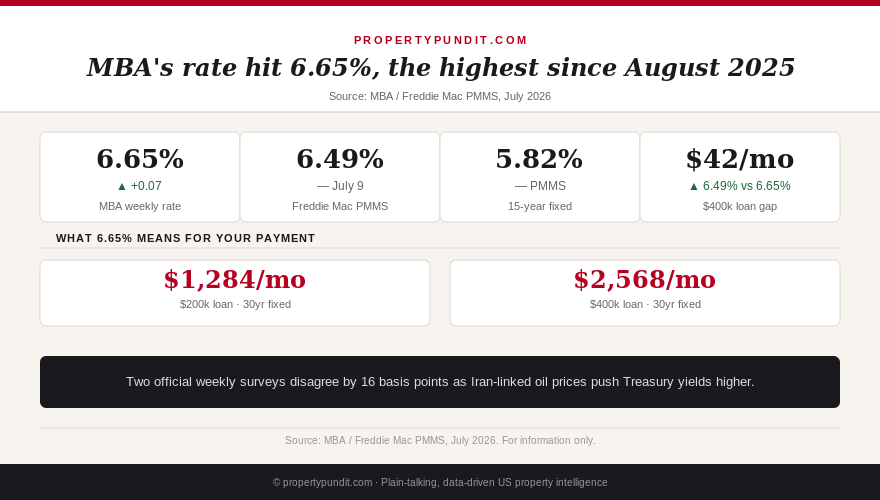

You've been checking the rate roughly the way people check a scoreboard, not because it changes your plan today, but because at some point the number is supposed to hit a level that makes refinancing obviously worth it. This week it moved, just not in the direction that number needed to go. The Mortgage Bankers Association's weekly survey put the average contract rate on a 30-year fixed conforming loan at 6.65% for the week ending July 10, 2026, the highest reading since August 2025 (MBA, July 15, 2026). That's the highest mortgage rates have been in nearly a year. Freddie Mac's benchmark survey, meanwhile, still shows 6.49% for the week ending July 9, with today's reading due at noon ET and not yet published as of this writing. Two credible weekly surveys, describing what should be the same market, sixteen basis points apart. If you're deciding whether this is finally your refinance window, that gap is worth understanding before you call your lender.

What the two surveys actually say

Freddie Mac's Primary Mortgage Market Survey, the official weekly benchmark most of the industry quotes, put the 30-year fixed rate at 6.49% for the week ending July 9, 2026, up from 6.43% the week before. The 15-year fixed rate came in at 5.82% (Freddie Mac PMMS, July 9, 2026). That reading holds until today's noon ET release. Separately, the Mortgage Bankers Association's Weekly Mortgage Applications Survey, covering the week ending July 10, 2026, showed the average contract rate for 30-year fixed conforming loans rising to 6.65% from 6.58% the prior week, the highest level since August 2025 (MBA, July 15, 2026). Purchase applications fell 7% on a seasonally adjusted basis that week, while refinance applications actually rose 4%, with FHA and VA refinance applications up 9% and 10% respectively. Two legitimate weekly averages of real lender activity are telling you two different things right now, and the number that decides your actual quote is neither one of them. It's the rate your own lender locks for you today.

Why two official surveys can disagree by 16 basis points

Neither survey is wrong. They sample different lender pools over different windows. PMMS draws from rate locks submitted through Freddie Mac's own Loan Product Advisor system, averaged Thursday through Wednesday. The MBA survey pulls from a much broader panel, roughly 75% of the retail mortgage application market, covering banks, thrifts, and mortgage bankers, and its survey week runs through Friday rather than Wednesday. In a week when Treasury yields kept climbing on renewed Iran-related oil price pressure, that extra day or two gave the MBA's panel more time to catch rates moving higher before the survey closed. Neither source is more "real" than the other; they're measuring overlapping but distinct slices of the same market at slightly different moments. Assuming last Thursday's PMMS headline is the rate a lender will quote you today could leave you underestimating your actual quote by close to a quarter point, which is worth confirming with a live number rather than a printed average.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What the gap actually costs you

On a $400,000 loan, a rate of 6.49% works out to a monthly principal-and-interest payment of $2,525.64. At 6.65%, that same loan's payment climbs to $2,567.86, a difference of $42.22 a month. Stretched over a 30-year term, that's roughly $15,200 in additional interest, all from a gap between two numbers that both call themselves "this week's mortgage rate." On a $300,000 loan, the same 16-basis-point spread costs $31.66 a month; on a $200,000 loan, it's $21.11. None of these gaps are large enough to change whether you can afford a house. They're large enough that assuming the lower of two available headline rates, without confirming which one your lender is actually quoting, can leave real money on the table over the life of a loan.

Why this gap matters more for your refi than your purchase

Say you're carrying a $350,000 balance at 7.25%, a rate that was common for buyers who closed in 2023 or 2024. Refinancing to 6.49% drops your payment from $2,387.62 to $2,209.94, a savings of $177.68 a month. Refinancing to 6.65% instead drops it to $2,246.88, a savings of $140.74 a month, a $37 gap in your monthly savings depending on which rate you actually land. That gap compounds when you run the break-even math against typical refinance closing costs of roughly 2% of the loan amount, about $7,000 on this balance. At the larger $177.68 monthly savings, you break even in about 39 months. At the smaller $140.74 savings, it takes closer to 50 months, nearly a year longer before the refinance pays for itself. If you're the kind of homeowner running this math on a spreadsheet before you commit, which of these two rates you plug in matters almost as much as the decision to refinance at all. Review our full refi break-even framework and the five refi triggers we track before you run your own numbers.

What's actually driving the rate higher

The renewed collapse of the Iran ceasefire pushed oil above $85 a barrel this week, and Treasury yields, which mortgage rates track more closely than the Fed funds rate, rose in response. June's Consumer Price Index actually cooled to a 3.5% annual pace from 4.2% in May, a reading that would normally argue for lower rates. The oil-driven geopolitical pressure offset that improvement this week instead. This is the same kind of driver that pushed PMMS from 6.43% to 6.49% between July 2 and July 9: a war-related shock to energy prices and bond yields, not a new domestic economic data release. Rates moved on geopolitics again this week, and geopolitical spikes tend to be choppier and harder to predict than a Fed-driven or CPI-driven move. Don't expect this week's headline number to hold if oil keeps climbing; base your lock-or-float decision on your own break-even math, not on a single week's print.

What this means for you this week

If your existing rate sits north of 7%, this week's environment, even using the higher 6.65% MBA reading, still supports a real, worthwhile refinance. Run the math on your specific balance rather than trusting either headline number on its own. If your rate is already at or below 6.5%, this week's rates don't help you, and waiting for a clearer signal makes more sense than acting on a single volatile week. Either way, your credit score still moves your individual quote more than the gap between these two national averages, so confirm where you stand before you call. The math above points toward getting an actual locked quote from a loan officer today rather than anchoring a decision to whichever survey happened to cross your feed, since a week where two official rate sources disagree by 16 basis points is exactly the week guessing gets expensive.

Most homeowners who run this math end up finding that a locked, lender-specific number is worth more than another week of watching two competing averages argue with each other. Treat 6.49% and 6.65% as the realistic band for this week, not as competing answers to the same question, and let your own loan officer's quote settle which one applies to you.