The offer is accepted. Your phone buzzed with the agent's message and your stomach did the thing — relief, terror, both at once. You've been saving for years, you've been outbid before, and now you finally have a deal. What you probably don't know yet is that the next 48 hours are the riskiest of the entire transaction — not because the seller might back out, but because you can accidentally blow it through inaction.

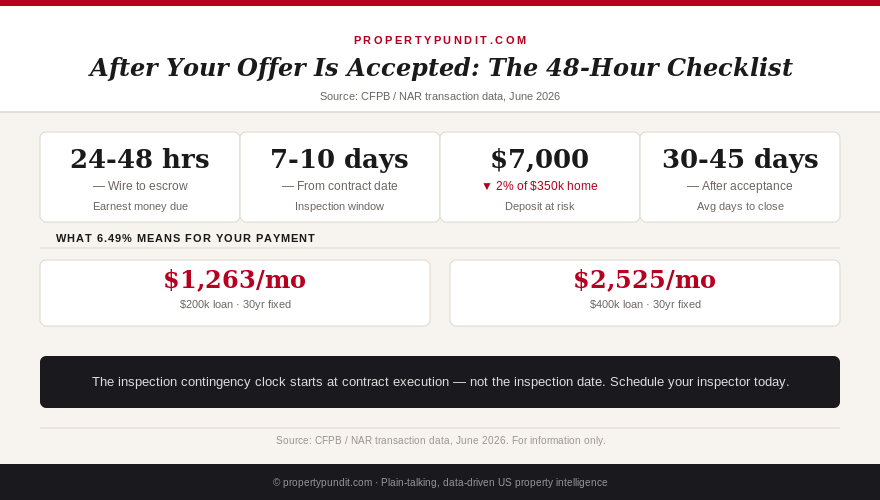

On a $350,000 home with a standard 2% earnest money deposit, you have $7,000 sitting in escrow that you can lose if you miss a single contractual deadline. The inspection contingency runs 7 to 10 days, and that clock started ticking the second both parties signed — not when you actually schedule the inspection. Your lender needs to be notified today, not this week. And the title company you pick in the next few days will cost you between $800 and $2,300, depending on who you choose.

This is what the first 48 hours actually look like, with the dollar consequences attached to every step you delay.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

Step one: wire the earnest money deposit within 24 to 48 hours

Earnest money is not a courtesy gesture. It is a contractual obligation with a specific deadline written into your purchase agreement — typically 24 to 48 business hours after execution. The standard deposit runs 1 to 3% of the purchase price: on a $350,000 home, that is $3,500 to $10,500. Most buyers in competitive markets land at 2%, so assume $7,000 is on the line.

The money goes to a neutral escrow account — held by the title company, the seller's brokerage, or an escrow company depending on your state. It is not paid to the seller directly, which is the most common misconception first-time buyers have about how this works.

If you wire the money correctly and the deal closes, every dollar applies to your down payment or closing costs at settlement. You don't lose it — it's just moving early. If the deal falls through due to a contingency you properly invoked (inspection, financing, appraisal), you get it back in full. The danger zone is missing the wire deadline entirely, or canceling the deal after all contingencies expire.

The practical checklist for the wire: confirm the escrow company's wiring instructions directly by phone before sending — wire fraud targeting home buyers is the fastest-growing real estate scam of the decade. Never send funds based solely on emailed instructions without a verbal confirmation call to a number you independently look up. Once wired, get a confirmation number and send it to your agent. Do this today, not tomorrow.

For a deeper breakdown of what contingencies protect your deposit in virtually every scenario first-time buyers actually face, see our earnest money myth explainer.

Step two: call your lender before end of business today

Your pre-approval letter showed the seller you were serious. It is not a mortgage. The formal loan application starts now, and every day you delay adds risk that your closing falls outside the contract timeline.

Here is what your lender needs from you in the next 24 hours: a copy of the fully executed purchase contract, confirmation of the purchase price and closing date, and any updated financial documents they request (pay stubs, bank statements). They will use this information to order the appraisal, which in many markets runs 10 to 21 days and cannot start until the lender places the order.

Pre-approval letters typically expire after 60 to 90 days from the issue date. If yours is running close to expiration — or if your financial situation has changed since approval — tell your lender now, not the week before closing. A lender discovering an income change during underwriting in the final week of a transaction can kill a deal that took months to get to this point.

One thing most buyers skip at this stage: ask your lender whether a rate lock makes sense now or at a specific point in the process. With the 30-year fixed at 6.49% (Freddie Mac PMMS, June 25, 2026) and no Fed cuts expected until 2027, locking in within the first week of contract avoids the risk of a rate spike during underwriting. Rate locks typically run 30, 45, or 60 days. A 45-day lock on a $280,000 loan costs nothing at most lenders but protects you against a 0.25% rate increase that would add $46/month permanently.

Step three: schedule the home inspection within hours, not days

This is the step most buyers get wrong, and the one with the most direct dollar consequence.

Your inspection contingency window — the period during which you can request repairs, negotiate a credit, or walk away with your deposit intact — starts at contract execution. Not the day you schedule the inspection. Not the day the inspector shows up. The moment both parties signed. On a standard 10-day inspection window, if you spend two days celebrating your accepted offer and then start calling inspectors, you've already used 20% of your contingency window on scheduling delays.

In most markets, a good home inspector has a 3 to 7 day booking lead time. That means you need to start calling today. For a $350,000 home, a general inspection runs $400 to $600. Add a sewer scope if the house is over 30 years old ($150 to $250) and a radon test if you're in a moderate-to-high-risk zone ($100 to $175). Budget $700 to $1,000 total for a thorough inspection package.

Once you have the inspection report, you have two practical options in a buyer's market: request a repair credit (a lump sum at closing) rather than a repair list, or walk away if the issues are structural. The credit approach is almost always more effective than asking the seller to manage contractors. On a report showing $12,000 in needed work, requesting an $8,000 credit at closing tends to close faster and with less friction than handing over a repair checklist. We covered the math on this in our inspection credit versus repair request explainer.

Step four: pick your title company and understand the $500 to $1,500 gap

In most states, the buyer chooses the title company — and most buyers let their agent choose it for them without asking about price. That is a $500 to $1,500 mistake on a typical transaction.

Title insurance has two components: the lender's policy (required by your mortgage company) and the owner's policy (optional but strongly recommended, since it protects your equity for as long as you own the home). On a $350,000 purchase, the total title cost including both policies, search fee, and closing fee typically runs $1,800 to $3,200 depending on the provider and state.

In states where title rates are not regulated — which includes most of the country — you can shop. Call two or three title companies, ask for a quote on a simultaneous-issue title package (where lender and owner policies are issued together at a discount), and compare the settlement fee and search fee alongside the policy cost. The quality of title searches does not vary much between providers; the price does.

In Texas, Florida, and New York, title insurance rates are state-regulated, so the premium itself won't vary — but the closing fee, search fee, and endorsement charges will. Ask for an itemized quote in all cases.

Your title company also handles the closing itself: they verify the chain of title, clear any existing liens, prepare the settlement statement, and coordinate the final wire transfer. Choose someone with clear communication standards, because you will be sending them financial information and sensitive documents for the next 30 to 45 days.

For the full breakdown of what every line on your closing disclosure actually means, our closing costs explainer walks through each fee bucket.

Step five: bind your homeowner's insurance before closing

Your mortgage lender requires proof of homeowner's insurance before they will fund the loan. Most buyers know this. What fewer buyers know is that you should start shopping now, not in the final week before closing.

Insurance binders — the temporary proof-of-coverage document your lender accepts — take a few days to issue after you select a policy. If you wait until day 28 of a 30-day closing to start, you are one slow insurer away from delaying your settlement date. A single day's delay in closing costs money: the seller may charge a per-diem penalty (often $100 to $300/day), your rate lock may expire, and moving arrangements get disrupted.

Shopping early also saves money. Homeowner's insurance rates vary significantly by provider for identical coverage on the same property. Get at least three quotes, and ask each insurer to run a quote that includes any bundling discounts with your existing auto policy. The annual premium on a $350,000 home typically runs $1,200 to $2,200 in most US markets — though Florida, Texas, and coastal states push higher. A $400/year difference between quotes is $12,000 over 30 years of ownership.

Confirm with your lender what coverage minimums they require (typically replacement cost value, not market value), and send the binder to your lender's insurance desk at least 72 hours before your scheduled closing date.

The 48-hour master checklist

Here is the full list in order, with the dollar consequence of delay attached to each item:

Wire the earnest money deposit (within 24 to 48 hours): $7,000 at risk if missed or if the deal falls through outside a contingency.

Call your lender and send the executed contract (today): appraisal cannot start until the lender orders it; every day of delay compresses your closing timeline and raises rate lock costs.

Schedule your home inspector (today, not tomorrow): inspection contingency window started at contract execution; a 3 to 5 day delay to schedule means the inspector's findings arrive late and reduce your negotiation window.

Select your title company (within 48 hours): $500 to $1,500 in savings possible by comparing quotes; your agent has preferences but you have the choice.

Start homeowner's insurance quotes (within 48 hours): insurance binders take days to issue; starting late risks a closing delay and per-diem penalties of $100 to $300/day from the seller.

Notify your employer (within 72 hours): if your lender needs an employment verification letter, getting it requested early avoids a last-minute scramble; HR departments at large companies can take 5 to 10 business days to issue verification letters.

Stop using your credit (starting now): your lender will run a credit refresh before closing. A new car loan, a store card opened for a furniture purchase, or a balance increase on an existing card can change your debt-to-income ratio and trigger a re-underwrite. Freeze discretionary borrowing until the keys are in your hand.

What actually threatens your deal at this stage

Most deals that fall apart after offer acceptance do so for one of three reasons: the appraisal comes in below the contract price, the inspection reveals something neither party anticipated, or the buyer's financing changes between pre-approval and closing.

An appraisal gap — where the appraiser values the home below the contract price — is manageable if you plan for it. The options are renegotiating the price, paying the gap in cash, or walking away under an appraisal contingency. A buyer who has already spent $1,000 on inspections and two weeks of emotional investment is more likely to pay the gap than to walk, which is why sellers prefer buyers with fewer contingencies. Know your number before you get to that conversation: how much above the appraised value are you willing to pay, and do you have the liquidity to do it?

A financing fall-through is the most preventable outcome of all. It happens when buyers change jobs, take on new debt, or move large sums of money between accounts during underwriting without telling their lender. Your loan file is a live document and underwriters check for changes. Keep your lender informed of any financial changes, no matter how minor they seem. A freelance contract deposit that lands in your checking account mid-underwrite looks like undisclosed income and will trigger questions. Tell your lender first.

The math here is straightforward: the buyers who close on time are the ones who treat the 48 hours after acceptance as the most urgent part of the transaction. The home is under contract. The work starts now. Don't wait for your agent to remind you — they are juggling multiple clients, and the deadlines are yours to track.

You spent months getting to an accepted offer in a market where sellers are offering concessions and inventory is rising. The buying decision was the hard part. The process from here is a checklist — and the first two items are due in 48 hours.