You've watched your account statement for three years. You've cut the subscriptions. You've moved back to cheaper rent. And you still can't close the gap between what you have saved and what you need at the closing table. Then the thought arrives: the 401(k). It's your money. Why not use it?

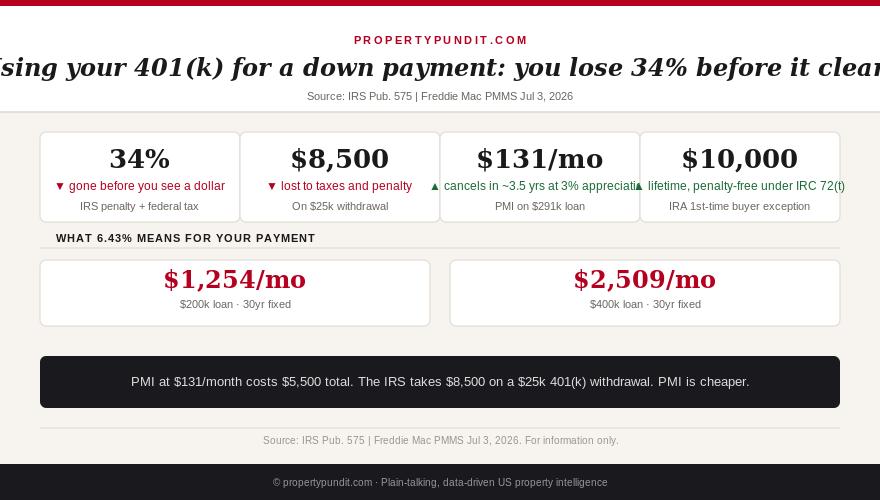

Here's what the IRS takes before that money hits your checking account. At a 24% marginal federal tax rate, you lose 34% of every dollar you pull out as a hardship withdrawal: 10% early-withdrawal penalty, plus 24% ordinary income tax on the full amount. On a $25,000 withdrawal, $8,500 goes directly to Washington. You receive $16,500. And the retirement compounding on the $25,000 you withdrew, at 7% annualized over 30 years, would have grown to roughly $190,000. You're not borrowing from yourself. You're permanently deleting $190,000 from your retirement portfolio to add $16,500 to a down payment.

The math rarely works out. But there are specific situations where it's the right call, and specific options within the 401(k) world that carry far lower costs than a hardship withdrawal. This article runs through every number.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

What the IRS takes before the money clears your account

There is no first-time homebuyer exception in the 401(k) rules. The IRS offers that break for IRAs (covered below), but 401(k) plans have no such carve-out. If you are under 59.5, every dollar you pull from a 401(k) as a hardship distribution triggers two separate charges.

First is the 10% early-withdrawal penalty, applied to the gross amount. Second is ordinary income tax, applied to the full gross amount at your marginal rate. If you earn $112,000 as a single filer in 2026, the extra $25,000 of 401(k) income pushes your taxable income to $137,000. Your marginal federal rate is 24%. The penalty alone is $2,500. The income tax is $6,000. Total cost: $8,500. That's 34% of the withdrawal before a single dollar touches your down payment.

The only scenario where the hardship withdrawal costs less is if you earn under $47,150 as a single filer, where the marginal rate drops to 12%. At 12%, the total hit is 22%: on a $25,000 withdrawal, you lose $5,500 and net $19,500. Still a steep entry price.

One more practical point: the IRS requires the plan administrator to withhold 20% automatically. That means if you request $25,000, you receive $20,000 in your account and get the remaining $5,000 back (or owe more) when you file your tax return the following April. The full $25,000 is still treated as taxable income, but your cash timing is off by thousands of dollars. If your down payment timing is precise, that four-month gap matters. Before you touch your 401(k), run your actual cost scenario with your tax filing status confirmed.

The 401(k) loan: lower upfront cost, two hidden traps

A 401(k) loan avoids the penalty entirely. The IRS allows you to borrow up to 50% of your vested balance, or $50,000, whichever is lower. Most plans charge an interest rate of prime plus 1%, currently around 8.5%. The interest you pay goes back into your own account, which is often cited as a benefit. Here's what that description leaves out.

You pay that interest with after-tax dollars. When you retire and withdraw the money, you pay income tax on it again. The interest is effectively taxed twice. On a $25,000 loan at 8.5% over five years, you pay roughly $5,600 in total interest. The double-tax cost on that interest, at a 24% rate, is an additional $1,344 in lifetime tax drag that a standard bank loan doesn't carry.

The second trap is the employment trigger. If you leave your job or are laid off before the loan is fully repaid, most plans require the full outstanding balance by the federal tax return due date for that year (typically April 15 of the following year, with an extension to October). If you can't repay it in time, the unpaid balance becomes a distribution: you owe the 10% penalty and income tax on whatever remains, at exactly the moment you're least prepared to pay it. In a volatile employment environment, taking a 401(k) loan tied to a job is a compounded risk most first-time buyers haven't modeled.

If you're confident in your job stability and can repay in five years, the loan is genuinely cheaper than a withdrawal. But confirm the repayment terms with your plan administrator before you sign. Some plans require repayment within 60 days of employment separation, not by the next tax deadline.

Two exceptions that cut the cost significantly

Two retirement account paths carry much lower costs than anything available inside a 401(k), and most first-time buyers have never heard of either one.

The first is the IRA first-time homebuyer exception under IRC Section 72(t)(2)(F). If you have a traditional IRA and have not owned a home in the past two years, you can withdraw up to $10,000 lifetime without the 10% penalty. You still owe ordinary income tax on the withdrawal, but eliminating the penalty drops the cost from 34% to 24% (at the same marginal rate). On a $10,000 IRA withdrawal, you lose $2,400 rather than $3,400. The remaining $7,600 is penalty-free down payment money. If your spouse also qualifies, you can each withdraw $10,000 for a combined $20,000 penalty-free between two IRA accounts.

The second is the Roth IRA contributions rule, which is more powerful. With a Roth IRA, your contributions (not your earnings) can be withdrawn at any time with zero tax and zero penalty, regardless of your age or reason. There's no homebuyer exception required because contributions were already taxed when you made them. If you've been contributing to a Roth for even three or four years, you may have $15,000 to $25,000 in contributed principal available at no cost. Pull the principal only, leave the earnings in the account, and the withdrawal is completely free. This is the single best retirement-account path to a down payment if you have a Roth with accumulated contributions. Check your plan statements for the "basis" or "contribution" figure before you assume you have nothing available.

The IRA penalty exception and the Roth contribution route both require you to have the accounts in the first place. If your retirement savings are entirely in a 401(k) and you have no IRA, you'll need to decide whether to roll funds over (which has a 60-day clock and tax considerations) or work with what you have. Consult a tax advisor before initiating any rollover timed to a home purchase.

Why the 401(k) math usually loses to just paying PMI

Here's the calculation most buyers skip. Suppose you're buying a $300,000 home at 3% down ($9,000). Your lender charges PMI at 0.54% annually on the loan balance (a typical rate for a 720-plus credit score buyer). On a $291,000 loan, that's $131/month. Under the Homeowners Protection Act, PMI cancels automatically when your loan-to-value ratio hits 80%. At 3% appreciation annually on a $300,000 home, you hit 80% LTV in roughly three and a half years. Total PMI paid: approximately $5,500.

Compare that to pulling $25,000 from a 401(k) to get to 10% down. The IRS cost is $8,500 in taxes and penalty. You paid $8,500 to avoid $5,500 in PMI. The 401(k) withdrawal cost $3,000 more than just paying the mortgage insurance and waiting for appreciation to cancel it. And you permanently removed $25,000 from a tax-advantaged retirement account that would have compounded for decades. This comparison holds unless PMI is significantly higher than 0.54%, your home is in a flat or declining appreciation market, or you're buying at a price point where PMI runs well above $200/month. In those cases, the time-to-80%-LTV calculation changes materially. Run the actual numbers for your loan size and credit score before assuming PMI is the worse outcome.

The math points toward this conclusion: for most first-time buyers earning $78,000 to $112,000, paying PMI and leaving the 401(k) intact is the better financial decision in the long run. The exception is when the buyer has an unusual combination of high PMI, flat appreciation, and a Roth IRA with substantial contributions available at zero cost. In that case, using the Roth contributions first and supplementing with the PMI savings is the cleanest path.

What to do instead

Before you touch any retirement account, check three alternatives that carry no IRS cost.

Down payment assistance programs: 2,679 programs operate nationwide with an average benefit of $17,900 (per the down payment assistance analysis published June 1, 2026). Many are forgivable grants that never require repayment if you stay in the home for three to five years. Start at your state housing finance agency's website. Georgia Dream, for example, covers the full FHA minimum down payment on a $260,000 home. Most programs are income-qualified, and at $112,000 many metro programs fall outside the limit, but rural and workforce programs often reach higher incomes.

Gift funds: Conventional loans allow 100% of the down payment to be gifted by a family member, documented with a gift letter. FHA loans have the same allowance. If a parent or relative can contribute, this is the zero-cost path.

Seller concessions: With 46.2% of spring 2026 home sales including seller concessions (Redfin, May 2026), asking the seller to cover closing costs instead of negotiating a price reduction frees up your own cash for the down payment. A $10,000 concession on closing costs is $10,000 less you need to bring to the table. See the seller concession guide published June 17 for the maximum limits by loan type.

If none of these alternatives are available and the 401(k) is your only option, use the loan (not the withdrawal) if your job is stable, or use Roth contributions if you have them. Avoid the hardship withdrawal unless you've confirmed, with actual tax calculations, that the IRS cost is lower than three or more years of PMI in your specific situation.

The 30-year fixed sits at 6.43% today (Freddie Mac PMMS, July 3, 2026). For most first-time buyers, the better move is to get into the home at 3% down with PMI, let appreciation and payments cancel the insurance, and keep the 401(k) compounding untouched. The math on that path beats the 34% withdrawal cost in every scenario where appreciation runs at 3% or better and PMI is under $200/month. If you're in a flat market or a high-PMI situation, run the full comparison with your actual numbers. But the default answer to "should I raid my 401(k) for a down payment" is almost always: no.