You have probably noticed the contradiction even if you haven't put a number on it: everyone keeps saying the economy is slowing down, yet your mortgage rate quote this week is the same, or worse, than it was a month ago. That gap between what the economy is doing and what your rate is doing isn't a mistake, and it's not going to resolve itself the way most rate-watchers assume it will. Understanding why matters for anyone deciding whether to lock a rate now, wait for a refinance window, or time a purchase around a Fed move that keeps not happening.

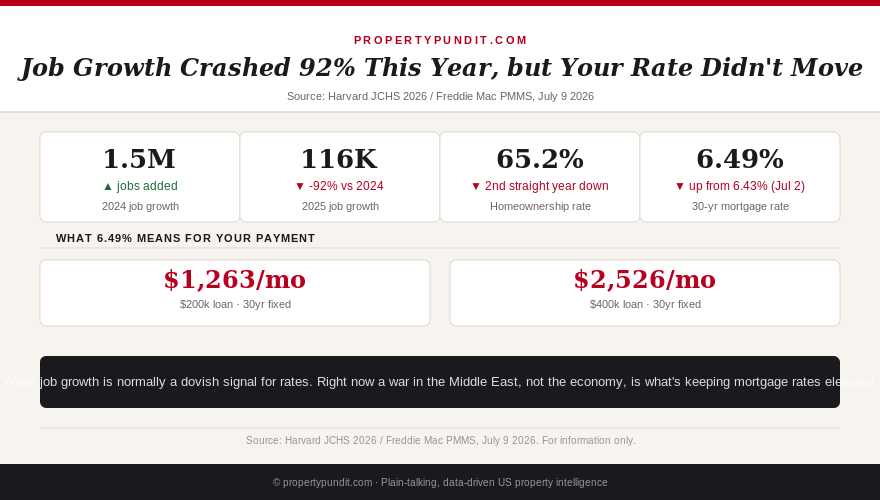

Harvard's Joint Center for Housing Studies released its State of the Nation's Housing 2026 report this month, and the labor market number buried inside it's the one worth sitting with: annual employment growth collapsed from 1.5 million jobs added in 2024 to just 116,000 in 2025, a decline of roughly 92%. Consumer confidence dropped more than 20 percentage points over the same stretch, reaching an all-time low in April 2026. This isn't a mild cooling. It is one of the sharpest labor market slowdowns in the report's multi-decade history, and it's happening at the same time home prices are setting records.

The homeownership rate absorbed the impact directly. It fell for a second consecutive year to 65.2%, with the steepest decline concentrated among adults under 35, whose ownership rate dropped to 37% from 39% in 2022. Annual growth in the number of homeowner households was cut roughly in half. Vacancy rates tell the same story from a different angle: the homeowner vacancy rate rose to 1.1% and the renter vacancy rate to 7.3% in the first quarter of 2026, both signs of softening demand relative to supply, even as sales of existing homes sit near three-decade lows.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Why a weakening economy hasn't lowered your rate

Here is the mechanism most homeowners get backward: mortgage rates don't track the Fed funds rate, and they don't track job growth directly either. They track the 10-year Treasury yield, which reflects inflation expectations, deficit concerns, and geopolitical risk as much as it reflects the labor market. Right now, the dominant force pushing Treasury yields higher isn't the economy at all. It is the renewed US-Iran conflict that escalated the week of July 6 through 9, 2026, which pushed oil prices and inflation expectations up and took the 30-year fixed from 6.43% on July 2 to 6.49% on Freddie Mac's official July 9 survey. Daily lender trackers moved even further, with Bankrate showing 6.58% and other trackers running as high as 6.6% to 6.66% by July 10 and 11.

That is the contradiction in one sentence: the labor market is sending a classic signal for lower rates, and a war is sending a stronger signal for higher ones, and right now the war is winning. The June 17, 2026 FOMC meeting, Kevin Warsh's first as Fed Chair, removed the committee's easing bias entirely and raised its median year-end projection for the Fed funds rate. CME FedWatch data has priced essentially no probability of a rate cut before 2027. A soft jobs report alone hasn't been enough to move that needle, and it's unlikely to be enough on its own until the deterioration shows up unmistakably in the unemployment rate, not just the pace of hiring.

So what does this mean for you: don't wait for this jobs data to translate into a near-term rate drop. The mechanism that would normally connect weak employment to lower mortgage rates is currently overridden by a geopolitical shock, and that can persist for months, not weeks.

What weak demand actually buys buyers right now

The flip side of a slowing economy is softer competition, and that part of the story is showing up in the data too. Payments on a median-priced home reached $3,100 a month in the fourth quarter of 2025, requiring an income of more than $120,000 to meet standard affordability guidelines, with both median new and existing home prices above $400,000. That is a genuinely difficult affordability bar. But rising vacancy rates and slower household formation are already producing real negotiating room in many markets: seller concessions hit a record 46.2% of spring 2026 sales nationally, and roughly 36% of active listings carried a price cut as of June 2026. Our guide to seller concessions and closing costs covers exactly what to ask for and when.

For a buyer watching rates and waiting for a better entry point, the practical read is that the "better entry point" is showing up on the price and concession side of the transaction well before it shows up on the rate side. A buyer who negotiates $15,000 to $25,000 off a list price today captures a real, immediate saving. A buyer betting on a rate drop that is currently being blocked by a geopolitical shock is betting on a variable nobody, including the Fed, currently controls.

What this means for your refinance and lock decisions

If your existing mortgage sits well below 6%, this data doesn't change your calculus much: refinancing into a 6.49% rate to chase softer demand elsewhere makes little sense, and the standard advice to only refinance when the new rate beats your existing rate by at least 0.75 to 1 percentage point still holds, a threshold we break down fully in our 5 mortgage refi triggers framework. If you are house-hunting and deciding whether to lock now or float, our rate lock versus float decision guide walks through the tradeoffs; the deteriorating labor market is a signal worth tracking over the next two to three FOMC cycles, not this week's rate sheet. A genuine, sustained rise in the unemployment rate, not just slower hiring, is historically what forces the Fed's hand, and that hasn't happened yet. Buyers who are also weighing their credit profile before locking should see our credit score and mortgage rate breakdown for what actually moves the needle on pricing.

The math points toward treating today's rate environment and today's price environment as two separate negotiations. Rates are being held up by a war, not by the economy, and they could stay elevated for exactly as long as that conflict does. Prices and concessions are already responding to the weaker economy Harvard's report describes. Most buyers who are waiting for both to move in their favor at once are going to be waiting considerably longer than buyers who negotiate hard on price today and watch the rate side separately.