You're three pages into your closing disclosure, and everything makes sense until you hit a line called "title insurance" for $1,850. Nobody explained this one. Your loan officer mentioned it once in passing weeks ago, and now it's sitting there next to your down payment and your first month's escrow like it's supposed to be obvious. At $112,000 income, in a market where every extra thousand dollars at the closing table matters, you deserve to know exactly what you're paying for before you sign, not after.

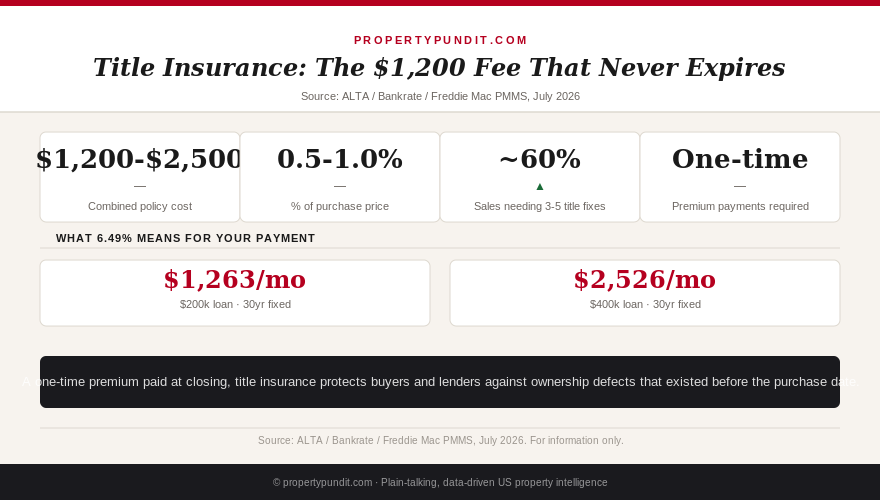

Here's the short version: title insurance is the one closing cost that protects you from a problem you can't see, buried in paperwork you'll never read, from owners you've never met. Nearly 60% of real estate transactions require clearing three to five separate title issues before they can even close, according to a March 2026 study by the American Land Title Association surveying 449 title professionals across 47 states (ALTA, 2026). That's not a rare edge case. That's most sales.

What title insurance actually protects you from

Every home has a paper trail of ownership going back decades, sometimes over a century, and that trail can have gaps: a forged signature on a deed from 1987, an heir nobody notified when a previous owner passed away, a contractor's lien that was never officially released, a clerical error when a deed was recorded at the county office. Title insurance protects you against defects that existed before your purchase date, even ones nobody, including the title company, knew about at the time. If one of those old problems surfaces after you own the home, threatening your claim to the property or your equity in it, the policy pays for the legal defense and covers your financial loss up to the policy amount.

This is fundamentally different from every other insurance policy tied to your home. Homeowners insurance protects against future events, fire, wind, theft. Title insurance protects against the past. That distinction is the whole reason it works as a one-time premium instead of a recurring bill: the risk is fixed at the moment of the title search, not ongoing. For a buyer stretching every dollar to hit a down payment target, understanding that difference means you stop mentally lumping this in with PMI or homeowners insurance as "just another monthly thing." It isn't one.

Lender's policy vs. owner's policy: the one you can actually skip

There are two separate policies, and conflating them is where most buyers get confused. The lender's policy protects the bank's financial interest in the loan, and it's required if you're financing the purchase; your loan will not close without it. It shrinks in value as you pay down the mortgage and disappears when the loan is paid off or refinanced. The owner's policy protects you, covering the full purchase price for as long as you own the home, and it's optional in most states.

Skipping the owner's policy is legal almost everywhere, and it will shave a few hundred dollars off your closing costs. It also means that if a title defect surfaces in year six, after you've built real equity through payments and appreciation, you have zero insurance protection on that equity, only the lender has coverage, and only for their remaining loan balance. Most title companies offer a simultaneous-issue rate when you buy both policies together at the same closing, which discounts the lender's policy substantially since the underlying title search work overlaps. Ask for that rate by name. Not every title company volunteers it.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why the cost swings from $1,200 to $2,500

Title insurance runs roughly 0.5% to 1.0% of your purchase price for combined lender's and owner's coverage, which is a wide enough range to be genuinely confusing when you're comparing loan estimates from different lenders. On a $320,000 home, a realistic first-time-buyer purchase price at $112,000 income, that puts combined title insurance somewhere between $1,600 and $3,200 before any simultaneous-issue discount. The swing comes down to your state. Some states, including Texas, New Mexico, and Florida, regulate title insurance rates directly, meaning every company charges the same published rate and your only lever is shopping the rest of the closing package. Other states let title companies compete on price, which means calling two or three companies for quotes can genuinely save you money, the same way shopping other closing costs can.

Unlike your PMI payment, which recalculates and eventually cancels as your loan-to-value improves, title insurance is priced once, paid once, and done. That one-time structure is exactly why it feels unfamiliar. You're used to negotiating rates that repeat every month, not a single number that has to be right the first time because there's no second chance to renegotiate it later.

The claim nobody talks about

Title claims are not hypothetical. The ALTA study found that mortgage payoffs need to be resolved in more than 90% of transactions and HOA dues or transfer fees show up in nearly 57%, meaning the title search is doing real, load-bearing work on almost every closing, not just protecting against rare horror stories. Most of those issues get caught and cleared before you ever sign anything, which is exactly the point: the title company's job is to find the problem before it becomes your problem. The insurance exists for the fraction of defects that slip through, an heir who shows up two years later, a lien that was recorded against the wrong parcel number and never properly indexed, a divorce settlement from decades ago that never actually transferred full ownership.

Without an owner's policy, a legitimate claim against your title means you're personally on the hook for legal fees and potentially your entire equity stake, with no insurer standing behind you. With one, the title company defends the claim and covers your loss up to the policy amount. For a buyer already carrying a tight credit profile and a thin cash cushion after closing, that's the scenario the owner's policy exists to prevent, not a rare catastrophe but the ordinary, unglamorous risk of buying something with a paper history longer than your own life.

Should you skip the owner's policy to save money?

If your closing costs are already stretched to the limit and every few hundred dollars matters, it's tempting to decline the owner's policy since it's optional and the lender's policy alone technically gets you to the closing table. Frankly, if you're a first-time buyer putting down 3% to 5% and financing nearly the entire purchase price, your equity position is small enough in year one that the exposure feels low. That changes fast. Two years of payments plus even modest appreciation can put $30,000 to $50,000 of your own money at risk with zero insurance covering it, for the cost of a few hundred dollars you'd have paid once, at closing, and never thought about again.

The math points toward buying the owner's policy in nearly every case, using the simultaneous-issue discount to keep the incremental cost as low as possible. Most people who run these numbers end up treating it the same way they treat homeowners insurance: not because they expect to need it, but because the one time they do, the alternative is catastrophic and entirely avoidable for a one-time fee smaller than a single month's mortgage payment.