You own two rental properties, one of them has appreciated nicely, and you're penciling out what happens if you sell it and redeploy the equity somewhere with better cash flow. You already know you'll owe capital gains tax on the profit. What most investors don't model correctly is that a separate, higher-rate tax applies to the depreciation you claimed every year you owned it, and it doesn't care what your capital gains bracket is.

What depreciation recapture actually is

Every year you own a rental, the IRS lets you deduct a portion of the building's value against your taxable income, typically over 27.5 years on a straight-line schedule. That deduction lowers your tax bill while you hold the property. When you sell, the IRS wants some of it back. The depreciation you claimed becomes "unrecaptured Section 1250 gain," and it's taxed at your ordinary income rate, capped at 25% federal, rather than the lower long-term capital gains rate (0%, 15%, or 20%) that applies to the rest of your profit. It's a separate calculation layered on top of the capital gains math, not a replacement for it.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

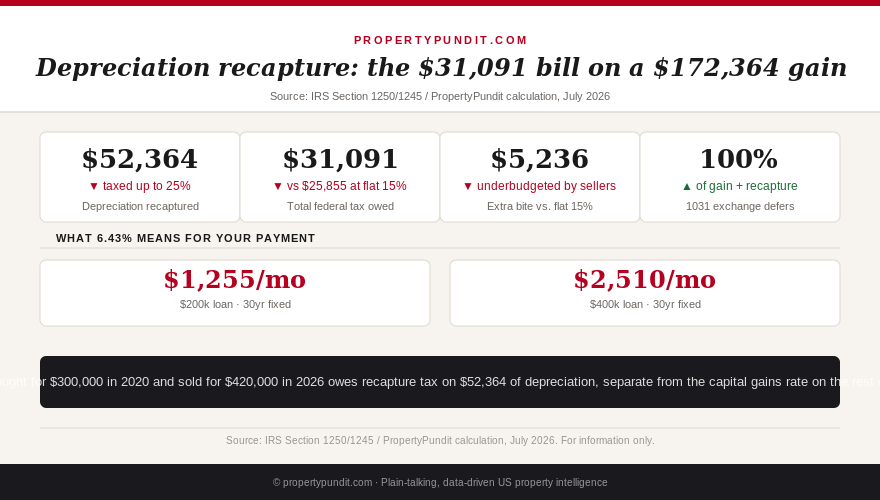

The worked example: a $300,000 rental sold for $420,000

Say you bought a single-family rental in 2020 for $300,000, with the building (excluding land) valued at $240,000. Straight-line depreciation over 27.5 years works out to $8,727 a year. Across six years of ownership, that's $52,364 in accumulated depreciation, all of it already deducted against your income in prior tax years.

You sell in 2026 for $420,000. Your adjusted basis is the original $300,000 minus the $52,364 already depreciated, or $247,636. Total gain: $420,000 minus $247,636, which is $172,364. Here's where the two-rate math kicks in. The $52,364 you depreciated is taxed as unrecaptured Section 1250 gain at up to 25%, which is $13,091. The remaining $120,000 of gain is taxed at the long-term capital gains rate, 15% for most investors in this income range, which is $18,000. Total federal tax on the sale: $31,091.

Compare that to what an investor assuming a flat 15% capital gains rate on the entire $172,364 gain would expect to owe: $25,855. The recapture provision adds $5,236 more than that assumption, an 18% effective tax rate on the total gain rather than a flat 15%. That gap is money most sellers don't budget for until the closing statement lands. So what for you: if you're penciling a sale to fund a down payment on the next property, use the 18% blended rate, not the headline capital gains rate, or you'll show up short at closing.

Why bonus depreciation can make the bill even bigger

The One Big Beautiful Bill Act reinstated 100% bonus depreciation for qualifying property placed in service after January 19, 2025, and many investors are pairing that with a cost segregation study to accelerate deductions on personal property and land improvements, appliances, carpeting, fencing, parking areas, rather than depreciating the whole building over 27.5 years. That strategy genuinely lowers your tax bill in the years you own the property. It also creates a second, worse category of recapture at sale.

The portion of accelerated depreciation attributable to real property still falls under Section 1250 and keeps the 25% cap described above. But the personal-property and land-improvement portion identified through cost segregation is Section 1245 property, and recapture on Section 1245 assets is taxed at your full ordinary income rate with no 25% ceiling. If your marginal rate is 32% or 35%, that piece of the bill is taxed at 32% or 35%, not 25%. An investor who did an aggressive cost segregation study to save $15,000 in tax during ownership can end up owing more than that back at sale, at a higher rate than the standard recapture math above. This doesn't mean cost segregation is a bad strategy. It means the tax you deferred during ownership is a bill with your name on it, and the interest-free loan from the IRS eventually comes due, often at a worse rate than you assumed.

The 1031 exchange is the only way to defer all of it

A properly structured 1031 exchange defers both the capital gains tax and the full depreciation recapture bill, Section 1250 and Section 1245 alike, by rolling your basis into a replacement property instead of cashing out. Our 1031 exchange guide covers the 45-day identification window and 180-day closing deadline in detail, both of which are absolute, not negotiable with the IRS. If the replacement property is financed with a DSCR loan rather than conventional financing, lenders will still run the same debt service coverage math covered in our DSCR loan investor guide, so exchanging into a market with better cash flow than the one you're leaving doesn't automatically clear underwriting. Run the DSCR on the replacement property before you commit to the exchange, not after.

What the data implies you should do

Before you list a rental with meaningful depreciation on the books, run the two-rate calculation above with your actual numbers, not a flat capital gains assumption, and check whether you used cost segregation, which shifts part of the bill into the uncapped Section 1245 category. Most investors who run these numbers honestly end up doing one of three things: selling anyway because the equity redeployment still wins after the higher tax bill, structuring a 1031 exchange to defer the whole amount into a better-performing property, or holding longer than planned because the after-tax proceeds do not justify the disruption. The math points toward treating depreciation recapture as a known, calculable cost of selling, not a surprise line item, the same way you would model a mortgage payoff or a real estate commission before you set a listing price.