Charlotte, North Carolina has a genuine reputation as one of the best cities for young buyers in the Southeast. Banking headquarters, a growing tech sector, no state income tax on retirement income, and an international airport that makes the city feel larger than it is. If you are a buyer at $112k income trying to decide where to plant roots in July 2026, Charlotte is on the shortlist for good reason. So is Columbus, Ohio — a city that tends to get dismissed as the kind of place people move to when they cannot afford anywhere else. The dismissal is wrong, and the numbers prove it. Columbus beats Charlotte on monthly cost by $823, on 5-year appreciation gain, and on down payment required. Here is the case, with every number sourced.

The counterintuitive finding is not just that Columbus is cheaper to buy — everyone knows Columbus is cheaper. What most buyers comparing these two cities miss is that Columbus is also growing faster, that Ohio's lower income tax reduces the Charlotte income-tax advantage, and that after you factor in property taxes, Franklin County's higher rate still produces a lower dollar amount per month than Mecklenburg County because Columbus's purchase price is $137,000 lower. The math stacks from every direction.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The side-by-side monthly cost table

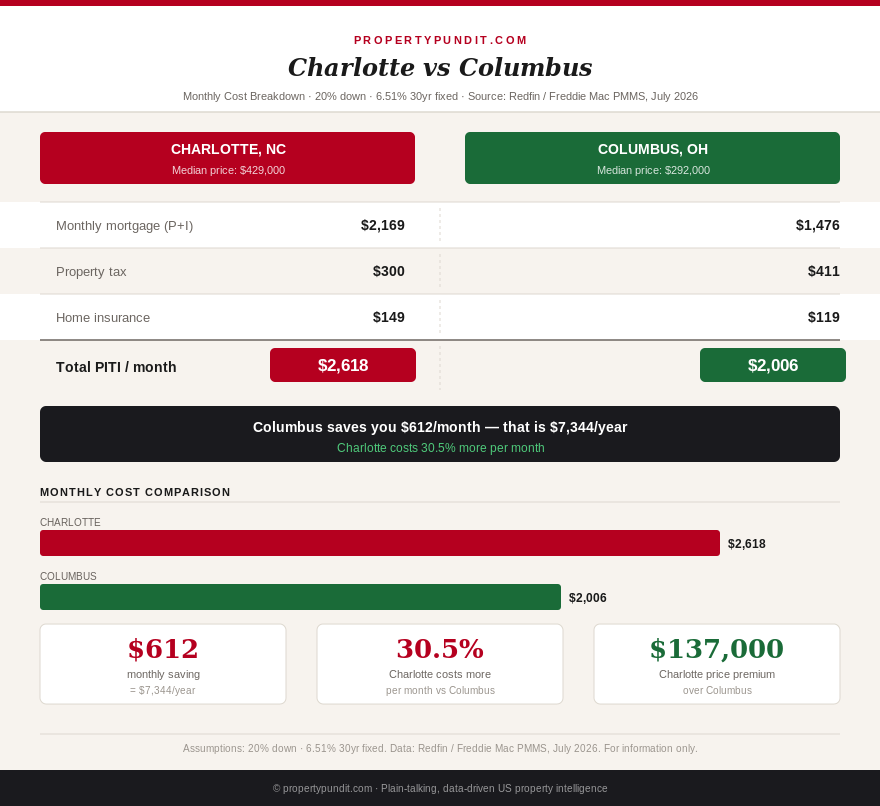

All figures below use 20% down payment and a 6.51% 30-year fixed rate (Freddie Mac PMMS, July 2, 2026). Income tax uses 2026 state rates at $112,000 gross income.

| Item | Charlotte, NC | Columbus, OH |

|---|---|---|

| Median home price | $429,000 | $292,000 |

| 20% down payment | $85,800 | $58,400 |

| Loan amount | $343,200 | $233,600 |

| Monthly P&I at 6.51% | $2,169 | $1,476 |

| Property tax/month | $300 (0.84%, Mecklenburg) | $411 (1.69%, Franklin Co.) |

| Homeowner's insurance | $149 | $119 |

| PITI total | $2,618 | $2,006 |

| PITI as % of $112k income | 28.1% (at the ceiling) | 21.5% ($607 buffer) |

| State income tax/month | $443 (4.75% flat, NC) | $232 (graduated, OH) |

| All-in monthly cost | $3,061 | $2,238 |

| Columbus monthly advantage | $823/month |

Sources: Redfin median home prices (Charlotte, Columbus; May 2026), Mecklenburg County tax records (effective rate 2026), Franklin County Auditor non-owner-occupied rate (2026), Ohio Department of Taxation graduated brackets (2026), North Carolina Department of Revenue flat rate (4.75%, 2026), Freddie Mac PMMS (July 2, 2026).

The so-what for you: if you are evaluating these two cities purely on monthly financial impact, Columbus saves you $823 per month from day one — that is $9,876 per year, which compounds significantly over a 5-year horizon. The question worth asking is whether Charlotte provides $823 per month in additional value in the form of career access, climate, amenities, or appreciation potential. The answer on appreciation, as the next section shows, is no.

The income tax gap most Charlotte buyers do not model

North Carolina's income tax is a flat 4.75% on all taxable income in 2026. Ohio uses a graduated structure that is far more favorable at $112,000 income. Ohio's brackets in 2026: 0% up to $26,050, 2.765% on income up to $46,100, 3.226% on income up to $92,150, and 3.688% on income above $92,150. On $112,000 gross income, effective Ohio income tax works out to approximately $2,783 per year, or $232 per month. North Carolina at the same income: $112,000 times 4.75% equals $5,320 per year, or $443 per month.

The difference: $211 per month. This is money that a Charlotte buyer pays every month that a Columbus buyer does not. Note that this is the state income tax only — both cities have similar local income tax situations for employees (Columbus has a 2.5% city income tax that applies to residents and workers; this applies equally to anyone working in Columbus and is separate from the state comparison above). When counting city income tax, Columbus residents face a 2.5% local rate, while Charlotte residents face no city income tax. Including the Columbus city income tax at 2.5% on $112k adds approximately $233/month, bringing Columbus's total tax cost closer to Charlotte's and narrowing the all-in advantage to roughly $590/month. This is still a meaningful gap, and the monthly PITI difference remains $612.

The so-what for you: if you are working remotely and your employer is not based in Columbus, you may not owe the 2.5% Columbus city income tax — consult a tax professional on your specific situation. If you do owe it, Columbus still comes out $590/month ahead of Charlotte on the full all-in monthly cost including all taxes.

Appreciation: Columbus is actually winning

This is the part of the comparison that surprises most people. Charlotte is known as a fast-growing Southeast city. Columbus is assumed to be stable Midwest. In 2026, the data says otherwise.

Columbus home prices rose approximately 6% year-over-year in 2026, driven primarily by the Intel Ohio One campus — a $28 billion semiconductor manufacturing investment in New Albany, Ohio, 20 minutes from Columbus. The campus is bringing 3,000 direct Intel jobs and an estimated 7,000 to 10,000 indirect supply-chain and service jobs to central Ohio (Intel, confirmed May 2026 with CHIPS Act funding). The employment anchor is the kind of structural demand driver that historically sustains appreciation through rate cycles. Columbus's year-over-year appreciation of 6% compares to Charlotte's 2.8% (Case-Shiller / Redfin, May–June 2026). Raleigh, the comparable high-growth North Carolina city, is down 3.4% year-over-year. Charlotte is outperforming Raleigh but still well below Columbus on growth rate.

Five-year appreciation at current rates:

- Charlotte at $429k growing at 2.8% per year: value after 5 years = $493,000. Gain: $64,000.

- Columbus at $292k growing at 6% per year: value after 5 years = $391,000. Gain: $99,000.

Columbus produces $35,000 more in equity gain over five years, on a property that cost $137,000 less to buy and $823 more per month to save rather than spend. Over 5 years, the Columbus monthly cost advantage compounds to $49,380 in additional savings (60 months times $823). Total Columbus financial advantage at year 5: approximately $84,380 compared to Charlotte, counting both the appreciation gap and the monthly cost savings.

The so-what for you: anyone buying a home in July 2026 at $112k income who is choosing between these two cities on financial grounds alone should choose Columbus. The only scenarios in which Charlotte wins are: (1) your career requires Charlotte specifically and the income premium from being in the Charlotte market exceeds $823/month in higher earnings; (2) you plan to stay fewer than 3 years, in which case transaction costs make both cities poor choices; or (3) you place high personal value on Charlotte's climate, amenities, or culture beyond what the numbers capture.

The case for Charlotte that the numbers cannot capture

Charlotte's real appeal is not in the spreadsheet. The city has Bank of America's headquarters, a growing presence from Truist, Wells Fargo, and Honeywell, a developing tech corridor in the South End and University Research Park, and an international airport with direct connections to Europe and Latin America. Charlotte has warm winters, proximity to both mountains and coast, and a lifestyle infrastructure — restaurants, sports, cultural venues — that Columbus is still building toward. These are real considerations for buyers in their 30s deciding where to spend the next decade. No financial model captures the value of living somewhere you genuinely want to be.

Charlotte's price-to-rent ratio of approximately 19 is also lower than many comparable Southeast cities, meaning the buy-versus-rent math in Charlotte is not as unfavorable as cities like Austin or Miami. At $112k income, a Charlotte buyer is right at the 28% housing guideline — which means the purchase is financially feasible, not comfortable. Any income growth above current levels, any bonus income, or any roommate arrangement changes the calculus meaningfully.

Columbus, for its part, has made significant investments in downtown development, the Short North arts district, and Easton Town Center. The food and arts scene has improved substantially over the past decade. Columbus is not Atlanta or Charlotte in terms of big-city amenities, but for buyers who prioritize financial margin and do not need the full Southeast urban package, it delivers more per dollar than almost any comparable market in the country.

The verdict at $112k income in July 2026

The math points toward Columbus. Lower purchase price. Lower monthly payment. Lower income tax. Higher appreciation rate. More down payment flexibility ($27,400 less required). The 28% housing rule at $112k income gives Columbus buyers $607 per month of financial breathing room; Charlotte buyers have essentially none. If an unexpected repair, a period of reduced income, or a second child enters the picture in year two, the Columbus buyer has a substantial buffer that the Charlotte buyer does not.

Columbus is not the right answer if Charlotte is where your career needs you, if your personal priorities require the Southeast lifestyle specifically, or if you are placing a bet that Charlotte's long-term growth trajectory will outpace Columbus's Intel-driven surge. Those are legitimate considerations that only you can weigh. The data on everything else favors Columbus by a margin that is too large to ignore. The 7 cities where $112k income still buys a home in 2026 article adds six other options to benchmark against if neither of these cities is the right fit. If you are seriously weighing Columbus and want to understand the underlying investor cash-flow math, the Ohio market spotlight covers the Intel appreciation thesis alongside the Franklin County property tax in full detail. The closing costs explainer will help you model the full out-of-pocket cost for either city once you are ready to make an offer.