You have been tracking the 30-year fixed as it eased from 6.51% in May toward 6.43% this week, and you assumed that meant homebuying costs were quietly getting easier. They weren't, at least not for four weeks in June. The median U.S. monthly housing payment climbed to $2,647, its highest level in a year, then posted its first year-over-year increase in eight months. Rates falling didn't save buyers this time. Prices did the damage instead.

The number that reversed

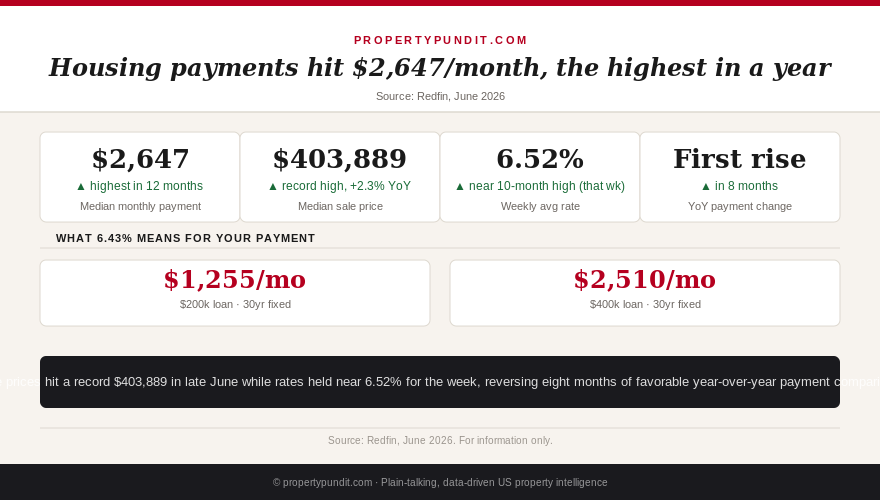

During the four weeks ending June 14, 2026, the median U.S. monthly housing payment reached $2,647, the highest level in a full year (Redfin, June 2026). Two weeks later, during the four weeks ending June 28, that payment posted its first year-over-year increase since October 2025, breaking an eight-month run of favorable comparisons that had made housing costs look like they were easing. They weren't easing anymore. So what for you: if you've been waiting for the "affordability is improving" narrative to keep playing out before you buy, this data point says that narrative just paused.

Why rate relief didn't show up in the payment

The median home sale price hit a record $403,889 during the same late-June window, up 2.3% year over year, while the average weekly mortgage rate held near 6.52%, close to its highest level in ten months for that specific week (Redfin, June 2026). Price growth simply outran the rate relief. A buyer financing the record median price at 6.52% pays more per month than a buyer financing a lower price at a higher rate from a year earlier, even though the headline rate story sounds like good news. Payment math is a function of price times rate, not rate alone, and this week is the clearest recent illustration of why that distinction matters. So what for you: stop tracking the rate in isolation. Track the payment on the specific price point you're actually shopping in.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What this means for your refi trigger point

The 30-year fixed has since eased to 6.43% (Freddie Mac PMMS, July 2, 2026), a seven-week low, and this rising-payment data doesn't change that number or your personal refinance math. It describes new buyers financing today's record prices, not existing borrowers with a fixed rate already locked in. Our refinance trigger framework still applies exactly as written: if you closed at 7.0% or higher, 6.43% clears most break-even calculations; if you closed under 6.75%, the math is closer and depends on how long you plan to stay. If your 2021-vintage ARM is due to reset this year, the payment jump described in our ARM reset payment math piece is the more relevant number for you than the national median payment figure in this article.

What to watch next

Three dates now matter more than this data point on its own. The next Freddie Mac PMMS reading lands July 9 and will confirm whether 6.43% holds or reverses. July 14 CPI is the next inflation print that could move the 10-year Treasury, and with it, mortgage rates, in either direction. July 30 FOMC is not expected to cut, per CME FedWatch pricing, so don't expect that meeting to move your rate regardless of what the payment data does between now and then. If you're within 30 days of closing, our rate lock versus float framework still recommends locking rather than gambling on a July surprise. So what for you: this week's record payment number is a reason to lock in your own terms with confidence, not a reason to wait for a better one that current data doesn't support.

What the data implies you should do

The math points toward treating "rates are falling" and "buying is getting cheaper" as two separate claims that can move in opposite directions, exactly as they did this June. If you're shopping at or near the national median, budget for a payment closer to $2,647 than to whatever a falling-rate headline implies, and confirm the actual price and rate on the specific home you're underwriting rather than extrapolating from the national number. Most buyers who run their own math instead of the headline end up locking a rate on a specific property this week rather than waiting for July 9 or July 14 to hand them a better deal that the current trend doesn't support.