If you are living in Nashville, earning $112k, and watching the housing math fail you month after month, there is a city two hours south that cleared the 28% affordability guideline with $820 per month to spare. Huntsville, Alabama has a $340k median home price, a defense and aerospace employment base that is adding 1,400-plus U.S. Space Command positions by 2027, and a property tax rate so low it barely registers in the PITI calculation. This comparison does not require you to love Huntsville over Nashville. It requires you to know what the gap actually costs.

The counterintuitive finding: even after accounting for Alabama's 5% state income tax — which Tennessee does not have — the all-in monthly cost in Huntsville is still $633 less than Nashville. That is $7,596 per year. Over five years of homeownership, it is $37,980. And Huntsville home prices rose 3.5% year over year in May 2026 (Redfin), faster than Nashville's 0.5%.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The raw PITI comparison at $112k income

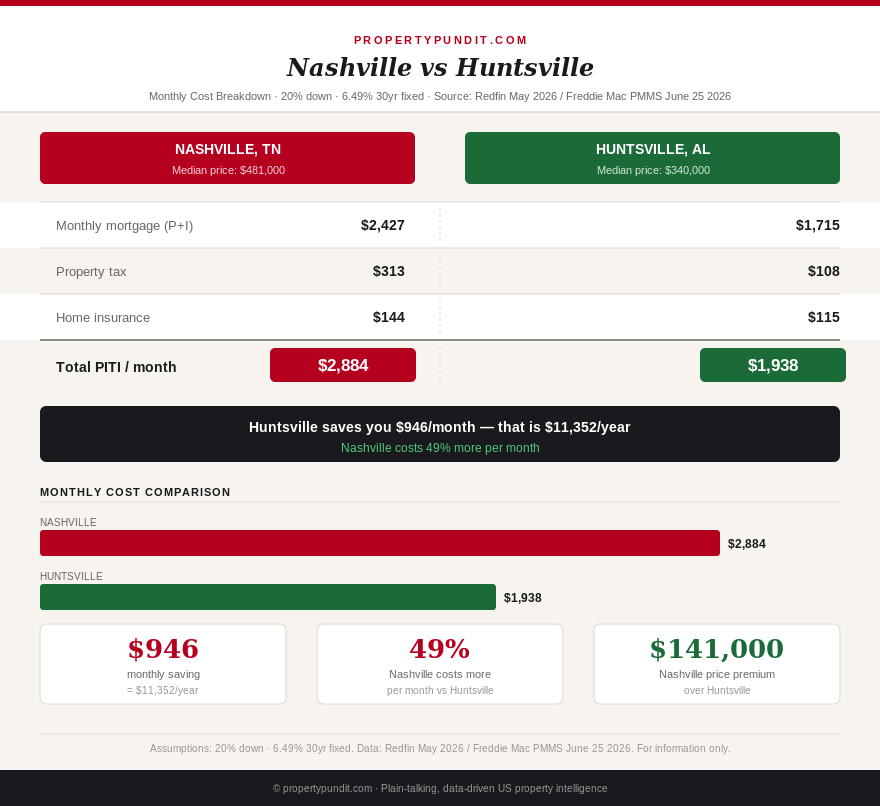

The 28% housing rule is the widely used guideline that says your monthly PITI payment should not exceed 28% of your gross monthly income. At $112k annual income, gross monthly is $9,333. The ceiling is $2,613.

Nashville at the $481k median, 20% down, 6.49% rate:

- Down payment: $96,200

- Loan amount: $384,800

- P&I at 6.49% (30-year fixed): $2,427/month

- Davidson County property tax (0.78% effective): $313/month

- Homeowner's insurance: $144/month

- Total PITI: $2,884/month

- As a share of $112k gross income: 30.9% — exceeds the 28% guideline by $271/month

- Tennessee state income tax: $0

Huntsville at the $340k median (Redfin, May 2026), 20% down, 6.49% rate:

- Down payment: $68,000

- Loan amount: $272,000

- P&I at 6.49%: $1,715/month

- Madison County property tax (0.38% effective — Alabama's rates are notably low): $108/month

- Homeowner's insurance: $115/month (Alabama has lower coastal risk premiums than the Gulf Coast)

- Total PITI: $1,938/month

- Wait — Alabama has state income tax at 5%. At $112k income, roughly $5,490/year ($458/month).

- Tennessee income tax saving for Nashville: $458/month (zero income tax)

All-in monthly comparison including state income tax:

| Cost component | Nashville, TN | Huntsville, AL | Difference |

|---|---|---|---|

| Median home price | $481,000 | $340,000 | -$141,000 |

| Down payment (20%) | $96,200 | $68,000 | -$28,200 |

| P&I payment | $2,427 | $1,715 | -$712 |

| Property tax/month | $313 | $108 | -$205 |

| Insurance/month | $144 | $115 | -$29 |

| PITI total | $2,884 | $1,938 | -$946 |

| State income tax on $112k | $0 (TN zero tax) | $458 (AL ~5%) | +$458 |

| All-in monthly (PITI + state tax) | $2,884 | $2,396 | -$488/mo (Huntsville wins) |

| % of $112k income | 30.9% (fails 28% rule) | 24.7% (clear headroom) |

Sources: Redfin median prices May 2026; Freddie Mac PMMS June 25 2026 (6.49%); Madison County, AL assessor effective rate 0.38%; Davidson County, TN effective rate 0.78%; Alabama Department of Revenue income tax schedule 2026.

Even with Alabama's income tax fully loaded into the calculation, Huntsville saves $488 per month all-in compared to Nashville. If you are buying at 20% down rather than waiting, Huntsville also requires $28,200 less in cash at closing.

What Huntsville's employment base actually looks like

The city everyone thinks of as a sleepy Southern town has been the center of US missile defense and space program engineering for 70 years. Redstone Arsenal is a 38,000-acre federal research and development installation housing the Missile Defense Agency, Army Materiel Command, Army Aviation and Missile Command, and the FBI's Counterintelligence unit — among others. More than 40,000 military and government civilian employees work on or around the installation.

The most significant recent development: U.S. Space Command is relocating its headquarters to Redstone Arsenal. More than 1,400 military and civilian positions are moving by 2027, bringing with them thousands of contractor jobs from Boeing, Lockheed Martin, Northrop Grumman, Leidos, SAIC, and similar firms that operate where Space Command operates. Blue Origin's manufacturing and research facility in Madison (part of the Huntsville metro) employs over 1,500 engineers and technicians.

The practical implication for a buyer: the Huntsville economy is federal government and defense contractor revenue. These are the most recession-resistant employers in the country. They do not disappear in a downturn. They do not relocate when a tech winter arrives. For someone evaluating job security risk in a home purchase at 6.49% rates, Huntsville's employment base is structurally different from a private-sector tech market.

Nashville's employment story is strong — it is the capital of Tennessee, has a major healthcare and education sector (Vanderbilt, HCA Healthcare, Bridgestone's Americas HQ), and a growing tech presence. But its housing market has priced in that story: the median was $481k in Q1 2026 after a 48% appreciation run from 2019 to 2022. That run has stalled, with Nashville now essentially flat year over year (-0.5%, Redfin May 2026) after the appreciation catch-up years.

Price appreciation: who is actually growing faster right now

The story most people tell about Nashville is that it will always appreciate faster because of its brand recognition and population growth. The data in 2026 disagrees with the short-term version of that story.

Nashville: -0.5% year over year in May 2026 (Redfin). Price cuts at 75.5% of spring sales — the highest seller concession rate of any major US metro. Active inventory up, buyer pool stretched by affordability.

Huntsville: +3.5% year over year in May 2026 (Redfin). Inventory growth of 5-10% improving buyer selection without creating oversupply. The Space Command announcement has added a visible demand catalyst that is not yet fully priced in.

On a $340k Huntsville purchase at 3.5% appreciation, the home is worth roughly $399k in 5 years — a $59k equity gain. On an $481k Nashville purchase at 0.5% appreciation, the home is worth about $493k — a $12k equity gain. This is not a projection of future performance; it is the current trajectory reflected in verified data.

Closing costs, seller concessions, and what the market feels like to buy in

Nashville's 75.5% seller concession rate means buyers have real negotiating power. As covered in our Nashville concessions explainer, sellers in Nashville are currently covering closing costs, rate buydowns, and inspection credits at a rate that was unimaginable three years ago. If you buy in Nashville and negotiate a 2-3% concession, that can recover $9,600 to $14,430 in closing costs on a $481k purchase — a meaningful offset to the higher price.

Huntsville's market is more balanced. Inventory growth of 5-10% gives buyers genuine selection, but the concession environment is less favorable than what Nashville's softening market currently offers. You are likely to negotiate a 1-2% concession in Huntsville, recovering $3,400 to $6,800 in closing costs. A clean offer with standard contingencies is competitive without requiring a bidding war escalation.

On a 10% down payment instead of 20%, the PITI gap widens slightly in Huntsville's favor: at 10% down, PMI adds roughly $175/month to Huntsville and $248/month to Nashville at the respective loan sizes and typical PMI rates. The relative advantage is similar.

Which city wins, and for whom

Huntsville wins for a buyer at $112k income who needs to fit a mortgage inside the 28% rule and wants positive cash flow from day one. It wins for a buyer who values recession-resistant employment over brand-name city appeal. It wins for a buyer whose work is remote or whose employer has a Huntsville or regional Alabama presence.

Nashville wins if your employment is Nashville-specific — healthcare leadership, country music industry, state government, or a company headquartered downtown. Nashville also wins if you are a buyer with sufficient income that the $2,884 PITI is comfortably within range — approximately $124k gross would bring Nashville to 27.9% of income. And it wins for buyers who believe the long-run appreciation story will reassert itself once rates ease toward 5.5% and the lock-in effect begins to loosen seller supply.

Frankly, at $112k income in 2026, Huntsville fits the math and Nashville does not. That is the most direct way to say it. A buyer who can genuinely do both should weigh the employment situation and career path first — the financial gap narrows significantly if one city requires commuting costs, career change, or a dual-income shift that the other does not. But if the employment situation is genuinely neutral, the numbers point toward Huntsville: it is $488/month cheaper all-in, appreciating faster right now, and building a defense employment base that the federal government has spent 70 years concentrating in one place.