The letter from your servicer says your payment is going up $167 a month starting next month, and you locked a fixed rate specifically so this couldn't happen. You call the servicer, and the person on the phone tells you the rate didn't change at all. What changed is your escrow account, the part of your payment covering property tax and insurance, and it just posted a shortage. If you bought your first home in the last two or three years at $78,000 income in Atlanta or anywhere else, this letter is probably sitting in your inbox or your mailbox right now, and it is catching a lot of first-time buyers off guard in 2026.

Here is what actually happened, why it is hitting so many buyers at once this year, and what your two real options are once the notice arrives.

A fixed rate locks your rate. It never locked your payment.

Your principal and interest payment is genuinely fixed for the life of a 30-year fixed-rate loan; that part of the math never changes. But most buyers who put down less than 20%, and plenty who put down more, also have an escrow account, where the servicer collects roughly one-twelfth of your annual property tax bill and one-twelfth of your annual insurance premium with every mortgage payment, then pays those bills on your behalf when they come due. That escrow piece was always an estimate, not a locked number, built from whatever your tax assessment and insurance quote looked like at closing.

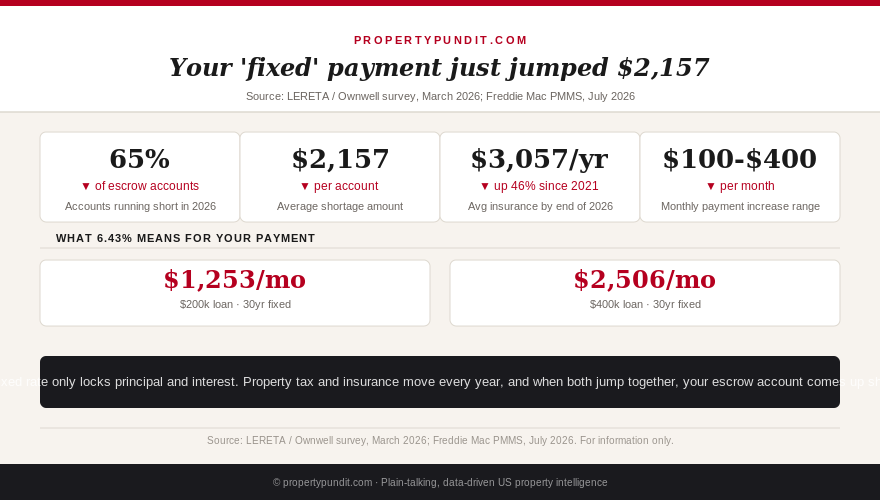

Property taxes and insurance premiums do not hold still. Homeowners insurance is projected to average $3,057 a year by the end of 2026, up 46% since 2021, and property taxes climbed to an average $4,427 per home in the most recent full-year data, up 3% year over year (ATTOM, insurance industry data, 2026). Every servicer runs an annual escrow analysis, typically once a year, comparing what actually got paid out for taxes and insurance against what it collected from you. So what this means for you: the interest rate on your Truth in Lending disclosure was never a promise about your total monthly payment, only about the loan portion of it, and treating the two as the same number is the exact assumption that makes this letter feel like a broken promise instead of routine math.

Why 65% of escrow accounts are short in 2026, not just yours

You are not being singled out. About 65% of escrow accounts are projected to run short this year because property tax and insurance costs have jumped together, in the same year, for a large share of homeowners (LERETA annual escrow survey, 2026). The average 2026 shortfall works out to $2,157, which, spread across 12 months the way most servicers offer, comes to about $179.75 in additional monthly payment (LERETA / Ownwell homeowner survey, March 2026). Three in five affected borrowers said the increase caught them by surprise, up from just over half a year earlier, which tells you this is a widening problem, not a one-time correction (Ownwell, March 2026).

The two drivers rarely move on their own schedule. A rising home value triggers a higher tax assessment; a separate renewal cycle brings a higher insurance quote, often 4% to 10% higher depending on your state and claims history. When both land in the same escrow analysis, a servicer that estimated your account conservatively a year ago is suddenly $150 or $300 a month short, and the shortfall plus the new higher ongoing collection amount both show up on the same notice. If your county has recently reassessed property values, the property tax appeal process is worth running before you assume the new number is final, since 30% to 60% of homes are over-assessed and a successful appeal lowers next year's bill and this year's escrow projection together. So what this means for you: if your notice bundles a tax jump and an insurance jump in the same year, do not treat it as two separate one-off problems. Check whether either number can actually be challenged before you accept the new payment as permanent.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The worked example: a $270,000 Atlanta purchase, one year later

Picture a buyer who closed on a $270,000 home in Atlanta at $78,000 income with an FHA loan and 3.5% down, the same profile behind a recent gift-funds down payment. At closing, the servicer estimated $2,400 a year in property tax ($200 a month) and $1,800 a year in insurance ($150 a month), for a combined escrow portion of $350 a month. A year later, the county reassessed the home after a strong local market, pushing the tax bill to $2,900 a year ($242 a month), and the insurance renewal came in at $2,300 a year ($192 a month) after a statewide rate filing. The new ongoing escrow portion is $434 a month, an $84 increase before the shortage repayment is even added.

Because the account paid out more than it collected for most of the past year, the servicer also posts a shortage of roughly $1,000, which, spread over 12 months, adds another $83 a month. Total payment increase: about $167 a month, squarely inside the $100 to $400 range showing up in escrow notices nationwide this year. On $78,000 income, that is real money, the difference between comfortable and tight in a monthly budget that likely has little slack built in from a first-time purchase. So what this means for you: run your own numbers the moment the notice arrives rather than after the new payment auto-drafts, because the lump-sum option only helps if you catch it before the 12-month spread has already started.

Your two options once the notice arrives, and which one actually saves money

Every servicer that posts a shortage is required to offer a repayment choice: pay the full shortage in one lump sum, or let it spread across the next 12 monthly payments along with the new, higher ongoing escrow amount. Paying the lump sum, in the Atlanta example roughly $1,000, immediately drops the added monthly cost from $167 to $84, the new ongoing escrow increase only. If you have that amount sitting in a low-yield savings account and your mortgage rate is meaningfully higher than what that cash is earning, paying it off in full is close to a guaranteed return equal to your mortgage rate on that portion of the balance. Spreading it over 12 months makes more sense if paying the lump sum would leave your emergency fund thinner than you are comfortable with, since a maintenance emergency layered on top of a drained reserve is a worse outcome than an extra $83 a month for a year.

Either way, read the actual escrow analysis statement line by line rather than skimming to the new payment total. Servicers occasionally misapply an insurance premium to the wrong policy year or use a stale tax bill instead of the current assessment, and catching that early is the difference between a phone call and a full year of overpaying. If mortgage insurance is also part of your monthly total, it is worth checking separately whether you have crossed the 80% loan-to-value threshold where PMI can be cancelled outright, since removing PMI in the same year an escrow shortage lands can offset some or all of the new increase. The math points toward treating the escrow notice as a full financial review moment, not a bill to pay and forget, since the same reassessment that triggered your shortage is also the trigger for challenging next year's tax bill before it happens again.

Most people who get a shortage notice do one of two things: pay it and move on without reading it closely, or panic and assume the loan itself is somehow broken. Neither is the right move. The closing costs breakdown is a useful reference if you want to see how your original escrow estimate was built in the first place, since understanding the starting assumption makes it much easier to spot exactly which line item moved and by how much. A fixed-rate mortgage did exactly what it promised: your rate never moved. Your payment was never the thing that was fixed, and the sooner that distinction is clear, the less each annual escrow letter will feel like a crisis instead of routine account maintenance.