You've a dozen browser tabs open, a mortgage calculator, three real estate agent recommendations, and a growing list of questions nobody quite answers in one place. Most guides give you either a wall of legal disclaimers or a vague "it depends." Here are seven questions real buyers are actually typing into Google right now, answered directly, with a specific recommendation attached to each one.

How much house can I afford on $112,000 a year?

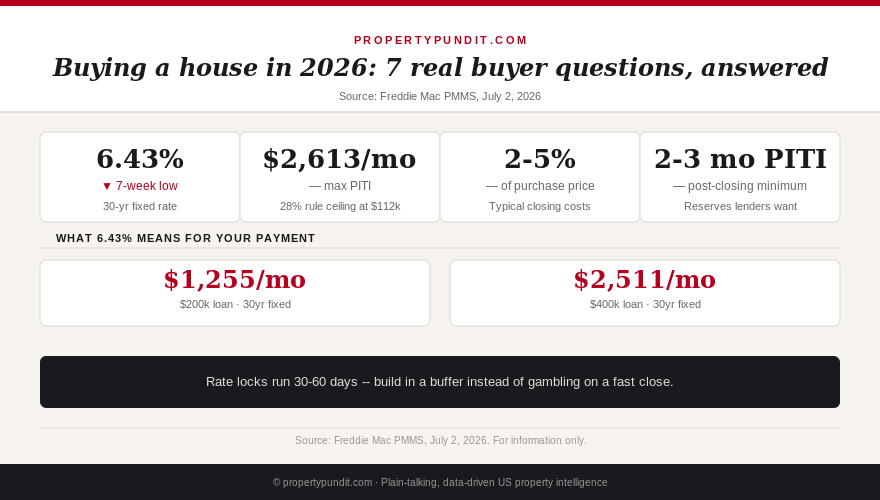

Using the 28% housing rule, $112,000 a year works out to $9,333 a month gross, which caps a comfortable total housing payment at roughly $2,613. At 6.43% with 20% down, that supports a purchase price somewhere in the $390,000 to $410,000 range, and the exact number moves with local property tax and insurance costs, which vary more than most buyers expect from one county to the next. Run the number for the actual home you're considering, not a national average calculator. If the PITI comes in above $2,600, look at a less expensive area or a larger down payment rather than stretching into a higher debt-to-income approval just because a lender says you qualify.

Should I buy now or wait for rates to drop?

The 30-year fixed sits at 6.43% as of Freddie Mac's July 2, 2026 survey, a seven-week low, and futures pricing shows no expected rate cut before 2027 at the earliest. Waiting has a real cost that is easy to underweight: home prices still rise 1% to 4% a year even in a market that favors buyers, and rent keeps compounding the entire time you sit on the sidelines. If you find a home that fits your budget at today's rate, the math points toward buying it and refinancing later if rates do eventually fall, rather than waiting on a cut that may not show up for 18 months or longer.

What's the difference between pre-qualified and pre-approved?

Pre-qualification is an unverified estimate based on numbers you told a lender over the phone or in an app, income, debts, and a self-reported credit range, nothing checked. Pre-approval means a lender has actually pulled your credit and verified your income and asset documents, and it carries real weight with sellers and listing agents, especially when the number on your pre-approval letter isn't automatically your real budget. Get fully pre-approved, not just pre-qualified, before you start touring homes seriously. In a competitive offer, a pre-qualification letter is frequently not taken seriously at all.

How much are closing costs, really?

Closing costs typically run 2% to 5% of the purchase price, which is $6,000 to $15,000 on a $300,000 home, and cover lender fees, title insurance, the appraisal, recording fees, and prepaid escrow for taxes and insurance. The full closing cost breakdown walks through every line item with real dollar figures. Ask your lender for a Loan Estimate before you shop so you know your actual number rather than a rule of thumb, and with roughly a third of listings nationally carrying price cuts right now, ask the seller to cover some of it instead of assuming you've to pay every dollar yourself.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Can the seller back out after accepting my offer?

Generally no. Once both sides sign, the contract binds the seller as much as it binds you, unless a specific contingency in the contract allows an exit. A seller who backs out without a valid contingency can be sued for specific performance or damages, though in practice most buyers instead negotiate the return of their earnest money and move on rather than fight over one house in court. Work with an agent or attorney who can respond fast if a seller tries to walk, and don't waive your own contingencies early just because you're worried about the seller's cold feet. Those contingencies protect you too.

What happens if my rate lock expires before closing?

Most rate locks run 30 to 60 days. If your closing slips past that window, which happens more often than buyers expect, you typically either pay an extension fee, often 0.125% to 0.25% of the loan amount per week, or re-lock at whatever the market rate happens to be that day, for better or worse. The full lock-or-float decision framework covers how to time this by closing date. Build a buffer into your lock period from the start; many experienced buyers now lock for 45 to 60 days even when a 30-day close looks realistic, because a small extension fee is far cheaper than losing your rate outright.

How much cash do I need saved beyond the down payment?

Beyond the down payment itself, budget for closing costs of 2% to 5%, plus the two to three months of mortgage payments in reserve that most lenders want to see sitting in your account after closing, plus a buffer for the immediate maintenance and utility setup costs that catch nearly every new buyer off guard in month one. The down payment myth covers why you likely need far less down than you think, which frees up more of your savings for this reserve. Don't drain your account to maximize your down payment. Keep at least two months of PITI in reserve after closing, because lenders check for exactly that, and life keeps happening after you get the keys.

The pattern behind all seven answers

Look back over these seven questions and a pattern shows up: almost every wrong assumption comes from treating a soft guideline as a hard rule, or a hard rule as a soft guideline, in exactly the wrong direction. Buyers assume pre-qualification carries the weight of pre-approval. They assume a rate lock is permanent once it is set. They assume a signed contract protects the seller as loosely as gossip suggests it does. In each case, the real rule is more specific, and more forgiving of a prepared buyer, than the rumor.

The math points toward treating every one of these questions as a five-minute phone call to your lender or agent before you act, not a guess you make on your own. At $112,000 income and 6.43% rates, the numbers already work in your favor if you run them correctly. Most of the buyers who end up frustrated later aren't the ones who asked too many questions early. They are the ones who assumed an answer instead of checking it.