Vermont is the state that real estate investors romanticize and then never buy. The covered bridges, the fall foliage, the sense that nothing bad ever happens there — it all sounds like exactly the kind of durable, recession-resistant market you want exposure to. Then you run the numbers. Burlington's median home price hit $499,000 in May 2026 (Redfin), single-family rents average $3,050 per month (Zillow Rental Manager, June 2026), and Vermont's top state income tax rate is 8.75% — the highest in New England, the highest on the entire East Coast above Georgia. The romantic thesis and the cash-flow reality are pointing in opposite directions. Here is where each one actually leads.

The statewide median tells a slightly better story at $385,000, up approximately 6% year-over-year (Zillow Home Value Index, May 2026). But Vermont is a small state with thin inventory, and the entry-level properties that could theoretically cash flow are concentrated in smaller towns with weaker rental demand. Burlington is the market with scale — 45,000 residents, the University of Vermont, and a tight rental vacancy rate. And Burlington is where the math breaks cleanest.

Vermont's income tax structure runs in five brackets from 3.35% to 8.75%. The top bracket kicks in at $229,550 for single filers and $279,450 for joint filers (Vermont Department of Taxes, 2026). An investor with $60,000–$80,000 in gross rental income is looking at an effective tax rate of approximately 6.6–7.5% on that income, depending on total household income. Unlike some states that treat long-term capital gains more favorably, Vermont taxes capital gains as ordinary income at the full rate.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

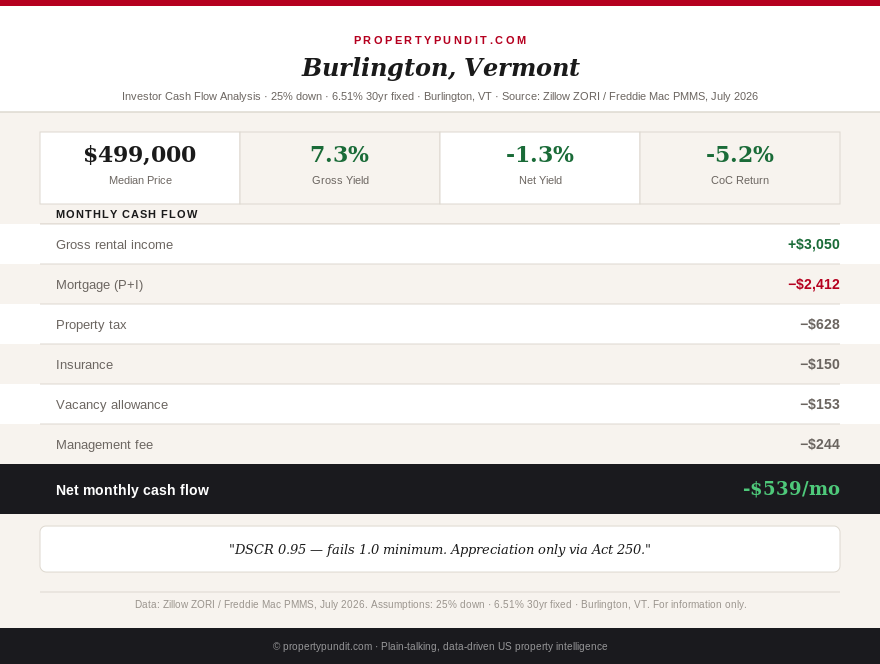

The Burlington PITIA math

Take a Burlington SFR at $499,000 with 25% down and a DSCR loan at 6.51% (Freddie Mac PMMS, July 2, 2026). Here is the full underwriting:

Down payment: $124,750. Loan amount: $374,250. Monthly P&I at 6.51% over 30 years: $2,364. Vermont nonhomestead property tax rate: 1.51% statewide average (Vermont Department of Taxes, 2026), or $7,535 per year on a $499k property, $628 per month. Homeowner's insurance: approximately $200 per month for Vermont (higher than national average due to winter weather claims). PITIA total: $3,192 per month.

Monthly gross rent for a Burlington SFR: $3,050 (Zillow Rental Manager, June 2026). DSCR: $3,050 divided by $3,192 = 0.956. The minimum DSCR threshold for a DSCR loan qualification is 1.0. Burlington at the median fails to qualify for DSCR financing at 25% down.

Subtract property management at 8%: $244 per month. Subtract vacancy allowance at 5%: $153 per month. Cash flow after all costs: $3,050 minus $3,192 minus $244 minus $153 = negative $539 per month. The effective DSCR including management and vacancy costs: 0.84. You are losing money before you write a single repair check.

The so-what for you: Burlington is a cash-flow negative market at every down payment between 20% and 35%. The only way to turn the math positive is a purchase price well below the median in a submarket with unusually strong rents — a combination that does not describe much of what trades in Burlington today.

What Act 250 actually does — and what it does not

Vermont's Act 250, passed in 1970, is the most comprehensive land use control law in the northeastern United States. Any development of 10 or more acres, any commercial project over 1 acre, any project above 2,500 feet in elevation, and any development in municipalities without local zoning plans requires a permit from one of nine regional environmental commissions. The review process covers criteria including traffic, water and air quality, educational capacity, fiscal impact, and visual aesthetics. Getting a permit can take 6 to 36 months.

The practical effect on housing supply is significant. Vermont has historically underbuilt relative to population need, and Act 250 is a material contributing factor. A state of approximately 650,000 people added fewer housing units per capita between 2000 and 2020 than virtually any other comparable-population state in the country. When supply is restricted, prices rise faster than they otherwise would. Vermont's appreciation has consistently outpaced the national average over multi-decade periods, even though the state's population growth is modest.

Here is what Act 250 does not do: it does not prevent property taxes from eroding your returns. It does not reduce Vermont's 8.75% income tax on rental income. It does not make Burlington rents high enough to support current prices at today's mortgage rates. Act 250 is an appreciation mechanism, not a cash-flow mechanism. It means that the home you buy in Vermont may be worth significantly more in 10 or 15 years because the state makes it genuinely difficult to build competing supply nearby. It means nothing about what happens to your bank account between now and then.

The so-what for you: Act 250 is a real structural advantage for Vermont's long-term appreciation case. An investor willing to absorb negative cash flow for 10-plus years in exchange for supply-constrained appreciation is taking a defensible position — similar to the thesis that justified buying coastal Maine or Hawaii in certain years. But this is a sophisticated, long-horizon position, not a "buy and collect rent checks" strategy.

The 8.75% income tax: what it costs in real dollars

Assume a Burlington SFR generating $36,600 in gross annual rent ($3,050 per month). After depreciation on the building value (approximately $9,500 per year on a $499k property at 80% building value), interest deductions, management fees, and maintenance, taxable rental income might net to $18,000–$24,000 per year. At Vermont's 6.6% marginal rate (the bracket below the top), that is $1,188–$1,584 per year in Vermont income tax on the rental income alone — roughly $99–$132 per month added to your holding cost.

If the investor is in the top Vermont bracket at 8.75%, the figure rises to $1,575–$2,100 per year, or $131–$175 per month. Compared to a zero-income-tax state like Tennessee, Mississippi, or Texas, Vermont costs an additional $1,600–$2,100 per year on a similar rental income profile. Tennessee's zero income tax is the reason Memphis at $185k beats Burlington at $499k on every investor metric except appreciation trajectory.

Capital gains on sale are treated as ordinary income in Vermont, with no preferential rate. Federal capital gains treatment still applies, but the Vermont state tax on a $150,000 appreciation gain — realistic over 15 years of Act 250-constrained supply dynamics — would be $13,125 at the 8.75% top rate. That is before any applicable depreciation recapture at the federal level. Exit costs from a Vermont investment position are meaningfully higher than exit costs from a Tennessee or South Carolina position.

The so-what for you: the 8.75% income tax is a genuine headwind on Vermont rental income and a significant exit cost at sale. Any investor modeling Vermont returns must include state income tax in both the holding period and the exit scenario or the projections will be materially wrong.

The statewide median at $385k: does it change the math?

At the statewide Vermont median of $385,000 with 25% down, the math improves slightly but does not produce positive cash flow. Down payment: $96,250. Loan: $288,750. P&I at 6.51%: $1,824. Nonhomestead property tax at 1.51%: $485 per month. Insurance: $160. PITIA total: $2,469. A SFR in a secondary Vermont market like Montpelier, Rutland, or St. Johnsbury commands average rents of $2,000–$2,200 per month for a 3-bedroom house. DSCR at $2,100 gross rent: 0.85. Cash flow after management and vacancy: approximately negative $595 per month.

Smaller markets have weaker rental demand and fewer comparable sales to establish DSCR values — lenders will scrutinize Vermont's thin rental comps more carefully than in a larger market. The lower statewide median actually produces worse cash flow than Burlington because rents in secondary Vermont cities do not compress proportionally with prices. Burlington's higher rents relative to suburban Vermont are the result of UVM enrollment, remote-worker demand, and employment at University of Vermont Medical Center. Remove those drivers and the rent support weakens without a corresponding drop in property tax.

Short-term rental: does Killington or Stowe rescue the math?

Vermont's ski and vacation markets — Killington, Stowe, Mad River Valley, and Sugarbush — attract short-term rental investors who underwrite on peak-season revenue rather than annual lease rates. A Killington SFR generating $4,000 per week during an 18-week ski season produces $72,000 in gross annual STR revenue. At that revenue level, even with the 8.75% Vermont income tax and high off-season vacancy, the annual cash flow can approach breakeven or modest positive territory.

Several Vermont municipalities, including Stowe, have passed or proposed STR registration requirements and occupancy caps in response to housing availability concerns. Killington and Ludlow (home of Okemo) are still relatively permissive for STR operations as of July 2026, but the regulatory trend across Vermont is toward more restriction, not less. Any investor underwriting a Vermont STR should model a scenario in which the municipality imposes a 90-day STR cap — a structure already adopted in parts of Stowe — and verify the current local rules before contracting.

Ski-area property prices reflect the STR premium. Killington chalets that produce $60,000–$80,000 in annual STR revenue list at $650,000–$900,000, which pushes PITIA to $4,200–$5,800 per month even at 25% down. The STR case is real, but the entry price for the properties that make the numbers work has been bid up significantly. The STR ski niche in Vermont is well-known, populated by sophisticated buyers, and priced accordingly — thin margins are the standard, not the exception.

The so-what for you: the Killington and Stowe STR markets represent the most viable Vermont investor entry, but require higher initial capital, careful regulatory due diligence, and active management. They are not a substitute for the buy-and-hold SFR market that works in Tennessee or Indiana. If you are sizing a Vermont STR investment, verify local ordinances directly with the town before committing earnest money.

Who Vermont actually makes sense for

Vermont is the right market for a specific investor profile: someone with a 15-plus-year horizon, willing to subsidize negative monthly cash flow with capital from other income, who believes the Act 250 supply constraint and Vermont's relatively stable economy produce consistent 3–5% annual appreciation. That investor is essentially buying a place where the government makes it legally difficult for competitors to build nearby — and accepting that the current income economics do not work in exchange for the long-term equity thesis.

For context, Maine's Portland market follows a similar logic — rent caps, high purchase prices, negative cash flow, but a geographic supply constraint (peninsula and coastline) that has driven consistent appreciation. Hawaii is the extreme version, where cash flow is negative in every market and the entire investor thesis is appreciation plus lifestyle value. Vermont sits between coastal Maine and Hawaii on this spectrum: constrained supply that supports prices, but no cash flow at current rates and prices.

The frankest assessment: an investor with cash from the sale of a Tennessee or Indiana property looking to redeploy into a position with lower ongoing management burden and supply-constrained appreciation has a reasonable case for Vermont. An investor expecting Vermont to produce monthly income to fund living expenses does not. The 8.75% income tax and 1.51% nonhomestead property tax combine to make Vermont one of the most expensive states in which to hold investment property on a current-income basis — even before the DSCR math fails at the entry price.

The math points toward this conclusion for most DSCR-oriented investors: Vermont is not the play right now. Tennessee's zero income tax, confirmed in the Tennessee market analysis, produces better investor economics at Memphis sub-$155k than Vermont produces anywhere at current prices. If appreciation is the primary thesis, compare Vermont's supply-constrained case directly against Idaho's similar dynamic — Idaho also runs negative cash flow everywhere, but without Vermont's income tax burden. The investor who genuinely wants Vermont exposure is better served understanding exactly what they are buying: a bet on Act 250 and the state's historical resistance to overbuilding, not a rental income stream.