If you took out a 5/1 adjustable-rate mortgage in 2021 at 2.75% or 3.0%, you already know the reset letter is coming — or has arrived. Your five-year fixed period is up. The rate you locked during the lowest mortgage environment in modern history is about to be replaced by whatever a formula tied to SOFR and a 30-year fixed market at 6.49% spits out. Most financial coverage treats this as a two-line summary: your rate goes up, and you should probably refinance. That framing misses the one number that actually changes your decision.

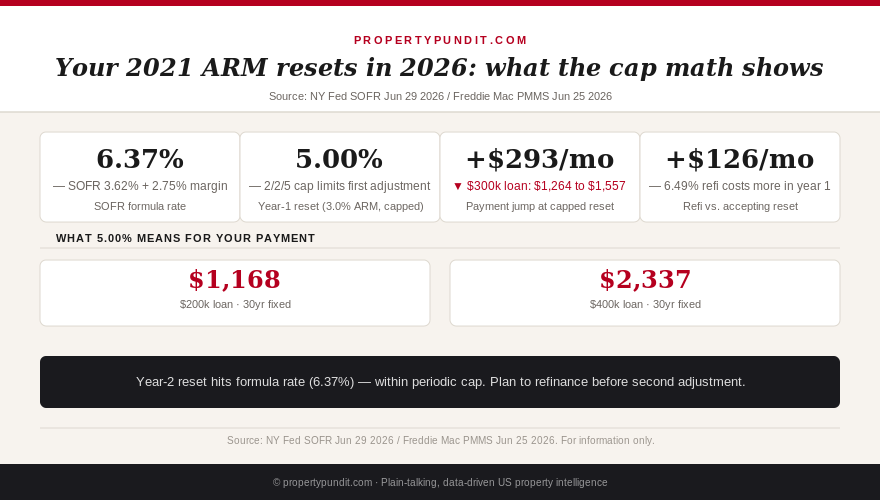

The SOFR 30-day average stood at 3.62% as of June 29, 2026 (Federal Reserve Bank of New York). Add the typical residential ARM margin of 2.75% and the raw formula gives you 6.37%. That sounds terrifying if you started at 3.0%. But it's not the rate you will pay at your first reset. Not even close.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

How the 2/2/5 cap structure actually works

Every 5/1 ARM comes with a rate cap structure stated in your loan documents. The most common is 2/2/5: the rate cannot rise more than 2 percentage points at the first adjustment, more than 2 points at any subsequent annual adjustment, or more than 5 points over the life of the loan. That first number is the one that matters right now.

If your original rate was 3.0%, the 2-point initial cap means the highest your rate can go at the first reset is 5.0% — regardless of what SOFR plus your margin calculates. The formula is the target; the cap is the ceiling. Since 6.37% exceeds the 5.0% ceiling for a 3.0% borrower, your rate resets to 5.0%. Full stop.

The table below shows how this plays out across the range of 2021 ARM rates:

| Original ARM rate | Formula rate (SOFR 3.62% + 2.75%) | First reset cap (+2%) | Actual reset rate |

|---|---|---|---|

| 2.50% | 6.37% | 4.50% | 4.50% (capped) |

| 2.75% | 6.37% | 4.75% | 4.75% (capped) |

| 3.00% | 6.37% | 5.00% | 5.00% (capped) |

| 3.25% | 6.37% | 5.25% | 5.25% (capped) |

| 3.50% | 6.37% | 5.50% | 5.50% (capped) |

Every 2021 ARM holder hits the cap at their first adjustment. The formula gives 6.37%; the cap pulls it back to a range of 4.50% to 5.50% depending on your start rate. For most borrowers, the first-year reset rate is meaningfully below the current 30-year fixed rate of 6.49%. That changes the math entirely for the question of whether to refinance right now.

The payment math: what the first reset costs you

Start with a $300,000 original loan at 3.0%. After five years of regular payments at $1,264 per month, your remaining balance is approximately $266,700. The first reset hits and your rate adjusts to 5.0% (capped). With 25 years and that balance, your new payment works out to $1,557 per month — a jump of $293 per month. That is real money. But here is where the analysis most financial writers skip: compare that to refinancing.

A new 30-year fixed loan on your $266,700 balance at today's 6.49% produces a payment of approximately $1,683 per month. Accepting your capped reset costs $126 less per month than refinancing. You also avoid $3,000 to $6,000 in closing costs. The first-year math squarely favors accepting the reset.

| Scenario | Rate | Monthly P&I | vs. current payment |

|---|---|---|---|

| Current (original ARM, year 5) | 3.00% | $1,264 | baseline |

| First reset (year 6, capped) | 5.00% | $1,557 | +$293/month |

| Refinance now (30yr fixed) | 6.49% | $1,683 | +$419/month |

| Second reset (year 7, formula rate) | 6.37% | $1,749 | +$485/month |

Loan: $300,000 original at 3.0%, $266,700 remaining balance after 60 months. PropertyPundit calculation, July 2026. Freddie Mac PMMS 6.49% June 25, 2026; SOFR 3.62% NY Fed June 29, 2026.

The math points toward accepting the first reset for most borrowers — unless you have a compelling reason to lock in certainty now, such as a near-term job change or a plan to sell within three years.

What happens at the second adjustment

This is where the analysis gets uncomfortable. At the second annual adjustment (year seven), the periodic cap of 2% applies from your post-reset rate of 5.0%. The formula says 6.37%; the periodic cap says you can go up to 7.0%. Since 6.37% sits under 7.0%, your rate moves to the formula rate: 6.37%. The cap does not protect you at adjustment two the way it did at adjustment one.

On your remaining balance at that point (roughly $258,000 with 24 years left), a rate of 6.37% produces a payment of approximately $1,749 per month. That is an additional jump of $192 from the year-six reset level, and $485 per month above your original payment. At this stage, your ARM rate is essentially in line with current 30-year fixed rates — so the argument for refinancing gets much stronger.

The honest reading of your situation: the 2/2/5 cap gives you one year of breathing room at a below-market rate. You should use that year purposefully, not passively.

Your one-year window: what to actually do

The data points toward a clear sequence. First, find your loan documents and verify your cap structure — 2/2/5 is standard but some lenders used 5/2/5 (a steeper first-year cap). Your note or closing disclosure states this explicitly. If your initial cap is 5%, your first-reset ceiling is your original rate plus 5%, not plus 2% — which means the formula rate of 6.37% may already be within reach at adjustment one.

Second, set a rate trigger for refinancing. Our 5 mortgage rate triggers framework covers this in detail: for most 2021 ARM borrowers whose rate was 3.0%, refinancing starts to make financial sense when the 30-year fixed falls below 5.75% (which produces a payment close enough to your year-two adjusted rate that you eliminate the reset risk without paying much more). With the Fed on hold and no cuts expected before 2027 per CME FedWatch, that trigger is probably 12 to 18 months away at minimum.

Third, watch the SOFR trend. The 30-day SOFR average drives your adjustment formula. If SOFR falls from its current 3.62% to, say, 2.75% — which would require Fed cuts — your year-two formula rate drops to 5.5% (2.75% plus 2.75% margin), and the reset is far less painful. Your ARM's flexibility works both ways.

Fourth, consider the assumable mortgage angle if you plan to sell. FHA and VA ARM loans are assumable — a buyer who takes over your 5.0% first-reset rate has a genuinely attractive deal versus the current market.

The ARM picture homeowners with fixed rates miss

There is a broader implication here that extends beyond the 2021 cohort. The conversation around rate lock decisions typically focuses on fixed-rate holders sitting on 3-4% mortgages who cannot move. ARM holders face a different pressure — their rates are moving whether they act or not. But because the cap structure is misunderstood, many are refinancing into 6.49% fixed mortgages to "eliminate uncertainty," when accepting the first reset would have cost them $126 less per month.

Frankly, if you are a 2021 ARM borrower with a 2/2/5 cap who has no plans to move in the next 12 months, the data says stay put through the first reset. The market is doing you a one-year favor. Use that year to watch rates, set your trigger point, and shop at least three lenders before you sign anything. The refi trigger framework gives you the exact number to watch for your original rate.

The second adjustment at year seven is where you should be planning to act — not now, unless your rate was 3.50% or higher and your periodic first-cap calculates above 5.5%, at which point refinancing today narrows the gap enough to justify the closing costs.