If you're working through the Western states looking for a cash-flow entry, Utah might look tempting from the tax profile alone. The effective property tax rate of 0.53% is the lowest in the West — half of Colorado's, a third of Nevada's higher-county rates, and a fraction of what Texas charges. There is no rent control anywhere in the state. The landlord-tenant laws lean decidedly in the owner's favor. On paper, Utah should be the friendliest investor climate west of the Rockies. In practice, the state's "Silicon Slopes" tech corridor turned it into one of the most expensive housing markets in the country, and rental income never came close to keeping pace.

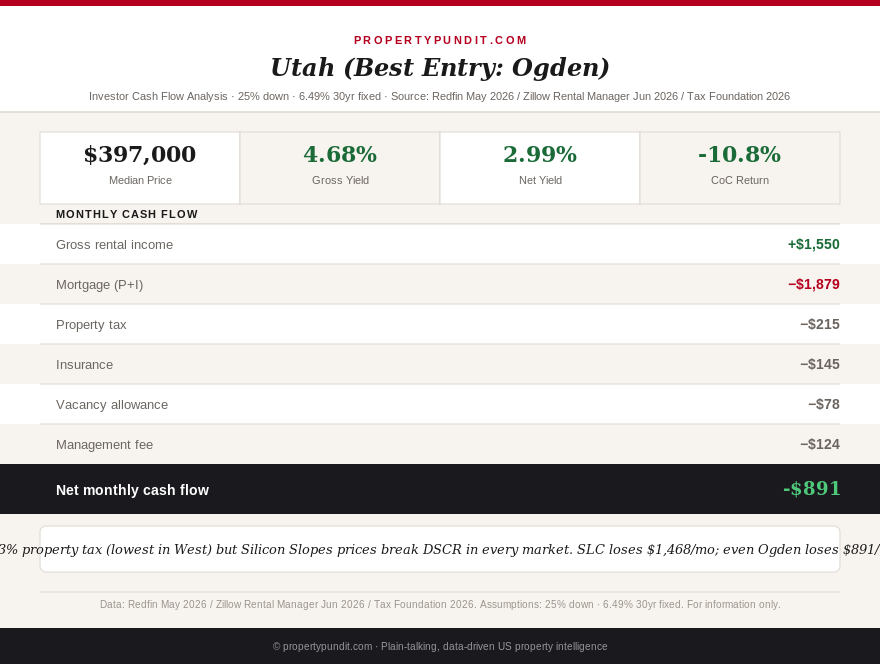

The statewide median home price reached $528,124 in May 2026, up 1.6% year over year (Redfin, May 2026). Salt Lake City proper hit $585,000 — up 3.5% — with homes going under contract in 29 days. Ogden, the most affordable of Utah's major cities, sits at $397,000 with a $1,550 average monthly rent. That is the best ratio in the state. It still does not work.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The tax profile: what the numbers actually say

Start with what Utah gets right. The 0.53% effective property tax rate is real, statewide, and applies equally to investment properties — there is no separate investor classification surcharge as there is in South Carolina (6% vs. 4% assessed value ratio) or Rhode Island. On a $397,000 Ogden acquisition, property tax runs approximately $215 per month. On a $585,000 Salt Lake City home, it is $327 per month. Both figures are dramatically better than what Texas investors pay — Bexar County (San Antonio) charges $558 per month on a $295k property, as we covered in Tuesday's Texas spotlight.

The income tax picture is more nuanced than most investor research presents. Utah does have a state income tax — 4.45% flat rate for 2026, reduced from 4.5% after the legislature passed its sixth consecutive tax cut earlier this year (Tax Foundation, 2026). That matters for investors comparing Utah to the zero-income-tax states: Tennessee, Texas, and South Dakota, which have all appeared in this series recently. On $30,000 in gross rental income, Utah's 4.45% tax costs approximately $1,335 per year ($111/month) after standard depreciation deductions. It is not the deal-breaker. The price-to-rent ratio is the deal-breaker.

Utah also has no rent control — another genuine advantage in a Western market where Oregon caps annual rent increases at 9.5% and California limits increases statewide. Utah landlords can price to market and raise rents at lease renewal without statutory restriction. That is the right policy environment for investors. The problem is that the market they're entering priced itself well ahead of rents years ago, and the gap has only widened.

The full PITIA math across Utah's major markets

All calculations use 25% down, 6.49% 30-year fixed (Freddie Mac PMMS June 25, 2026), 8% property management, and 5% vacancy. Rents from Zillow Rental Manager and RentCafe, June 2026.

| Market | Median price | P&I (25% down) | Tax + ins. | Avg. rent | DSCR | Monthly CF |

|---|---|---|---|---|---|---|

| Ogden | $397,000 | $1,879 | $360 | $1,550 | 0.69 | -$891 |

| Provo | $485,000 | $2,295 | $392 | $1,500 | 0.56 | -$1,382 |

| Salt Lake City | $585,000 | $2,768 | $527 | $2,100 | 0.64 | -$1,468 |

| Park City | $1,200,000+ | $5,676+ | $880+ | N/A long-term | STR only | LTR fails |

Sources: Redfin May 2026 (prices); Zillow Rental Manager / RentCafe June 2026 (rents); Tax Foundation 2026 (property tax rates); Freddie Mac PMMS June 25, 2026 (6.49%). PropertyPundit calculation.

Every market fails DSCR underwriting — and DSCR lenders typically require a minimum of 1.0 to 1.25, well above any number in this table. If you were to attempt a DSCR loan on a Utah SFR, no major lender would approve it at these price and rent levels. You'd need to bring roughly 40% to 50% down to make the math work on paper — at which point the cash-on-cash return is so thin it no longer justifies the capital allocation.

Why the property tax advantage disappears at scale

The comparison to Texas is instructive. Texas charges 2.0% to 2.3% in property taxes — we modeled Bexar County at 2.27%, which adds $558 per month on a $295k San Antonio acquisition. Utah's 0.53% is genuinely superior. But compare markets at equivalent investment price points and the advantage vanishes. An Ogden property at $397k pays $215 per month in property tax. A Tulsa, Oklahoma property at $220k — with Oklahoma's 0.92% rate — pays $168 per month in property tax. You're paying less in absolute dollars for Oklahoma's property despite a higher percentage, because the base price is lower. And Tulsa sub-$185k produces positive cash flow of +$121/month with a DSCR of 1.27, as we covered in the Oklahoma spotlight.

The lesson isn't that low property tax rates are meaningless — they're not. Utah's 0.53% is a genuine structural advantage that will matter more as prices eventually moderate relative to rents. The lesson is that a great tax rate in an expensive market can still produce worse absolute economics than a higher tax rate in a cheaper market.

Silicon Slopes and the rent decoupling problem

The structural reason Utah's rent-to-price ratio is broken comes down to what drove prices up. Adobe, Microsoft, Qualtrics, Pluralsight, and dozens of other tech firms established major operations in the SLC-to-Provo corridor (branded "Silicon Slopes" by local boosters) through 2018 to 2022. High-earning tech workers bid prices up sharply. Between 2020 and 2023, Salt Lake County home prices rose over 50%. Rents did not. Rents are set by local wage levels broadly — not just by tech workers — and Utah's overall median household income of approximately $79,000 (U.S. Census Bureau, 2024) constrains what most tenants can pay.

The result is a classic decoupling: prices in SLC appreciated at a rate that implies a 2-3% gross yield, but local rents can only support a 5-6% yield before the math breaks. At 6.49% mortgage rates, you need a gross yield closer to 8% to clear positive cash flow. No Utah market delivers that on an SFR. A duplex or small multifamily structure changes the calculation somewhat — two units sharing the same lot can hit 7%+ gross yield in Ogden — but SFR buy-and-hold is a non-starter at current rates.

What Utah investors should actually consider

There are two scenarios where Utah makes sense for capital deployment in 2026. The first is appreciation plays in specific corridors. Lehi and American Fork in Utah County (part of Silicon Slopes proper) have seen consistent 8-12% annual appreciation over the past decade, and with BYU's enrollment growth and continued tech hiring, the demand fundamentals remain. These are not cash-flow investments — they're appreciation bets with negative carrying costs, essentially financed speculative land holds. That is a viable strategy for investors with capital reserves, but you need to model the carry cost explicitly: at $485k with 25% down and -$1,382/month, you're paying $16,584 per year to hold the property before any appreciation.

The second is short-term rental in Park City and the Wasatch ski corridor. Utah's STR regulations are less restrictive than many Western mountain markets, and Park City attracts premium bookings year-round. At nightly rates of $300 to $600 for ski-season weeks and $150 to $250 for summer shoulder months, a well-located Park City STR can cover carrying costs on a $1.2M+ acquisition. This is a fundamentally different investment category — hospitality management, not passive rental income — and carries higher operating expenses, occupancy risk, and potential regulatory change.

For a standard SFR buy-and-hold investor, frankly, the math points away from Utah at current rates. The states where the numbers work — Mississippi at $144k, Indiana sub-$185k, Oklahoma at $220k, Pennsylvania's Pittsburgh corridor — deliver DSCR above 1.25 and positive monthly cash flow without requiring appreciation assumptions. Utah might get there if rates fall to 5% and prices moderate another 10 to 15% relative to rents. That is a 2028 thesis, not a 2026 entry.

The DSCR loan framework we covered in May shows exactly where the minimum qualifying threshold sits — and Utah is nowhere near it. Until rent growth catches prices or rates fall meaningfully, most investors who run these numbers end up looking at a different state.