You have watched Seattle rents climb toward $3,700 a month for a single-family house and wondered whether the math finally works for a landlord willing to pay $865,000 for the privilege. It doesn't, and the gap isn't close. Across Washington in July 2026, at a 6.43% mortgage rate and a 25% down payment, exactly one market gets near breakeven, and only at the cheap end of it.

The statewide number hides three very different markets

Washington's statewide median sale price is $612,823, down 0.88% year over year (Redfin, May 2026). That figure is dragged upward by Seattle and its Eastside suburbs and dragged downward by inland cities like Spokane. Treating the state as one market is how out-of-state investors end up underwriting Spokane cash flow with Seattle assumptions, or the reverse.

Seattle's median home value sits at $865,000, roughly flat year over year (Zillow ZHVI, June 2026). Tacoma, an hour south, runs $500,000, up 0.9% (Redfin, three months ending May 2026). Spokane, on the state's dry side near the Idaho border, sits at $355,000, down 1.7% (Redfin, three months ending April 2026). The price spread between Seattle and Spokane is $510,000 for what is nominally the same state market. For a Washington investor, the state median is close to useless. The city you pick determines whether you clear breakeven at all.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Seattle: the priciest math in the state

A Seattle single-family rental at the $865,000 median, financed with 25% down at 6.43%, carries a monthly principal and interest payment of $4,071. Add King County's roughly 0.84% effective property tax ($606/month), landlord insurance (about $105/month), a one-month vacancy allowance ($312/month), and an 8% management fee ($300/month), and total monthly costs run $5,394 against a typical 3-bedroom single-family rent of $3,750 (RentCafe / Zumper, June 2026). Net cash flow: roughly negative $1,644 a month. The debt service coverage ratio, gross rent divided by mortgage plus tax plus insurance, comes out to 0.78, well under the 1.0 minimum most DSCR lenders require. Our DSCR loan investor guide covers how that threshold is calculated and why lenders won't budge on it. If your Washington strategy leans on Seattle cash flow, the numbers say to rebuild the strategy around appreciation instead.

Tacoma: cheaper, but still bleeding

Tacoma looks like the value play at $500,000, but the arithmetic still runs negative. Principal and interest on 75% financing at 6.43% is $2,353/month. Pierce County's effective property tax rate of 1.05% adds $438/month, the highest rate of the three cities covered here. With insurance, vacancy, and management factored in, total monthly cost is $3,304 against a typical single-family rent of $2,500 (Zillow Rental Manager, May 2026). Net cash flow: roughly negative $804 a month, with a DSCR of 0.86. Tacoma is closer to viable than Seattle, but a landlord still needs six figures of outside income to carry the shortfall, or a materially larger down payment than 25%. So what for you: if Tacoma is your entry point because it's "cheaper than Seattle," run the real DSCR before you assume cheaper means it cash flows.

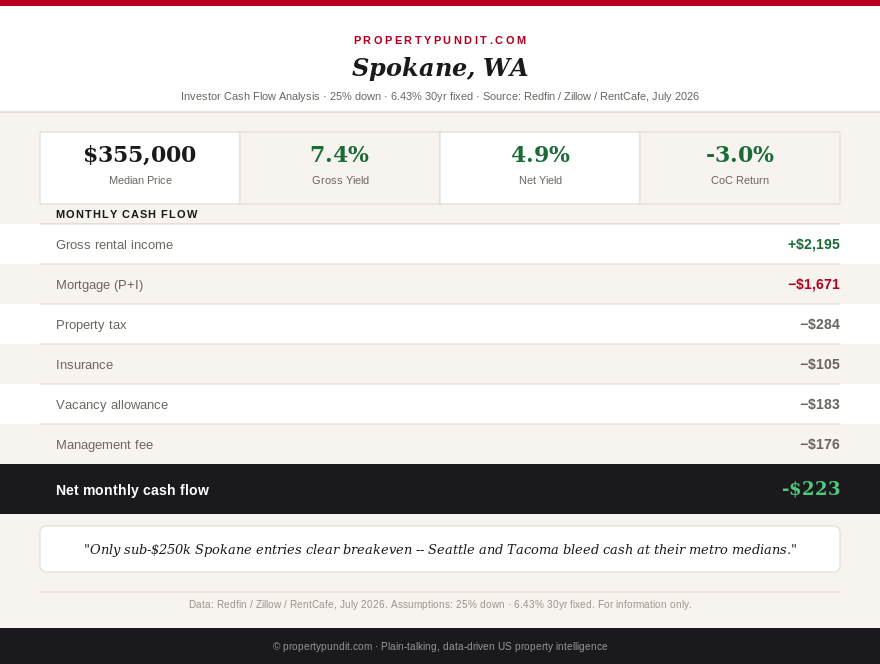

Spokane: the only market that gets close

Spokane is where the state's math finally starts to work. At the $355,000 citywide median, principal and interest at 6.43% and 25% down is $1,671/month. Spokane County's 0.96% effective tax rate adds $284/month. Rent for a typical single-family home runs $2,195/month (RentCafe, June 2026). After insurance, vacancy, and management, net cash flow lands at roughly negative $223 a month, with a DSCR of 1.07, technically above the 1.0 lending threshold even though real cash flow after operating costs is still negative. That gap between "passes DSCR" and "actually cash flows" is exactly the trap our property management fee breakdown warns about: a loan can qualify on paper while the property still loses money every month.

Drop to Spokane's entry-level tier, homes around $250,000 renting near $1,800/month, and the picture flips. Principal and interest falls to $1,177/month, property tax to $200/month, and total monthly cost to roughly $1,776. Against $1,800 in rent, that produces a DSCR of 1.21 and net cash flow of about positive $24 a month once vacancy and management are subtracted. It's a thin margin, not a windfall, but it's the only positive number in this entire article. If you're underwriting a Washington rental for cash flow rather than appreciation, sub-$250,000 Spokane is the only entry point that currently clears it.

The rent cap most investors haven't modeled yet

House Bill 1217 caps most 2026 lease renewal increases at 7% plus inflation, or 10%, whichever is lower. The Washington Department of Commerce set the actual 2026 ceiling at 9.683%. That's a real constraint on the traditional landlord playbook of pushing rent hard at renewal to offset a negative-cash-flow purchase. New construction is exempt from the cap for its first 12 years, and a landlord can still set market rent freely for a brand-new tenant, so unit turnover remains a lever, just a slower one than in states with no cap at all. For a Seattle or Tacoma buyer already underwater on day one, the rent cap removes the easiest route back to breakeven: raising rent faster than costs rise.

The one number working in an investor's favor

Washington has no state income tax on wages or rental income, which every spotlight in this series treats as a real, ongoing advantage. Less well known: Washington's state capital gains tax, which runs 7% on gains above $250,000 and 9.9% above $1 million, explicitly exempts real estate. A landlord who sells an appreciated Washington rental owes federal capital gains tax and federal depreciation recapture, covered in our SFR yield county map, but no state-level capital gains bill at all. That's a genuine point of separation from income-tax states that tax the full gain on exit, and it partially offsets the weak monthly cash flow documented above. So what for you: Washington rewards a buy-and-hold-to-sale strategy far more than a buy-and-rent-for-income strategy at today's prices.

What the data implies you should do

The math points toward treating Washington as two separate strategies, not one. If you want monthly cash flow today, Spokane's entry-level tier under roughly $250,000 is the only Washington market that supports it, and even there the margin is thin enough that a single vacant month erases a year of profit. If you're underwriting for appreciation and tax-free exit instead, Seattle and the Eastside remain defensible on a 7-to-10-year hold, backed by no state income tax and no state capital gains tax on the eventual sale. Most investors who run these numbers honestly end up picking one lane or the other rather than trying to force Seattle to cash flow like Spokane. Frankly, if your primary goal is monthly income, Washington in July 2026 is not the state to chase it in outside of Spokane's cheapest tier.