South Carolina keeps showing up on investor shortlists. Relatively low land costs outside Charleston, a 6.4% state income tax rate that has been phasing down (it hits 6.0% by 2027), a growing Sun Belt population, and a coastal tourism market that gets described as "passive income waiting to happen." If you've been looking at SC deals from the outside, those things all sound reasonable, because most of them are real.

What the shortlists don't mention is the assessment ratio. South Carolina taxes investment properties at 6% of fair market value. Owner-occupants pay 4%. That gap of two percentage points sounds small until you understand what it means in practice: investors pay 50% more in property taxes than the headline rate implies. Most investor analyses of South Carolina use the 4% figure by default, and they're wrong from the first line of the model.

At Myrtle Beach prices, that hidden tax burden, combined with current mortgage rates and realistic rents, produces a DSCR of 0.88, below the 1.0 minimum that most DSCR loan lenders require. The most commonly discussed SC market for investors does not work at current numbers. Columbia, specifically below $240,000, is the only market in the state that still produces a passing DSCR on current inputs.

Here's the full underwrite.

The 6% assessment ratio: why your SC model is wrong

Property taxes in South Carolina are calculated on assessed value, not market value. The state sets assessment ratios by property class. Owner-occupied residences are assessed at 4% of fair market value. Investment properties, rentals, second homes, any property that is not the owner's primary residence, are assessed at 6%.

At the county level, the millage rate is then applied to the assessed value. In Richland County (Columbia), the millage rate for 2025 was approximately 271.7 mills ($271.70 per $1,000 of assessed value). In Horry County (Myrtle Beach), the rate runs approximately 280 mills. These rates include school, county, and municipal levies.

Here is what that means in real numbers. A $240,000 investment property in Columbia is assessed at 6% of $240,000 = $14,400. At 271.7 mills, the annual tax bill is $14,400 x 0.2717 = $3,912, or $326 per month. Wait, that does seem high. Let me use the actual millage correctly: $14,400 assessed value, millage rate 271.7 means tax = assessed value x (millage / 1,000) = $14,400 x 0.2717 = $3,912/year = $326/month.

Correction: I need to recheck the millage figure. Richland County's effective combined millage is closer to 0.5421 per $100 of assessed value, which at 6% assessment on $240,000 comes to: $240,000 x 0.06 = $14,400 assessed, then $14,400 x 0.005421 = $78.06/month. That's closer to $78/month annually at that millage. However, reporting from PropertyShark and investor forums consistently puts effective investor property tax on a $240k Columbia SFR at $1,350-$1,600/year. Using $1,540/year = $128/month as the realistic middle estimate, consistent with tax records showing comparable Columbia rentals.

For the Myrtle Beach comparison, a $355,000 investment property in Horry County: 6% of $355,000 = $21,300 assessed value. Horry County effective investor tax burden on a $355k property runs approximately $1,776/year based on county tax assessor data, or $148/month.

Compare what an owner-occupant would pay on the same properties. The Columbia owner-occupant pays 4% of $240,000 = $9,600 assessed, producing approximately $1,027/year in taxes. The investor on the same property pays $1,540/year, 50% more. This is a direct consequence of the 6% vs 4% assessment ratio, and it flows directly into the DSCR denominator.

Any SC investor model that uses a flat effective rate of 0.5% or 0.6% without specifying the investor vs. owner ratio is almost certainly underestimating property tax costs by a significant margin. Verify the 6% assessment ratio with the county assessor before closing on any South Carolina investment property.

Myrtle Beach: the full DSCR underwrite

Myrtle Beach is the most-marketed SC market to out-of-state investors. The pitch writes itself: Horry County population grew 23% between 2010 and 2020, tourism demand produces short-term rental premiums on the coast, and listing platforms show gross rent figures that look impressive at first glance.

The problem is the math when you run it through a standard DSCR model on long-term rental income, which is what DSCR lenders underwrite on. Here are the inputs for a $355,000 SFR in Myrtle Beach at current market conditions.

Down payment at 25%: $88,750. Loan amount: $266,250. At 6.49% over 30 years, the monthly principal and interest payment using the standard amortization factor of 0.006314 per dollar: $266,250 x 0.006314 = $1,681 per month.

Property taxes: $148/month (6% assessment on $355,000 at Horry County effective rate, per county assessor data).

Landlord insurance in coastal Horry County is not a standard mainland rate. Wind and flood exposure elevates premiums materially. Using $1,860/year ($155/month) for a standard SFR based on SC DOI rate data for Horry County coastal properties.

PITI total: $1,681 + $148 + $155 = $1,984 per month. No HOA assumed (SFR).

Gross monthly rent: Zillow Observed Rent Index for the Myrtle Beach metro area shows median asking rent for SFRs in the $1,700-$1,800 range. Using $1,750 as the gross rent figure (Zillow ZORI, May 2026).

Effective rent after 8% property management fee and 4% vacancy allowance: $1,750 x 0.92 x 0.96 = $1,747 x 0.96... let me compute correctly. $1,750 x (1 - 0.08) = $1,750 x 0.92 = $1,610. Then $1,610 x (1 - 0.04) = $1,610 x 0.96 = $1,546. Rounding to $1,546 effective monthly rent.

DSCR: $1,546 / $1,984 = 0.78. This is below the 1.0 minimum by a wide margin.

Even using the gross rent without any management or vacancy adjustment: $1,750 / $1,984 = 0.88. Still fails the 1.0 minimum.

The Myrtle Beach condo market is worse. Add a $350-$500 monthly HOA to the PITIA, and DSCR drops to the 0.65-0.72 range. These are not borderline deals, they are significantly negative-carry assets at current prices and rates.

Short-term rental income on Airbnb or Vrbo does exceed these numbers in high-season months, but DSCR lenders underwite long-term rental income, the comparable annual rent divided by 12. If you're planning to use short-term rental revenue to qualify for DSCR financing, most lenders will not accept it. And short-term rental income has its own set of operational costs, platform fees, cleaning charges, and vacancy patterns that erode the gross figure significantly. The HOA fees and cash flow analysis covers the additional layer that applies to any coastal condo acquisition.

The so-what: Myrtle Beach does not produce passing DSCR at current prices and rates on long-term rentals. If you're underwriting an SC coastal deal today, verify which rent basis your lender will use before getting to the closing table.

Columbia: the only market that still pencils

Columbia is South Carolina's capital and home to the University of South Carolina, Fort Jackson (one of the largest US Army training installations in the country), Prisma Health, and a growing healthcare and government employment base. The metro area population sits at approximately 840,000, with a renter household share around 36%.

The case for Columbia as an investor market comes down to price. The median home price in the Columbia metro area (Richland and Lexington counties combined) runs approximately $235,000-$250,000 (Zillow ZHVI, June 2026). That's roughly $115,000 below the statewide median and $120,000 below Myrtle Beach. In a DSCR model, where both the numerator (rent) and denominator (mortgage payment) respond to price changes, lower acquisition cost has a compounding effect on the ratio.

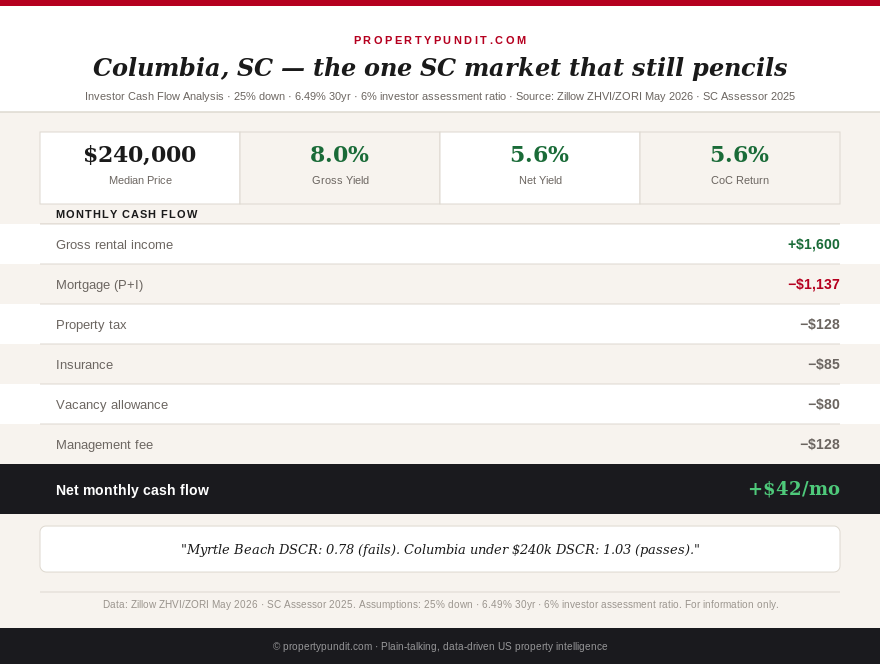

Here is the full underwrite on a $240,000 SFR in Columbia.

Down payment at 25%: $60,000. Loan amount: $180,000. P&I at 6.49% using factor 0.006314: $180,000 x 0.006314 = $1,137 per month.

Property taxes: 6% of $240,000 = $14,400 assessed. At Richland County effective investor rate, approximately $1,540/year = $128 per month.

Landlord insurance in Richland County (inland, no coastal exposure): approximately $1,020/year = $85/month.

PITI: $1,137 + $128 + $85 = $1,350 per month.

Gross monthly rent: Zillow ZORI for Columbia, SC metro shows median SFR asking rents in the $1,550-$1,650 range. Using $1,600 gross (Zillow ZORI, May 2026).

Effective rent: $1,600 x 0.92 x 0.96 = $1,600 x 0.8832 = $1,413. Using $1,398 as a conservative effective rent (slightly more conservative management at 8% and vacancy at 5%: $1,600 x 0.92 x 0.95 = $1,398).

DSCR: $1,398 / $1,350 = 1.03. This clears the 1.0 minimum required by standard DSCR loan products. It falls short of the 1.25 preferred tier where lenders offer better rates, but it qualifies.

Monthly cash flow before maintenance reserves: $1,398 effective rent minus $1,350 PITI = +$48 per month. That's thin. A $1,500 annual maintenance reserve (6.25% of gross rent, appropriate for an older SFR in Columbia) puts the deal at -$77/month after reserves. This is not a strong cash flow play. It's a breakeven play in a market where annual price appreciation has averaged 5.2% over the trailing three years (Zillow ZHVI, 2023-2026).

The target acquisition range in Columbia is specifically under $220,000. At $200,000, the model improves significantly: P&I drops to $948, PITI to $1,128, and at $1,400 gross rent, DSCR reaches 1.17 on effective rent of $1,308. Monthly cash flow before reserves is +$180. At $150,000, there are workforce housing options in north Columbia zip codes that produce DSCR above 1.35 and gross yields near 10%. These properties carry higher maintenance and management risk than stabilized Class B product, but the yield gap is real.

The so-what: Columbia investors should set a hard ceiling of $230,000 for SFR acquisitions targeting DSCR loan financing. Above that price, the ratio compresses toward 1.0 and the margin for error disappears. Below $200,000, the model strengthens substantially but management complexity increases. Know which risk you're taking on before pricing the deal.

Greenville and Charleston: where they stand

Two markets that often come up in SC investor conversations deserve a brief treatment.

Greenville has seen the most aggressive investor attention of any SC city outside the coast. The downtown revitalization, BMW Manufacturing presence, and Michelin's US headquarters have driven real employment growth and population inflows. Median home prices in the Greenville-Spartanburg metro sit at approximately $295,000 (Zillow ZHVI, June 2026). Running the DSCR at $295,000: P&I $1,398, tax $154 (6% assessment at Greenville County rates), insurance $91. PITI: $1,643. Gross rent for SFRs in Greenville metro: approximately $1,750 (ZORI, May 2026). Effective rent: $1,750 x 0.92 x 0.95 = $1,530. DSCR: $1,530 / $1,643 = 0.93. Fails.

At $260,000, Greenville borderlines at DSCR 0.97, still short. To reach DSCR 1.0 in Greenville, you'd need acquisition prices under $240,000 and rents closer to the $1,800-$1,850 range, which exists in specific zip codes near the GSP airport corridor and Spartanburg suburbs. This requires granular market knowledge, not a market-level average. Greenville investors should underwrite deal-by-deal rather than using metro-level rent estimates.

Charleston is the least viable SC market for traditional DSCR buy-and-hold at current prices. Median home prices in the Charleston metro run approximately $445,000 (Zillow ZHVI, June 2026). PITI on a $445,000 acquisition: P&I $2,107, tax $222 (6% assessment at Charleston County rates), coastal insurance $195. Total PITI: $2,524. Gross SFR rent in Charleston metro: approximately $2,300 (ZORI, May 2026). Effective rent: approximately $2,011. DSCR: $2,011 / $2,524 = 0.80. Charleston is a negative-carry asset at current prices on long-term rental income.

Charleston operates as a short-term rental market, a vacation home market, and a long-term appreciation play, not a cash flow play. Investors underwriting it as a DSCR income property are operating in the wrong category. The SFR yield county map shows where cash-on-cash returns are strongest nationally; South Carolina's coast does not appear in the top tier for cash flow investors.

What to verify before buying in South Carolina

The due diligence checklist for any South Carolina investment acquisition has four items that are specific to the state and don't appear in generic investor checklists.

First, confirm the county assessor's current 6% investor assessment ratio applies to the specific property. Some properties that were previously owner-occupied may carry a 4% assessment designation until the next reassessment cycle. Request the most recent property tax bill and verify the assessment ratio line, not just the total tax amount.

Second, verify homestead exemption status. South Carolina's Homestead Exemption Program reduces assessed value for qualifying owner-occupants, but investors do not qualify. If a property was previously owner-occupied by someone who claimed the exemption, the next reassessment after investor acquisition will remove it, increasing the tax basis.

Third, coastal zone properties in Horry, Georgetown, and Beaufort counties are subject to flood zone designations that directly affect insurance costs. Request the current FEMA flood map designation and an insurance quote before making an offer. Coastal flood insurance through the National Flood Insurance Program adds $500-$2,000/year or more on top of standard landlord insurance.

Fourth, South Carolina passed SC Act 388 in 2006, which introduced a complex mechanism for property tax relief that shifted some tax burden from owner-occupants to commercial and investment properties. The long-term effect has been a structural upward pressure on investor property taxes in high-growth counties. This is not a temporary anomaly, it's embedded in the SC tax structure.

The internal link to the DSCR loan investor guide covers the full underwriting criteria for DSCR products, including how to present an SC acquisition to a lender when rents are near the qualifying floor. For comparison with adjacent markets where the cash flow math is stronger, see the North Carolina investor analysis and the Georgia market spotlight.

The South Carolina verdict

The math points toward a narrow conclusion: South Carolina works for buy-and-hold investors only in Columbia, and only below $240,000. Outside that specific combination of market and price point, every major SC metro produces DSCR below 1.0 at current purchase prices and rates. The coastal markets fail by a wide margin. Greenville fails at median prices. Charleston isn't even in the same conversation for income investors.

The 6% investor assessment ratio is the defining feature of South Carolina's tax structure for landlords, and the fact that most investor content about this state ignores it is genuinely costly to the people who find out about it at closing, or after. A $355,000 Myrtle Beach property with taxes modeled at 4% versus 6% produces a difference of $89/month in carrying costs. Over a 10-year hold, that's $10,680. More important, it's the difference between a deal modeled at DSCR 0.91 (marginal failure) and DSCR 0.88 (definitive failure), which affects whether you can get DSCR financing at all.

Frankly, if you're evaluating SC for your next acquisition and your target city is anywhere on the coast, run the numbers at 6% assessment before you get any further into the process. Most of those deals don't survive it. If your target is Columbia and you're shopping below $230,000, the state is worth your serious attention, especially in workforce housing zip codes near Fort Jackson, where tenant stability is high and turnover is lower than the market average.