Every personal finance article you've read about mortgages probably told you the same thing: get the 15-year. Pay it off fast. Save a fortune in interest. And the numbers they cite are real — a 15-year mortgage on a $270,000 loan at today's rates does save roughly $207,900 in interest compared to a 30-year loan. That is not a myth. What is a myth is the idea that this deal is right for most first-time buyers, or that the interest savings represent the full financial story.

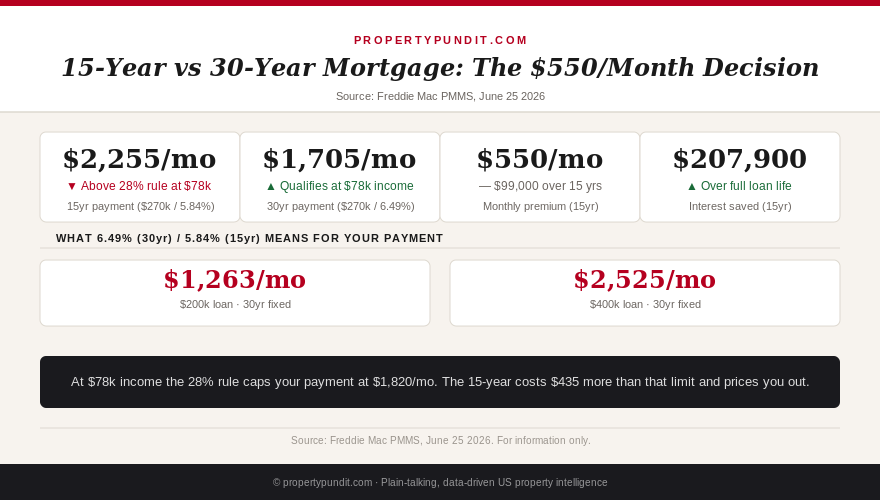

At $78,000 in annual income, the standard 28% housing-to-income guideline gives you $1,820 per month to spend on principal, interest, taxes, and insurance. The 15-year fixed at 5.84% (Freddie Mac PMMS, June 25, 2026) costs $2,255 per month on a $270,000 loan. That is $435 over your limit — and your lender knows it. The 30-year fixed at 6.49% on the same loan costs $1,705 per month, leaving $115 of budget room. That is not just a cash flow difference; it is a qualifying difference. The 15-year loan price-outs you from the home before you can even apply.

Get this in your inbox every Friday.

One email. The number that matters and what it means for you.

The full payment comparison: $270,000 loan at current rates

Here is the side-by-side on a $270,000 loan, the approximate amount a buyer at $78,000 income with 10% down would borrow on a $300,000 home.

The 15-year fixed at 5.84%: monthly payment $2,255. Total paid over 15 years: $405,900. Interest paid: $135,900. Monthly budget room at $78k income: $2,255 is 34.8% of gross monthly income — well above the 28% guideline and above most lenders' qualifying ceiling.

The 30-year fixed at 6.49%: monthly payment $1,705. Total paid over 30 years: $613,800. Interest paid: $343,800. Monthly budget room at $78k income: $1,705 is 26.2% of gross monthly income — under the 28% guideline and qualifying comfortably.

Interest cost difference: $343,800 minus $135,900 equals $207,900. That is real money. But notice what it costs: $550 more per month for 15 years, and the 15-year rate (5.84%) is actually lower than the 30-year rate (6.49%) — which is typically the case, since shorter terms carry less risk for lenders. Even with that rate discount, the higher payment makes the 15-year unaffordable for most buyers in this income bracket.

The income you need to comfortably afford the 15-year payment: $2,255 divided by 28% equals $8,053 per month in gross income, or $96,643 per year. That is $18,643 more than $78,000 — roughly what a buyer with a 30% income increase from a promotion or a dual-income household with combined $96k can access. For a solo buyer at $78k, the 15-year is not a choice; it is not available at this loan amount without an underwriter willing to stretch to 35% or more of gross income, which most won't do for a first-time buyer without compensating factors.

The buying power problem: 15 versus 30 years at the same income

The payment gap does more than change your monthly budget — it changes how much house you can buy. This matters because most first-time buyers are shopping against a specific set of homes in a specific market at a specific price point.

At $1,820 per month maximum (28% of $78k gross), here is the maximum loan each term supports:

The 15-year at 5.84%: maximum loan of approximately $217,800. With 10% down, maximum home price of $242,000. With 20% down, maximum home price of $272,250.

The 30-year at 6.49%: maximum loan of approximately $288,100. With 10% down, maximum home price of $320,100. With 20% down, maximum home price of $360,125.

The 30-year lets you buy a $360,000 home on the same income. The 15-year limits you to $272,000. That is an $88,000 difference in buying power — which in most markets represents the gap between the home you want and the home that is actually available at your price point.

In Atlanta, where a buyer at $78k income is trying to get into a neighborhood with decent school ratings and a reasonable commute, $272,000 is a tight ceiling. The $320,000 to $360,000 range unlocks meaningfully better options. Choosing the 15-year does not just cost you $550 per month — it could cost you the home you actually wanted to buy.

The opportunity cost argument: what $550/month does over 30 years

This is where the 15-year versus 30-year argument gets interesting — and where most financial advice stops short.

If you take the 30-year mortgage and invest the $550 monthly difference in a diversified index fund earning 7% annually (roughly the historical real return of a US total market index fund over long periods), here is what happens at the end of 30 years:

Monthly contribution: $550. Annual return: 7%. Years: 30. Future value of those contributions: approximately $671,000.

Compare that to the $207,900 in interest savings from the 15-year mortgage. The investment approach produces more than three times the financial benefit — assuming you actually invest the difference consistently, which is admittedly a large assumption for many people.

But there is a catch: after year 15, the 15-year borrower owns their home free and clear and can invest $2,255 per month (their former mortgage payment) for the remaining 15 years. At 7%, that generates approximately $707,000 on its own. The true comparison is more complex than either number suggests, and it depends heavily on whether you hold the home for 30 years (unusual), what market returns actually do, and whether you have the discipline to invest the monthly savings consistently.

The cleaner way to think about it: the 30-year mortgage is a tool that preserves monthly cash flow and buying power at the cost of more lifetime interest. The 15-year is a forced savings mechanism with a guaranteed return equal to your mortgage rate (5.84%). If you are unlikely to invest the $550/month savings, the 15-year's forced paydown is valuable. If you are disciplined about investing, the 30-year often wins mathematically.

The third option nobody mentions: the 30-year with voluntary extra payments

Here is the move that solves the entire debate for most buyers in this situation: take the 30-year mortgage, and pay extra principal each month when you can afford to.

On a $270,000 loan at 6.49%, the minimum payment is $1,705. If you add $200 per month in extra principal — putting you at $1,905 total — you cut the loan payoff from 30 years to approximately 24 years and reduce total interest by roughly $85,000. Add $550 per month (equivalent to the 15-year payment), and you have effectively recreated the 15-year payoff schedule without being locked into the higher payment during months when cash is tight.

The critical advantage of the 30-year with voluntary extra payments over the actual 15-year: if you lose your job, face an unexpected medical expense, or need to redirect cash flow for six months, you drop back to the $1,705 minimum. The 15-year has no such floor — the $2,255 is contractually required every month regardless of circumstances.

For first-time buyers, financial flexibility in the first five years of homeownership is more valuable than it looks in a spreadsheet. The hidden costs of homeownership — maintenance, appliances, HVAC systems, roof — hit hardest in year one through five. Your true monthly cost as a homeowner averages $675 above your mortgage payment. A rigid $2,255 commitment leaves almost no room for those surprises.

When the 15-year actually makes sense

The 15-year mortgage is the right choice for a specific buyer: someone who already owns a home with significant equity, has a high income relative to the loan amount, is refinancing into a 15-year to lock in a lower rate and accelerate payoff, and does not need the monthly flexibility.

The income math: if your household earns $130,000 or more and you are borrowing $270,000 (a low loan-to-income ratio), the $2,255 payment is 20.8% of gross monthly income — comfortable, qualifying easily, and leaving significant room for savings and living expenses. At that income level, the interest savings are meaningful and the payment constraint is not binding.

The refinancing scenario: a buyer who took a 30-year at 7.5% in 2024 and is considering refinancing now faces a different analysis than a new buyer. If their remaining balance is $250,000 and they refinance to a 15-year at 5.84%, the payment increases by roughly $280 per month versus a 30-year refi at 6.49% — but they shave years off the payoff and save significant interest while the spread between 15-year and 30-year rates is above 0.6 points.

The myth to dispel is simpler: the 15-year is not automatically better just because it saves more interest. For a first-time buyer at $78,000 income buying a $300,000 home, the 30-year preserves buying power, keeps your payment within qualification limits, and leaves room for the unexpected. As covered in our mortgage amortization explainer, the interest front-loading of a 30-year feels painful in the early years — but the flexibility it provides is worth the cost for most first-time buyers in this income range.

What this means for your decision today

If you are a first-time buyer at $75,000 to $90,000 in annual income borrowing $240,000 to $290,000: take the 30-year. The 15-year payment will either price you out of your target home, push your debt-to-income above qualifying limits, or leave you so cash-flow constrained in year one that the first major repair bill creates a crisis. Use the 30-year to get in the door and build equity through appreciation and gradual paydown. When your income grows and you refinance in five to seven years, you can revisit the 15-year calculation with a much smaller balance and a more comfortable payment.

If you are earning $110,000 or more with a modest loan amount relative to income: run the actual 15-year numbers for your specific situation. At higher incomes and lower loan-to-income ratios, the interest savings genuinely win and the payment constraint is manageable. The 15-year works — it just does not work for everyone, despite what the generic financial advice implies.

The bottom line: the $207,900 savings are real. The 15-year mortgage is a powerful wealth-building tool for buyers whose income comfortably supports the payment. For everyone else, taking the 30-year and directing the savings toward either extra payments or index fund contributions tends to produce better financial outcomes with less risk. Know which buyer you are before the lender presents the choice.

For context on how your lender calculates your qualifying budget and why the approved amount often differs from what you should actually borrow, see our pre-approval vs budget explainer. Understanding both numbers before you shop is the single most useful thing a first-time buyer can do in the current rate environment.