampa by a modest but real margin, $71 a month, once every tax and insurance line item is counted honestly rather than relying on the "no income tax state" shortcut that most buyers use to skip the analysis. That margin is not large enough to override a genuine career opportunity, a family preference, or a strong personal pull toward one climate over the other. It is large enough that anyone treating "Florida has no income tax" as the entire financial case for Tampa, or "Arizona has cheap property tax" as the entire case for Phoenix, is working from an incomplete picture. Get an actual insurance quote for the specific property you are considering in Tampa before you finalize a decision either way; the $3,600 estimate here is a reasonable middle figure, but it swings by thousands of dollars a year based on the individual home's age, roof condition, and wind mitigation status. For buyers weighing a similar income-tax-versus-property-tax tradeoff in a different pair of cities, the Charlotte vs Columbus comparison runs the same kind of analysis for a different regional matchup, and the Nashville vs Huntsville comparison shows how a lower-tax neighboring city can still lose on total monthly cost once income tax is added back in.